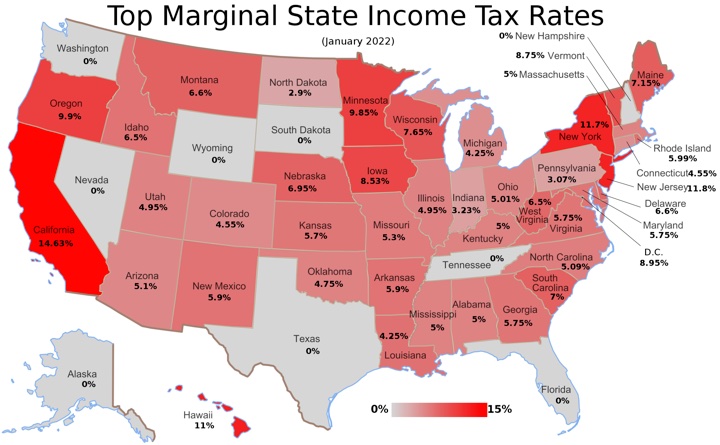

If you live in a state that taxes interest income, you may know that can significantly alter the net after-tax yield on your investments. This is because direct U.S. government obligations like Treasury bills and bonds are generally exempt from taxation in most states. For example, if a Treasury bill is yielding 5% but is exempt from a 8% state income tax, that would make it the equivalent after-tax yield of a bank CD at 5.65% APY (assuming 22% federal tax rate). That’s a pretty big difference! See Treasury Bond vs. Bank CD Rates: Adjusting For State and Local Income Taxes for details.

Money market mutual funds (available in most brokerage accounts) usually hold part of their portfolio in securities that count as US government obligations (USGO). (See Vanguard Federal Money Market Fund: How to Claim Your State Income Tax Exemption.)

For the 2022 tax year, Vanguard Federal Money Market Fund (VMFXX) had about 38% in USGOs, but the Vanguard Treasury Money Market Fund (VUSXX) had 100% in USGOs (source). As long as the yields were pretty close, your after-tax yield would be much higher with the Treasury Money Market fund if you were in a high state/local tax bracket. (VMFXX is the default sweep though, so you’d have to manually purchase VUSXX.)

However, these USGO percentages can change from year to year, and it is happening in 2023. A quick rewind – here is a list of what is and is not exempt from state and local taxes.

*Investments in U.S. government obligations may include the following: Federal Farm Credit Banks, Federal Home Loan Banks, the Student Loan Marketing Association, the Tennessee Valley Authority, the U.S. Treasury Department (bonds, notes, bills, certificates, and savings bonds), and certain other U.S. government obligations. GNMA, FNMA, Freddie Mac, repurchase agreements, and certain other securities are generally subject to state and local taxes.

In particular, even though the Vanguard Treasury Money Market Fund has “Treasury” in its name, it doesn’t only hold Treasury Bonds. It can also hold something called repurchase agreements (“repos”). These are often sold on a very short-term basis (overnight or less than 48 hours). While a repo is considered a very, very safe loan backed by government securities, it is not itself a government security, which means the income it creates is taxable at the state and income level.

As of July 2023, here is the percentage of repurchase agreements held by these two example money market funds: 58% for VMFXX and 34% for VUSXX. This would suggest that the USGO number for VUSXX will be significantly less than 100% for 2023, although VUSXX still holds less repos than VMFXX.

For an in-depth comparison, “retiringwhen” of the Bogleheads forum has created a detailed Google Spreadsheet that tracks and calculates the after-tax yields for several different money market funds from Vanguard and Fidelity. I would point out that the low expense ratio of Vanguard funds makes their money market funds consistently better than Fidelity money market funds across the board.

I also hold some Treasury bonds directly and while laddering isn’t that much hassle, recently I have been considering simplifying to VMFXX and VUSXX as the go-to place for my liquid cash savings account. For now, the tax-equivalent yield is higher than nearly all other savings accounts due to my high state-tax situation. I am also looking at ETFs that hold mostly T-bills like SGOV and BIL.

Bottom line. If you want to be precise, the full-geek DIY investor with state/local income taxes has to take into account the percentage of repos in their money market fund portfolios in order to calculate the true tax-equivalent yield to compare against other cash alternatives.

[Top image credit – Wikipedia]

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

It would be great if you could do a similar article but on property taxes and add that to the state income taxes to get a sum total of taxes. Then also add in what property values are in each state. States that do not have an income tax have high property taxes with high property values so tax payers may actually be paying more overall taxes.

Agreed, and there are also sales and/or general excise taxes as well. You may find this link interesting:

State and Local Tax Burdens, Calendar Year 2022

https://taxfoundation.org/publications/state-local-tax-burden-rankings/

Oh yeah, hard to see these numbers… additional taxes. Let us all move to Alaska !!! Plus, you will get a resident’s bonus annually from the State of AK because of the oil revenues.