If you earned interest from a money market fund or bond mutual fund/ETF last year, a significant portion of this interest may have come from US Treasury bills and bonds, which are generally exempt from state and local income taxes. (California, Connecticut, and New York have special rules.) However, in order to claim this exemption, you’ll probably have to manually enter it on your tax return (or be sure to notify your accountant) after digging up a few extra details. The details are almost never included on your 1099-DIV form.

Here’s how to do it in at TurboTax.com, the online version of TurboTax tax software. (I received some requests for a more detailed walkthrough after my H&R Block version.) I found the following information from the TurboTax FAQ:

What about dividends from U.S. government bonds?

The federal government taxes income you receive from its own bonds. Although your state doesn’t tax income generated by U.S. government bonds, each state defines government bonds differently.

To find out if these dividends are taxable in your state, review your 1099-B along with the supplemental pages from your consolidated tax statement. If you can’t find the info, you might be able to get it from your brokerage or mutual fund company website.

Once you have found the info in your documents, just follow the screens here and we’ll help you enter an adjustment for the nontaxable amount in your state. When you get to your state taxes, we’ll subtract the adjustment from the income reported to your state.

I did not find “just follow the screens” especially helpful, so I started up a dummy return at TurboTax.com for 2023 and manually created a 1099-DIV form from “Apex Clearning” (sic) with $100,000 of total dividends. This is in the Federal return section. You may choose to import this form and then review it afterward.

This part should just be exactly the same as the 1099-DIV form that was sent to you. Don’t add any extra entries and just continue.

On the next screen, you should click on the box for “A portion of these dividends is U.S. Government interest.”

Here, you will enter the amount of interest (out of the amount in line 1a of your 1099-DIV) that represents interest from US government obligations. For example, if you received $100,000 in total dividends from the Vanguard Treasury Money Market Fund (VUSXX) in 2023, you will find it does meet the threshold requirements for California, Connecticut, and New York and it had a US government obligation percentage of 80.06% in 2023. In this example, $80,060 of the $100,000 in dividends would be excludable. I would enter $80,060 in the form below.

This information should carry through to your state tax return, reducing your state taxable income.

Here are some links to find the percentage of ordinary dividends that come from obligations of the U.S. government. You should be able to find this data for any mutual fund or ETF by searching for something like “[fund company] us government obligations 2023”. If you do not see the fund listed within the fund company documentation, it may be because it is 0%.

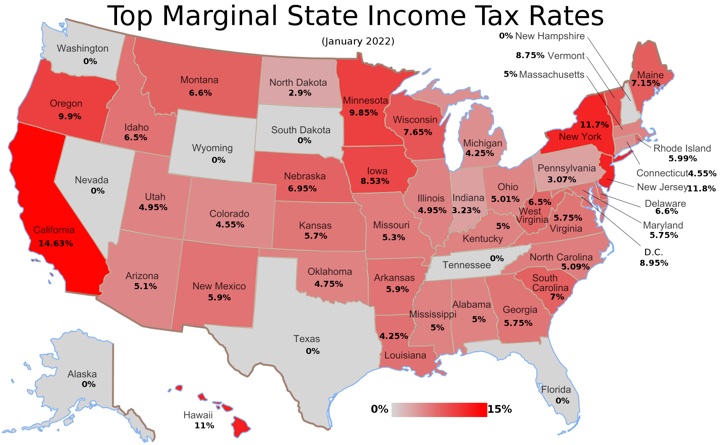

[Image credit – Tax Foundation]

In 2022, 21 states issued special relief payments to eligible residents in 2022. The Tax Foundation has a partial list of

In 2022, 21 states issued special relief payments to eligible residents in 2022. The Tax Foundation has a partial list of

The Best Credit Card Bonus Offers – May 2024

The Best Credit Card Bonus Offers – May 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - May 2024

Best Interest Rates on Cash - May 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)