Amazon keeps thinking up new ways for folks to send/receive/reload/ingest Amazon gift credits. Which is fine with me, because they’ll usually pay you a few bucks to try it out. Click here to check eligibility for their latest targeted offer: Get a $5 Amazon credit on your next order if you send a $50 Amazon gif card by text message by 12/22/18. If needed, use promo code SMS2018.

Amazon keeps thinking up new ways for folks to send/receive/reload/ingest Amazon gift credits. Which is fine with me, because they’ll usually pay you a few bucks to try it out. Click here to check eligibility for their latest targeted offer: Get a $5 Amazon credit on your next order if you send a $50 Amazon gif card by text message by 12/22/18. If needed, use promo code SMS2018.

Don’t forget that the Discover it card has Amazon.com as a 5% cash back category this quarter, so you might consider using that as your funding source if you don’t have anything better. Otherwise, you’re basically buying a gift card but make sure to choose “Text Message” as the delivery option. Yes, you can send it to yourself if you want. You should see a little grey box when you check out with this text:

Qualifying offers

Thank you for treating someone to an Amazon.com Gift Card. Now we’re treating you to a $5 promotional credit automatically applied to your account, and good for eligible products sold by Amazon.com.

Here’s the offer text:

Surprise someone with an Amazon.com Gift Card sent by text message, and get a $5 promotional code to spend on yourself. Just send at least $50 in Amazon.com Gift Cards by text message and in a single order by December 22, 2018, and receive a $5 promotional credit automatically applied to your account after the qualifying order has shipped. An email notification will also be sent within three (3) days after shipping, confirming your Amazon.com Promotional Credit.

If you’ve been holding onto that iPhone for longer than you thought you would, you are not alone. According to this

If you’ve been holding onto that iPhone for longer than you thought you would, you are not alone. According to this

Public libraries have offered eBooks for a while, but I stopped using the service because it was too much work. There weren’t that many popular titles available, and finding them was tedious with a waitlist of unknown length. When you did finally get the book, I couldn’t read it on my Kindle and would have to use a clunky third-party Overdrive app. These small hurdles meant that I often wouldn’t finish the book before the due date, upon which the book was unceremoniously yanked back into the cloud.

Public libraries have offered eBooks for a while, but I stopped using the service because it was too much work. There weren’t that many popular titles available, and finding them was tedious with a waitlist of unknown length. When you did finally get the book, I couldn’t read it on my Kindle and would have to use a clunky third-party Overdrive app. These small hurdles meant that I often wouldn’t finish the book before the due date, upon which the book was unceremoniously yanked back into the cloud. I started sharing my net worth anonymously because it was so hard talk about it publicly. Even today, my site logo is a voice bubble with money inside. Fast forward nearly 15 years later, and it is still unlikely that you know your coworkers’ salaries, let alone their net worth!

I started sharing my net worth anonymously because it was so hard talk about it publicly. Even today, my site logo is a voice bubble with money inside. Fast forward nearly 15 years later, and it is still unlikely that you know your coworkers’ salaries, let alone their net worth!

Consumer Reports shared some results from their 2018 Car Reliability Survey in the public articles

Consumer Reports shared some results from their 2018 Car Reliability Survey in the public articles

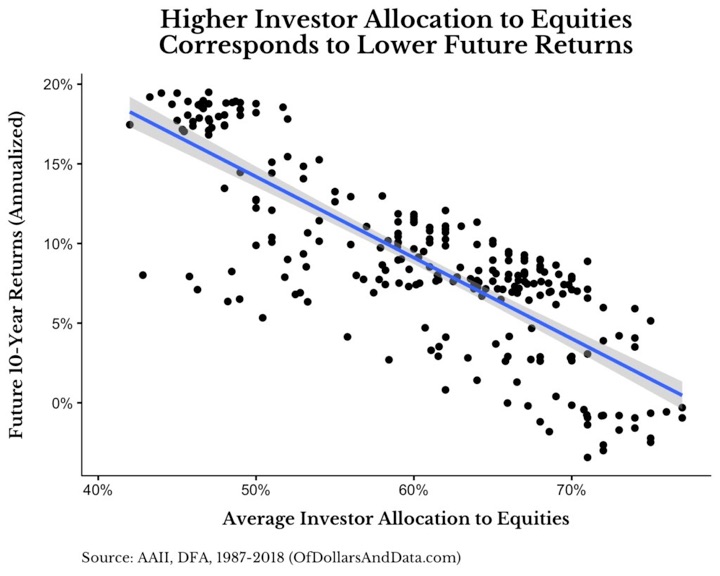

A recurring theme in my asset allocation philosophy is to stick with simple and safe bonds in your portfolio. The problem is, there will be other bonds that outperform safe, shorter-term US Treasury bonds and you might start to question your decision. I try to remind myself to consider how they fit into your entire portfolio. I would rather take on risk with stocks due to their big upside potential and use bonds for stability in times of stress.

A recurring theme in my asset allocation philosophy is to stick with simple and safe bonds in your portfolio. The problem is, there will be other bonds that outperform safe, shorter-term US Treasury bonds and you might start to question your decision. I try to remind myself to consider how they fit into your entire portfolio. I would rather take on risk with stocks due to their big upside potential and use bonds for stability in times of stress.

If you shop at Target stores and are an existing TopCashBack portal member, grab a

If you shop at Target stores and are an existing TopCashBack portal member, grab a

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)