LendingClub.com is a website that securitizes person-to-person loans so that you can lend money to other people in as little as $25 increments, and you collect the interest after some fees. The idea is to replace banks and credit cards as the major middlemen used for lending. “Investors earn better returns, borrowers pay lower rates.” I’ve been investing some money with them since they started in 2007.

Last time I wrote about LendingClub in May, I expressed concerns about their historical performance data living up to their marketed 9.65% returns and then LendingClub responded on why they thought things weren’t that bad. It’s been 3 months, so I figure it’s a good time for another update.

The first part of their argument is that they think that loan performance over time will go like this, with a drop and then significant recovery near the end of the term:

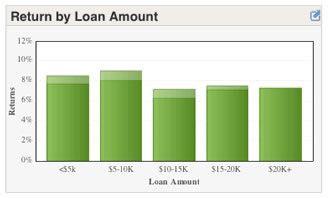

However, I don’t see that behavior happening. As you can see below, the older the loans, the lower the overall performance. Returns just keep dropping for loans going from 1.5 to 3 years old. There is no rise or recovery at the end of the three-year term. Data was taken from actual LC loans with observation date of August 17th, 2010.

Loans Originating Second Half of 2008 (about 1.5-2 years old)

Loans Originating First Half of 2008 (about 2-2.5 years old)

Loans Originating 6/1/2007 to 12/31/2007 (about 2.5-3 years old)

Note the change in the y-axis scale

Now, the next part of their argument was that all the loans that originated before they changed their credit requirements and interest rates at the end of 2008 weren’t a valid data set to be analyzing. (That doesn’t make me feel much better because as an early adopter, I hold a lot of those loans.) While improved underwriting may make the average returns higher, I don’t see why it should affect the overall performance behavior over time.

2009+ Loans Only

Okay, so the newer vintage loans that originated after January 1st, 2009 take into account their current lending criteria. In the end, we’ll just have to see if people really get higher returns. From now on, I’m going to try and track the performance every quarter. Here is the performance of loans originating in the first half of 2009, as of August 17th, 2010. Since it a loan has to be late for 4 months to be actually considered in default, this means the loans only have effective ages of 1 to 1.5 years.

So far, not too bad at about 8% return. Here is the performance of loans originating in the first quarter of 2009 with two observation dates (May 2010 and August 2010) overlaid on top of each other. You can see that the loan performance has decreased slightly over the last 3 months. I hope that I am wrong, and that the performance does start to improve.

You may call me a LendingClub basher, but I still consider myself an active investor and supporter. I want them to have awesome returns, but the data simply doesn’t support the likelihood of earning 9.5% annually. Investors should go into it with realistic expectations, and ideally an interest in P2P social lending. Despite this, if LendingClub can average, say 6% returns going forward, that would still be quite an accomplishment for this new business model. I know I’d be happy with that.

To Prospective Borrowers

Honestly, LendingClub is more attractive as an option for borrowing money and/or credit card debt consolidation. You can borrow up to $25,000 and you can know your rate before actually applying for the loan. If the rate quote they give you can be beaten elsewhere, then just walk away with no obligation. When writing your loan application, try to include as much applicable information as possible (reason for loan, how will you repay, monthly budget breakdown) and answer all lender questions promptly for the best results.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I’ve been investing in lending club for ~2 years now. My return is listed as 9.5%. Not too bad. I have, however, noticed the same trends you mention here so don’t plan on putting any new money in and will probably take money out as loan payments are made instead of reinvesting it. I tend to notice two trends in defaults: they either default after 1 or 2 payments, or they default more than a year into the loan. The defaulting after 1 or 2 payments really bothers me because it shows lending club’s screening process isn’t sufficient. I even had one person default before one payment.

I hope they succeed, but it’s still too new for me to throw much money into it. I’ll re-evaluate again in 2012 when post 2009 loans have had a chance to mature and we can see what the returns are really going to be like.

It’s pretty hard to get that 9.65% return no question about it. Otherwise, we all be putting our hard earn cash in this. Grade A loans seem to get you around 7%. Of course the $25 bonus is why everyone should give them a try.

Last time you did an LC post my rate was in the red, but I can happily say several months later I’ve climbed up to around 2.5%. I only have about 30 loans so all it takes is one deadbeat to really hose you. I find it rewarding but I wouldn’t throw too much of my dough in there.

I’ve been pretty happy with my lending club loans so far. However, I do think we have to keep in mind the economic situation that we are lending money in. High unemployment, BKs at a 5 year high, etc. We are bound to have a few delinquent loans in this environment.

My Lending Club return so far is over 11% and my loans are in their last year of repayment. So far I have only had one loan default which is lucky, I guess. Most of my invested money was from referral bonuses so my actual return is much higher. I like Lending Club but I still wouldn’t invest too large a percentage of my money there.

