Eventually, you will be presented with the idea of writing covered calls on your portfolio and earning “easy income” from this strategy. I already know intuitively that there must be a cost to this “passive income” and that the net effect is worse performance than simply holding the same index fund or stock for the long term. However, the pushback is usually that you can get a more reliable cashflow in exchange for giving up some of your upside.

The article The Hidden Cost of Covered Call Writing (via Abnormal Returns) does a good job of explaining why there is unfortunately no “free lunch” with this strategy, even if your goal is to create steady income.

Many investors focus on the call premium as a source of portfolio “income” while still participating in a limited amount of appreciation of the stock. As long as the stock stays below the strike price and the call expires worthless, the strategy can generate positive portfolio income, making it ideal for flat or down markets. However, trying to time when stocks and markets will be flat or down is extremely difficult, particularly given the long-term upward bias of the equity markets. As such, there is a hidden cost of covered call writing, which is the potentially significant opportunity cost of having the stock go above the strike price causing lost portfolio appreciation.

Covered calls work great when they work out, since you get to keep your stock and the “free income”. Giving up your upside may seem like a good deal, but you must realize that much of the stock market’s return comes from lumpy periods where it shoots up without warning.

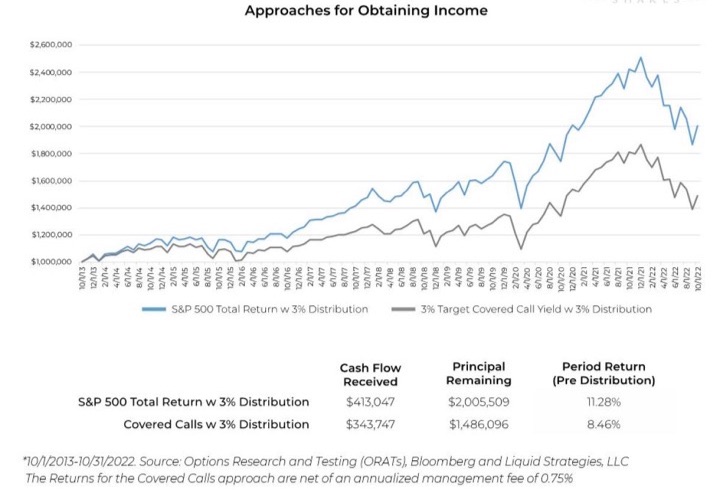

The chart below from the article compares the performance results between simply withdrawing 3% a year from your S&P 500 portfolio from 2013 to 2022, as opposed to writing covered calls with a 3% yield on your S&P 500 portfolio. The chart does add a 0.75% annual management fee for this approach, but even if you add that back in, the difference is still 11.3% vs. 9.2% annualized return.

Lower volatility is also commonly cited as a benefit of a covered call strategy. Well, yeah, if you limit your upside every time the strike price is exceeded, then you will have lower volatility.

In a rising market, covered calls may actually reduce upside portfolio volatility, which is the type of volatility that investors benefit from. As such, when evaluating covered call strategies that show lower volatility statistics than the broader market, investors should be mindful of where that volatility reduction may be coming from.

Am I willing to give up 2% in annual returns for a steady income? Nope. I mean, 2% is already roughly the entire dividend yield of the S&P 500. The problem is that most people who use this strategy aren’t properly tracking their performance and probably won’t know if they are lagging behind simple buy and hold. The call premium income comes in most of the time, so it’s easy not to realize the true cost of missing out on the gains.

There are certainly scenarios where if you think you have an information edge, knowing how to structure an option can help you make the right bet. But they aren’t magic! I am very skeptical of the idea of any options strategy that will somehow give you reliable income without a significant cost of hurting your total returns. That just gives me the same feeling of someone who claims to invent a machine that defies a basic law of physics.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I think that it would depend on the overall goal. I wonder if there’s a study that shows writing calls and never allow the shares to be called away.

How would that compared to the calls being called away or just the buy and hold strategy?

I was thinking about this; if a trader uses a relative low delta, say about 10 or 15, and writes monthly or semi annuaually calls, can still get some premium and keep the stocks, or roll it in case of getting close to the strike price. The real problem comes with the weekly/30 delta plays

I agree in general with your conclusion that you lose out by selling calls relative to just buying and holding because you sell off your upside. Mathematically, owning the underlying and selling a call is equivalent to not owning the security but selling a put–a strategy with very limited upside and nearly unlimited downside and not something people tend to think of as a good investment.

