Common retirement planning advice tells you to plan on replacing 70-80% of your pre-retirement income. However, this Financial Post article argues that number may be closer to 35%. Article found via k66 of Bogleheads.

Essentially, the author segregates your income to “regular” spending and temporary “investment” spending that won’t continue into retirement. Regular consumption includes food, transportation, home and car maintenance, and insurance. Temporary spending include a mortgage, child-related costs, work-related costs, and retirement savings. The idea is that in retirement your house will be paid off and your kids will be financially self-sufficient, so those “investment” expenses will go away and you’ll need less money than you may think.

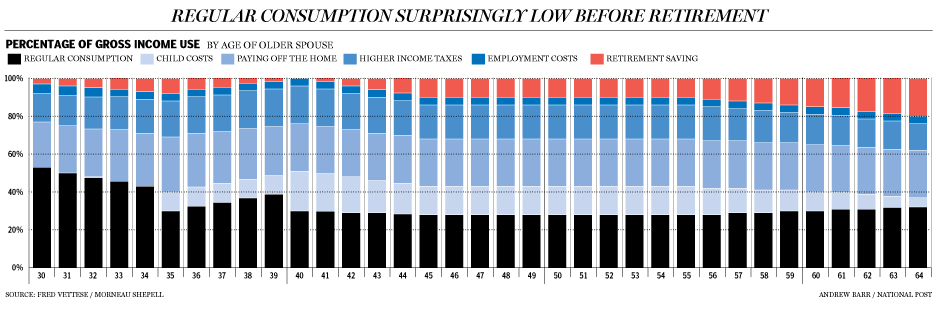

Here’s an illustration of how this would break down for a theoretical couple that bought a house at 30, had kids at 35, and retires at 65.

(click to enlarge)

Now, it’s easy to get hung up on how this chart doesn’t accurately reflect your life. It’s not supposed to! Instead, imagine for yourself what this chart might look like for your situation. For example, my parents definitely kicked up their savings rate post-kids and pre-retirement. For us, we had our highest savings rate pre-kids. You may need 20% of your current income, or you may need 80%. This is one place where a rule-of-thumb just isn’t useful.

I would note that the article doesn’t really mention health insurance or other health-related costs, possibly because it is a Canadian newspaper. Also, young people in the US probably spend at least a few years paying down college loans. Finally, some folks will need to account for new post-retirement spending that might pop up like travel and other costly recreational activities.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Obviously these theoretical kids got some pretty awesome college scholarships. Child spending most definitely spikes when they go to college.

The article is basically correct. I retired two years ago, and our spending is about 35% of per-retirement income. I would go one step further, and say that when planning for retirement, you should ignore your per-retirement income entirely, and estimate your post retirement spending from scratch.

Per the chart, our household is around 36 or 37. Conceptually, it’s pretty spot on. As we prepare for a second child, it is hard to see how we will maintain the same retirement savings rate (about 17% of total household income, including matches). It will likely be crowded out by daycare (x2), our student loan payments, new life insurance policies, the second 529 account, etc. I’m having a hard time letting go of the retirement contributions though, as I don’t want to miss out on the compounding! (We will surely continue to save enough to fully utilize the matches.)

I think the 35% may be a bit too low for a lot of families. If median income for a family is $50k then they’re saying that a retired couple ought to be able to live off of $17,500 a year? Thats not much.

Like you say, many of my clients end up spending less than than the ‘typical’ 70% used by most financial planners. I’ve been in the industry for almost 20 years and am a certified planner, but it seems the industry has consistently used unrealistic numbers. For instance, most financial plans are based on assumptions that you will earn average historical rates of return. When those returns on based on the best 30 years the stock market has ever seen you get some pretty skewed numbers! Many plans are projecting a 10% return still when interest rates are extremely low. So it makes it even more important that people not only use a more realistic withdrawal rate but also a more realistic rate of return.

This reminds me of the difficulty in modelling spending when using retirement calculators.

I was puzzled when I encountered the “Bernicke’s” spending model option on the popular online retirement calculator firecalc.com. This option decreases projected spending after age 56 as you get older at a rate I found alarming – it appears to put you at less than half your original annual spending by age 76!

I always dismissed that option as unrealistic when using the calculator and instead opted for the “constant” spending model. After reading this blog post, I’m thinking maybe there could something to the Bernicke model after all?

Also note in the article that the “real life example” (which the chart is of) is of a “higher income couple”. Without knowing what that is and what the housing cost reference is (or medical for that matter), the “35%” number is just another pop-finance red herring headline.

There are also a lot of assumptions in pop-retirement planning that each year one just gets an inflation adjustment. I think that misses the point that most people want to improve their lot over time. Living for 30 years in retirement at the same inflation adjust level I am now is not very appealing…especially if one has ratcheted down to save for retirement in the first place! Everyone really has to work off their own numbers and situation.

Dan and Thad make excellent points. And Thad’s last sentence is really what we all need to take to heart “Everyone really has to work off their own numbers and situation.”

Taking that a step further, no one knows for sure what will happen in the future–what type of economy we will have, how high or low inflation might be, what will happen to SS and Med. There are simply too many variables to model. My approach, instead, is to stress-test a retirement income plan to see where the strengths and weaknesses are. That way you can have an idea of how it will react in different environments and plan accordingly. For instance, if a low-inflation/slow growing economy occurs I will do X; whereas if a high-inflation, slow growth economy occurs I will do Y. There are few things that you can control, but one thing you can do is have a plan that takes into account the various possibilities. Great discussion!

Just to clarify my previous comment – By saying the article is “basically correct”, I mean that everyone needs to determine their post-retirement income needs, and it will not necessarily end up being 70-80% of per-retirement income (the number that so many “retirement calculators” assume). The fact that that percentage, for me, came out to about 35%, is just a coincidence. No-one is saying that 35% is the new target. It might be for some, but everyone must plan their own, as several have said.

For those who live below their means before retirement, the number will be smaller, and vice-versa.

It’s highly questionable that an average couple would buy a house at 30, and get kids at the age of 35. In real life there would be something different: perhaps first child in their late twenties, then lot of debts and only small portion of lucky folks would manage to get its own house.