Okay, now what? I thought I carefully reviewed all the terms, but it turns out because I live in PA I can’t participate? Now what? I deposited $250 this morning. :\

I keep track of my net annualized returns on all money going into my LC account. So far I am at 9.1%. LC lists my return at 12.58%, but that does not include losses from selling bum notes. So far, I have sold 11 notes over the 16 months I have been on LC. Of those, 4 went to default after the sale and the rest are now current.

While I have sold the Grace Period notes at a 10% discount on average off the PAR value for a $25.10 loss, I have manged to net $74.11 over just letting them go into default. Considering I have only netted $96 total through LC, it appears that this strategy makes all the difference. I am not totally confident that there will always be a market for GC notes though. Especially if LC opens up to more states.

I have two suggestion for LC’s FolioFN:

1) Implement an automatic note alert system. I frequently try to sell notes that are in the grace period, but there is no way to automatically delist my note if it goes from “Grace period” to “Current”. Of the 11 notes I sold, 6 were sold right after they went current at because LC has no such mechanism. The lack of such a mechanism has cost me about 1.5% point in annualized. LC you need to fix this!

2) Change the default search option in the FolioFN note search. Right now the default is to only look for notes that have 60 or less payments remaining. The problem is that I am trying to sell a note that has 61 payments because it is a 60-month note that has not made a single payment and LC has added an extra catchup payment. As is, there is no way to find my note for sale on FolioFN.

I’ve been with LC for about 2 years…after using $25 from one of your first posts on LC. So far so good….that’s all I can say.

I’m getting about 8.5% so far with only one loan defaulting on the first payment. I think the guy just took the money and fled. Good thing it was only $25…and it was a referral bonus! So, no money lost yet.

I will be putting more money into LC this year only and then wait and probably just reinvest the money I get back.

It is impressing to see how many requests for loans they get and how little they actually approve for lending…the more requests they get the stricter they get on they lending. We’ll wait and see.

I work for a “big 4” bank and have quite a bit of lending knowledge. I have 45 notes outstanding and am earning 9.4% over 18 months. No defaults and I don’t venture into the C-grade folks very often. I think it comes down to knowing what is a good/bad credit risk. I personally find some A-paper rated candidates from LC that I would put in the lower B category. Be very careful about FICO score. The recent meltdown is a testament to the fact that you can’t rely on the FICO alone. Capacity to repay is the better criteria.

I like LC and have had success with it, two years in with over an 8.5% rate of return, no defaults, although one is currently over 31 days late.

But I think that one big drawback to LC is that you can’t pull your money out short of reselling your notes. Stocks can be sold at basically their value, which is not true for the notes. So I’m careful to not put too much into LC if there is any possibility that money could be needed as an emergency fund.

I have 5 LC accounts (kept opening them for the free $25 until I hit the limit) with a total of about 85 notes invested in. Of those, no defaults and only 1 31-120 days late. My lowest rate of return on any of my 5 accounts according to LC is 11.66%. I rarely invest in A loans because you can find lots of good C and D grade loans that look good. Recently I even invested in a G grade loan because the numbers made sense, the person had a stable job (if there is such a thing any more) and their story was very compelling. We’ll see how that goes. I don’t like to say I’ve been lucky because I really put a lot into picking loans to invest in. There are times I’ve gone a few days without buying any notes because I couldn’t find one that I liked. I think being afraid to invest in C, D, E, F and G loans is a mistake because you really end up missing out on some decent borrowers by not even taking a look at those loans.

If you’re getting a consistent 6-7% return after some defaults and complain about it, you better take the money and put it in a savings account as you are NOT an investor, you’re a money under-the-mattress kind of person. Look around, it’d be hard to get a great passive income investment like this out there… because bankers don’t want you to know about it. I have a good number of loans, and my share of defaults. Went from 10% to 5% and now back up to 7%… and in summary, I LOVE IT! I don’t sweat the defaults anymore like I did before. They are part of the whole game.

So from the BORROWER side of things:

I’m 1.5 years into a $9k loan I used for one of my real estate investments. Overall, I’m happy with the program and I got the funds @ 9.4% which was at least 0.75% less than my next cheapest option for an unsecured personal loan at the time.

What I don’t like:

1. You can’t find out what your rate is going to be until they perform a hard credit inquiry.

2. TWO credit inquiries are required, one from Lending Club and one from the bank that backs them. Whether you take out the loan or not, these will show up as inquiries for 2 years on your credit report.

3. It’s incredibly cumbersome to make additional principal payments unless you are paying off the loan in full. My payment is $288 but I’d like to make an additional principal payment of $100-$300 each month depending on that property’s expenses for the month, but there’s no easy way to do that. Instead, I just have to siphon the extra funds each month into a side account and make an early payoff when all the funds are available.

If it weren’t for the double inquiries, I wouldn’t hesitate to use them again.

I also wish they’d get approved by the state of OH so that I could be an investor as well!

-Billy

So, I opened an account but can’t seem to find anything on their website that mentions how to get the $25 bonus. You mentioned that I don’t have to deposit anything. What exactly do I have to do?

Thanks!