However, with the proliferation of index options and the reduction in commissions (~$2 per options trade at Schwab) AND the fact that most options expire worthless, I have started an experiment in covered call writing earlier this year to get a sense for whether there is potential there. Not as a substitute for long exposure in the portfolio but perhaps as a diversifying source of return from the time value of the options.

I bought 300 shares of SPY and have been systematically selling 3 contracts (300) of calls ideally at the money with weekly Friday expiration every week. Each Friday I roll out in one trade by buying back the expiring option and selling a new one expiring a week later. I have found that I can generate $800-$1,000 of premium per week, which over the course of a year would be a pretty attractive total return. Thus far the market has rallied so I’ve been losing money on the options piece but earning more than I’m losing on the underlying SPYs because the time value (theta) erodes each week.

I started this at the end of April. The S&P 500 is up 6.3% over that period and my return on the strategy has been 4%. If the market had been flat I would be up more like 5-5.5%, which to me illustrates why this could be an interesting addition to a portfolio. For small investors, diversification possibilities are relatively limited to long stock market exposure. For a portion of the portfolio, having something that can generate some return in the absence of the market going up could be worthwhile. So far it has made the portfolio look less bad on days and weeks while the market is down–the question is how much value will it add overall.

Anyway, I’m doing this as an experiment for a year to get a feel for the ins and outs of trading the strategy and how I will react in cases where the market is down (Should I close out the position early? If so should I enter into a new one with a lower strike?) and when it is up (Should I roll into a higher strike after a big up week or remain in a lower one hoping the market will go back down again and I can capitalize on the short exposure in the option? Should I just let my SPYs get called away and start over on Monday?). And of course to track in a spreadsheet how the strategy actually performs.

So in summary, you agree with the conclusion that it’s a losing strategy and then proceed to do the exact thing anyway wondering if your result will differ.

No. I agree that the strategy shouldn’t be expected to keep up with a 100% long equity benchmark, especially in rising equity market like we’ve seen for most of the last 15 years.

We may be entering a period with higher (or at least not falling) interest rates which won’t provide the same tail wind for long-only stocks and bonds–and also possibly a higher volatility environment where options premiums are higher than they’ve been over the last decade.

I think this may be a superior diversifier for replacing part of the stock/bond portfolio for individual investors who don’t have access to alternative investments. I also wouldn’t characterize anything with an 8 1/2% return over the historical period a “losing strategy.”

Jonathan, check out volatility risk premium as it says that options are overpriced on average and thus there’s an edge in selling them. However your article is a good example that mechanical option writing is not good enough to stand on its own, and requires position sizing and risk management. For example, when the markets tank, it’s not a good idea to roll the strike down to capture the same percentage yield as the market tends to snap back and you just took most of the downside while capping your recovery.

Also, yield and income is the biggest scam in this industry. So many crappy funds that offer high yields by cannibalizing their price returns. We’re need to be looking at total returns and compare with risk ratios like sortino etc and max drawdowns.

Where does the 3% yield on covered calls number come from? As of the market close on Friday, you could sell an at the money call on SPY for $3. This works out to ~0.7% yield for 1 week. If you could achieve a similar yield weekly that annualizes to ~36% per year. Quite a bit of upside risk however.

Want to mitigate that upside risk? (and you probably should), you could use $2 of that premium to buy a 1-week call with a strike of $432. While you are correct there is no free lunch, with this strategy, you lose at most $1/share and only if SPY closes between 430 and 432 next Friday. I would roll the position forward another week prior to Friday’s expiration and sell another covered call if that is at the money in the case that was to occur. At least then you are retaining the gain on the underlying shares. This strategy annualized out to about an 11% cash yield from premiums. Note that none of this is very tax-efficient.

That said, this strategy will generally outperform the underlying index in down markets and underperform in up markets (which are more common).

An easier way to accomplish a covered call strategy is to use GlobalX Covered call ETFs. There are 12 of them covering different indexes and tilts. They have somewhat higher expenses than a straight buy and hold index ETF but it saves a ton of work. Disclosure: I have small positions in QYLD and XYLD in a retirement account and have the dividends automatically reinvested. They pay just under 1% per month currently on average. My theory is that the higher dividend returns will allow me to DCA into more shares and mitigate the ETF’s underperformance against the underlying indexes.

