Time for fun with charts! A famous chart in the early retirement community is The Crossover Point from the book Your Money or Your Life, which shows that you’ve reached financial independence when your investment income equals your monthly expenses:

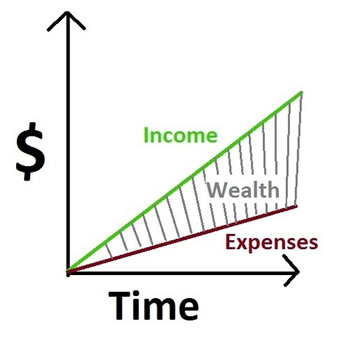

Fellow blogger Adrian of 7million7years also shared a related chart from Chris Han of Quora, where wealth is the shaded area between your income and expenses:

Specifically, if you plotted all your income and expenses over time, the shaded area between would the amount you’ve saved your entire financial life. Bigger shaded area, bigger nest egg.

(Math nerds: The units of income are dollars/time, i.e. $50,000 per year. Therefore, the area under the curve – integrals anyone? – is indeed dollars. If you measured the area under the curve for the green line, that would be all the money you’ve ever made. Do the same for the red line and that’d be all the money you’ve ever spent. The difference is what you’ve saved. Ignoring investment returns, that is indeed your wealth!)

The Problem

I’ve worked with people making $30,000 a year, and with those making over $300,000 a year. In both places, there are folks working until they’re past 65+ and still worrying about retirement. I suspect this is why:

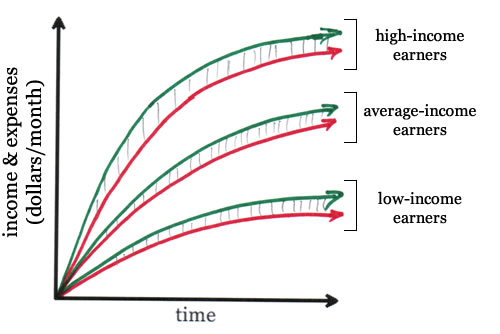

See the problem? Expenses tend to rise with income (lifestyle inflation), so that the size of the wealth wedge tends to stay the same! Sure, your house may be bigger and your car may park itself, but if their chart looks like this, they would all end in the same place if they faced extended unemployment: BANKRUPTCY.

The Solution

You have to mind the gap between income and expenses. This is another one of those simple but hard principles of personal finance. Some people find it easier to increase income. Some people find it easier to minimize expenses. It really doesn’t matter, as long as you keep the same amount of distance between the two lines the amount saved is the same.

Here are some parting thoughts. Chris adds:

Decreasing the slope of the red line becomes significantly harder over time as you grow accustomed to your lifestyle.

Adrian adds:

…it is easier to grow Wealth dramatically by increasing the slope of the green Income line than it is to decrease the slope of the red Expense line.

I would add that while increasing income is super-duper-awesome, lowering expenses has a double-impact. The lower your expenses, the bigger the Wealth wedge, and the smaller the Wealth wedge you need to be financially free. A high-income person and an average-income person could save the same amount, but the person with a much lower income could have a higher multiple of their expenses saved up and thus actually be better off financially.

What’s your insight into this deceptively simple chart?

The Best Credit Card Bonus Offers – July 2024

The Best Credit Card Bonus Offers – July 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - July 2024

Best Interest Rates on Cash - July 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I like your take on why people are always worrying about retirement. I believe it is indeed because people don’t maximize their gap. When I tell people I think I’ll only need $1.5 million or so for early retirement, they can’t believe I’m willing to “only” live on $45,000/year (at a 3% withdrawal rate). Meanwhile, I’m wondering how I could possibly spend nearly $4000/month when we currently only live happily on $2000/month! I think a lot of wealth is shifting your perspective and realizing you can have an incredible lifestyle anywhere in the world for not much more than the average American wage.

Yes! Totally! We r doing just that and loving it. 45 retired and doing it and traveling. Living on $22,000 with $45,000 available per year. We totally underspend and don’t feel deprived.

I think your “Problem” chart is generally correct in spirit, because most people tend to upgrade their lifestyle as they earn more. To do otherwise is exceptional, so count yourself as exceptional.

However, one thing to keep in mind is that our progressive tax system also plays a part in this. The folks on that lower income line aren’t paying any federal income tax, and indeed may be receiving transfer payments in the form of refundable tax credits. Last year my household paid a full 27% of our income in the form of federal income taxes (effective/average/total, not marginal tax rate), and if you add on my share of FICA and state income taxes, you can add another ~6-8% to that figure. That’s a pretty big hit to the wedge for people even if they continue to save a big % of their pre-tax income at a high income level. This isn’t a value judgement, just an observation.

