My contrarian thought of the day? I feel that the retirement planning industry downplays the role of luck. Life is not a as certain as the smooth exponential curves that they show you. Perhaps the statistically optimal bet is to jump a bit early and hope for the best, while having a backup plan for the worst. You might just win an extra 10 years of freedom.

If you tinker with portfolio survival calculators like FireCalc and cFIREsim that model hundreds of possible paths, you may notice that the “failure” paths usually happen when a bear market occurs soon after you retire. If you keep spending when a portfolio is down, it may never recover.

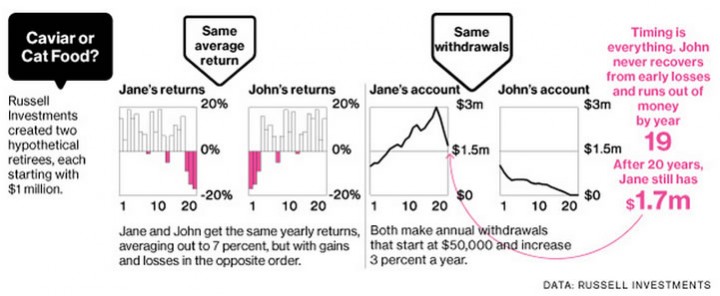

Even if you have the same portfolio size, same withdrawals, and the same average returns, having the bad years occur upfront can lead to failure while having the bad years at the end can lead to success. This is known as sequence of returns risk.

Retiring in 2000 with a 4% withdrawal rate: Warning! 🚨🚨🚨 In 2021, most people happily accept that the stock market just goes up and up. However, every so often there will be a “lost decade”. If you retired in 2000 with a portfolio invested in the S&P 500 and used a 4% withdrawal rate (increasing each year by 3% for inflation), here’s how that would have looked like (yellow line):

Retiring in 2010 with a 4% withdrawal rate: More money than you started with. 💰💰💰 If you have solid returns upfront, then you gained a decade of priceless freedom! For retirees of the “Class of 2011”, consider that their portfolio is likely larger today in 2021 even after a decade of withdrawals.

Retiring in 2021? Crystal ball is cloudy. If you are in the retirement “Class of 2021”, many predictions call for another lost decade. Yet, even if the next 10 years have poor returns, better times may be right around the corner. From this article by Davis Advisors:

Though frustrating, stretches of disappointing results for the market are not unprecedented. History shows however, that these difficult stretches have been followed by periods of recovery. Why? Because lower prices increase future returns. – Christopher Davis

This article was written in 2012, and it turns out that Davis was right. As of Q2 2021, the trailing 10-year annual return of the S&P 500 is over 12% annualized. Here is a chart showing the subsequent 10-year performance after each past “lost decade of stock returns”.

Surviving the first 10 years of retirement. The lesson here is to avoid taking out big withdrawals during a stock market slump drop during the first 10 years, so that it can benefit from the rebound of the next 10 years. At the same time, you don’t want give up the chance of 10 extra years of freedom. Therefore, perhaps the best bet is to retire when you have a reached your chosen savings target (for example, 25 times annual expenses), but also maintain a detailed backup plan during the first 10 years. Here are some things you might include in that plan:

- Plan ahead for way that you can temporarily cut back on spending if you need to. Big to small. For example, plan to move to a lower-cost city, country, or housing option.

- Identify non-essential assets that you will sell if you need to. Vacation property, etc.

- Maintain employment opportunities in your current career field. Go back to part-time, freelance, consulting, etc.

- Have alternative employment plans in a different career field to create supplemental income.

(By “plan”, I mean written out on a piece of paper. This improves the clarity of your thinking.)

The most powerful way to counter “sequence of returns risk” is variable withdrawals – a fancy term for the brilliant idea of not taking out as much money from your portfolio when it is getting beaten down. But the first 10 years is the most important, and the first 10 years is probably the easiest to go back to the workforce in a limited capacity.

Bottom line. Deciding when to stop working can be a difficult, personality-driven decision, but one option is to retiring with 95-98% odds of success with a practical backup plan, rather than waiting several more years and reaching 99.5% odds of success. Accept that luck matters (and also that you might have to go back to work). However, you also might gain extra priceless years of freedom. Life is never 100% certain anyway.

The Best Credit Card Bonus Offers – May 2024

The Best Credit Card Bonus Offers – May 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - May 2024

Best Interest Rates on Cash - May 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Agreed. Most retirement planning, advice, websites, charts, predictions, algorithms, products ad infinitum downplay the role of luck. In fact, almost everything ignores the luck component.

Timing and luck play a huge role. I had neighbors who were not planning to retire yet who, when COVID hit, were forcibly retired early by their employers. They were the most expensive employees to pay to “do nothing”, so they were let go. Others are holding on a few more years hoping for things to recover. Who knows what will happen? Timing and luck matter, no matter how well you plan.