You just do the strategy and take out 3% of the portfolio every year, same as with the buy and hold.

Thank you. This language “…as opposed to writing covered calls with a 3% yield on your S&P 500 portfolio” didn’t really convey that.

Spending the time to do this would definitely not be worth it for 3%.10-11% maybe…

To clarify, you can adjust your desired “yield” from options with the strike price on your options. So you could target a 3% yield or a 4% yield or a 5% yield, and you could reinvest or withdraw 3% of your portfolio, 4%, 5%, etc. The comparison here is between simply withdrawing 3% a year from your buy and hold portfolio, or trying to manufacture a 3% yield from options and then withdrawing that 3% a year.

You could get a 10% “yield” from options, and ETFs like QYLD will offer you this, but many people don’t realize the “income” you are getting is often just a return of principal. If you hand me $100,000, I can give you 10% income a year too ($10,000 a year)… I’d just be giving you some of your original $100,000 back as well each year.

I found selling puts and covered calls have been very lucrative for me . I consider myself a somewhat conservative investor and well over 90% of my covered calls expire worthless. Yes, I have been burned with stocks like NVDA, its meteoric rise did get away from me and the call was assigned at a significantly lower price, however higher than I paid for it.

Nothing is a sure thing, however, if you are willing to settle for lower premiums, thus reducing your risk I believe selling covered calls can be a successful strategy.

This is exactly why this strategy remains popular and why it lags a long portfolio. You feel the easy income 90% of the time, but you don’t realize what you are missing the other 10% of the time. The majority of the S&P 500 index long-term return is from a few huge winners. The winners often keep on winning for a long time. Once you add in the transaction costs and/or expense ratios, I have seen no long-term evidence that this strategy works. This post shows some evidence that I have found that it doesn’t work.

There is an empirical study on QQQ, SPY and IWM covered call strategy. QQQ seems to have gained the most which is obvious given the volatility. Interesting to watch it. Based on the study it does PAY to invest in covered call strategy on ETF/Indexes. Here is the study on You Tube.

https://youtu.be/JJAmSACWPLw

Do you have a direct link to the actual study? There is plenty of YouTube content on covered calls and QYLD, and it always sounds great, but I’d like to see an actual long-term study that takes into account trading costs and/or ETF expense ratios. QYLD is trendy due to its high income but I am skeptical it will beat a simple long strategy. I’d much rather be the ETF management company earning that expense ratio every year.

The video kind of is the study. You have to join the creator’s Patreon to see the actual spreadsheets.

Some caveats to it based on a brief watch of the video

– He’s analyzing only one five year period in time (2017-2022)

– He’s making some assumptions as to the premiums received, so there’s error introduced here.

– To his credit, he does address the cost of getting called out and repurchasing the shares the following business day using option premium money.

Did it for 6 months. Pretty successfully. Generally selling 30 delta puts (or calls if I owned the stock).

But it is a lot of work. And added stress. And when the market tanks, you are generally locked up from being able to mentally pull the trigger on writing calls when the strike is below your cost.

People are successful at it , but you have to have the right mindset and really tight risk management.

Instead I am currently devoting part of my portfolio to DIVO and JEPI, and let the pros write when it makes sense.

Finally, if this is done in a taxable account, the paperwork on the Schedule D is a pain!

If a person is living off invested assets isn’t it called “Hold and Sell” not “Buy and Hold?”

Buy a CEF like ETV from Eaton Vance, earn a steady 8-10% and let pro’s do the hard work.

Looking at ETV’s distribution history, it’s been declining since inception. Started at $.475 per share quarterly and is currently $.0945 monthly, about an 40% decline since the fund’s inception. At the same time, the share price has declined from ~$20 to $13.24

Had you bought 100 shares at inception in 2005 for ~$2000 you would have collected ~$2659 in dividends and had shares worth $1324 today. That barely kept up with inflation during the time period.

Had you reinvested all of the dividends, you’d have done better with a little over 600 shares worth roughly $8000.

If however you invested the same $2000 in SPY during the same time period, you’d have collected ~$1156 in dividends and had shares worth about $7261.67 today.

If you’d reinvested dividends, you would have shares worth about $10284 today.

So from an overall value perspective, ETV only (sort of) works if you reinvest dividends, which sort of negates the benefit of having that cash flow, which is decreasing over time anyway.

Not saying there is no reason to invest in ETV or other CEFs but SPY seems to win bigly.