Capital One 360 is running their annual Financial Independence Day promotion, with what is traditionally the best bonus of the year for their 360 Savings and 360 Checking accounts. (Formerly known as ING Direct.) These online bank accounts offer no monthly fees and no minimum balance requirements, all with a decent interest rate. As a result, the savings account makes a great “online piggy bank” where you can make free transfers from your existing checking accounts from any bank into the 360 Savings account on a regular basis. Promo details:

Capital One 360 is running their annual Financial Independence Day promotion, with what is traditionally the best bonus of the year for their 360 Savings and 360 Checking accounts. (Formerly known as ING Direct.) These online bank accounts offer no monthly fees and no minimum balance requirements, all with a decent interest rate. As a result, the savings account makes a great “online piggy bank” where you can make free transfers from your existing checking accounts from any bank into the 360 Savings account on a regular basis. Promo details:

360 Savings $76 Bonus

- Grab $76 when you open a 360 Savings® account.

- This has to be the primary account holder’s first 360 Savings account and it needs a $500 minimum deposit.

- The bonus starts earning interest on day 1, but you can’t take it out for at least 30 days.

360 Checking $100 Bonus

- Earn $100 when you open a 360 Checking® account. Sign up for fee-free 360 Checking®, make 5 Debit Card purchases or 5 mobile deposits with CheckMateSM within 45 days and snag a cool $100 on day 50.

- This has to be your and your joint account holder’s (if you have one) first 360 Checking account.

- Open 360 Checking from June 30th – July 3rd and make a total of 5 Debit Card purchases or 5 CheckMateSM deposits or any combination of the two within 45 days.

- Your $100 bonus will be automatically deposited into your account on day 50.

Update: There is now a 2-way tie for the most beautiful girl in the world. As we welcome our newest addition, posting will be lighter than usual for the next couple of weeks (years? decades?). Looks like early retirement might have to be pushed back a bit again…. totally worth it. 😉

Update: There is now a 2-way tie for the most beautiful girl in the world. As we welcome our newest addition, posting will be lighter than usual for the next couple of weeks (years? decades?). Looks like early retirement might have to be pushed back a bit again…. totally worth it. 😉  Updated. If you open multiple bank accounts in order to take advantage of higher interest rates or sign-up bonuses, you may be concerned about any potential consequences from all that activity. In my experience, there are two main factors to be aware of when you open a bank account:

Updated. If you open multiple bank accounts in order to take advantage of higher interest rates or sign-up bonuses, you may be concerned about any potential consequences from all that activity. In my experience, there are two main factors to be aware of when you open a bank account: Our family keeps a full year of expenses put aside in cash reserves; it provides us with financial stability with the additional side benefits of lower stress and less concern about stock market gyrations. Emergency funds can actually have a

Our family keeps a full year of expenses put aside in cash reserves; it provides us with financial stability with the additional side benefits of lower stress and less concern about stock market gyrations. Emergency funds can actually have a  I started following Jonathan’s blog about five years ago because I shared the same interest in personal finance and the goal of early retirement. I’ve made a lot of investing mistakes over the years, but with my 40th birthday coming up later this month I thought I’d share my approach which had the primary goal of income generation and capital preservation.

I started following Jonathan’s blog about five years ago because I shared the same interest in personal finance and the goal of early retirement. I’ve made a lot of investing mistakes over the years, but with my 40th birthday coming up later this month I thought I’d share my approach which had the primary goal of income generation and capital preservation.

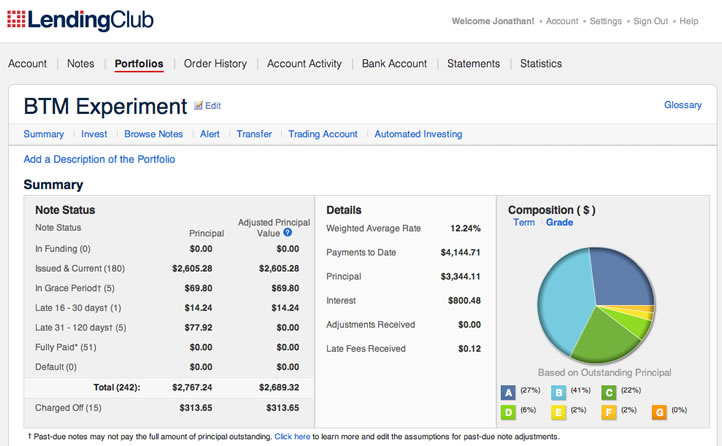

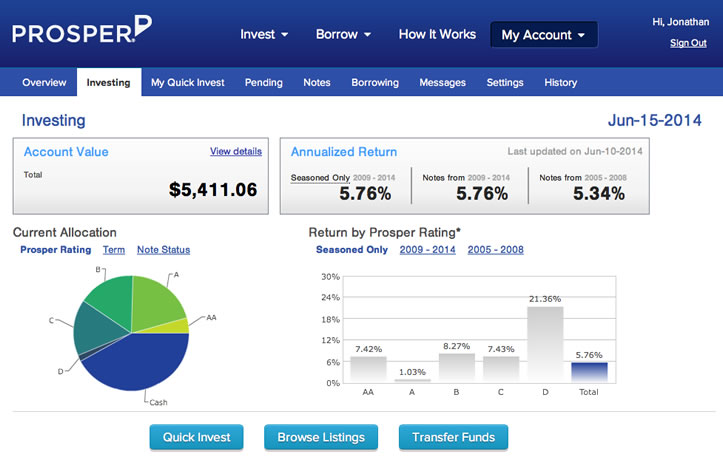

In November 2012, I invested $10,000 into person-to-person loans split evenly between

In November 2012, I invested $10,000 into person-to-person loans split evenly between

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)