Much of life is actually very simple. But people love to creatively complicate things, which adds needless difficulties.

I agree, it really is this simple. But simple is not always easy.

And, as a friend of my used to say, “If it were easy, everyone would do it.”

Should all those charts be exponential rather than logorithmic or linear (well unless the scale is logarithmic then) in shape, since inflation compounds just like everything else. Inflation also can mess with the ‘crossover point’ idea, but it’s a good way to think about money differently.

“Trend of Monthly incoming going up” => not easy but doable

“Trend of Total Expenses staying flat” => very hard to do if you are single, nearly impossible to do if you have a growing family.

a better(more general) chart would be just have slope of “Trend of Monthly incoming” be higher than “Trend of Total Expense”.

This is why I love your blog

Andy – 27% effective federal tax rate? Wow, you are doing very well for yourself. Vice President Biden and his wife paid less than 22%, and they had income of $385,000 last year.

Can’t tell for sure, since their chart only goes to 2009, but looking at the Tax Policy Center’s info at http://www.taxpolicycenter.org/taxfacts/displayafact.cfm?Docid=456 your 27% would put you in the top 1% in household income. Congrats.

The crossover point is a fallacy. Your expenses increase exponentially with inflation, but your investment income doesn’t.

Do the math… If you have $750k invested @ 7% return with $50k in expenses, your investment income exceeds your expenses. With 3% inflation, you’ll be broke in 25 years.

To make it work, you need your rate of return to increase exponentially over time. Good luck with that.

@sdub – I agree the original book was a little weak on the investment theory, but that’s why you should use an inflation-adjusted return. I would say most people should work with a safe withdrawal rate of 2-4% depending on age.

I have been living this chart for a long time, and preaching it to my kids.

I learned a long time ago the old adage (that is not so popular):

“IT IS NOT WHAT YOU MAKE THAT COUNTS, IT IS WHAT YOU KEEP THAT COUNTS”

America is full of the “Joneses showing off to each other” and diving deeper into debt. I live through this and watch the neighbors and family members violate this one rule, which you have forumalated into a chart in a really nice way.

Then, people complain about Foreclosure, Downsizing, Not being ready for Retirement, and also Not having enough for Goals. It is ALL upto us.

If we do not handle our Input and Output (for Health and Wealth), we will have to deprive ourselves of many situations in the future. It is basically a way to STEAL THE FUTURE FROM YOUR OWNSELF, BY LIVING IT OFF TODAY, AS IF TOMORROW WILL NEVER HAPPEN.

I am not sorry for people who then have to come and rent one of my properties at age 60 or 65 that I have bought with money that I did not spend in my 20’s or 30’s at expensive restaurants, or phenomenal vacations, or getting water with my meal instead of coke (for 30 years)!

Sacrifice Today For A Stronger Tomorrow has been what my parents taught me, and I am teaching my teenage kids.

Today, they have a lower end Samsung Android phone that we just got them a year ago, and they will sacrifice time to get a Samsung SIII, and we will buy it used (probably). So, no, they do not walk around with iPhones, or the latest iPods or any iPads, but we bought them a condo instead of a small dorm room so that they can have peaceful living while they go to the Univ.

Again, Sacrifice Today for a STRONG Tomorrow. And, none of those charts will have income and expense lines merging into each other causing chaos.

Just my 2 cents that I am living, and now preaching to anyone who wants to listen, learn and implement.

Kenny

PS: It was NOT easy to have one pair of sneakers for my kids, or run a car into the ground, or not upgrade the carpet to hardwood floors when it just had come out. No silver spoon here, just built from ground zero.

@Kenny – what a great story – and great words to live by. I am in my mid-30s, and trying to do the exact same (except I do buy a soda when out for dinner, and we do eat out) – we have a great income (north of 150), and are well on our way…and save about 60% of what we make.

Questions for you: how many rentals were you able to accumulate? were you able to retire? how many kids, and on what (ballpark) type of income? Any real estate resources you would direct me to – would like to follow in your footsteps. PS Sorry if I am prying…disregard if you are uncomfortable responding. Thanks!

People who don’t know me well see me living in an old house, drive a used car towards 200K miles, and have no smartphone. Close friends know my income has more than doubled, my stock portfolio has mushroomed, and I’ll be a millionaire before 40.