I invested $10,000 into person-to-person loans in November 2012, split evenly between LendingClub and Prosper. It’s been a little over 9 months since then, so I wanted to give a detailed update in addition to my brief monthly updates. The primary goal of this portfolio is to earn a target return of 8-10% net of defaults, but I also wanted to see if there were significant differences between the two competitors Prosper and LendingClub.

I invested $10,000 into person-to-person loans in November 2012, split evenly between LendingClub and Prosper. It’s been a little over 9 months since then, so I wanted to give a detailed update in addition to my brief monthly updates. The primary goal of this portfolio is to earn a target return of 8-10% net of defaults, but I also wanted to see if there were significant differences between the two competitors Prosper and LendingClub.

I’m also considering liquidating both portfolios after 12 months have passed. I’m getting a little bored with the experiment, and having to sell the loans would also allow me to compare the ease of selling either company’s loans on the secondary market.

Portfolio Credit Quality Comparison

I wanted to keep these portfolios comparable in terms of risk level, while still trying to maximize overall return net of defaults. Peter Renton of LendAcademy made this helpful chart comparing estimated defaults rates with their respective credit grades. Since each company has their own proprietary credit grading formula, they don’t match up perfectly.

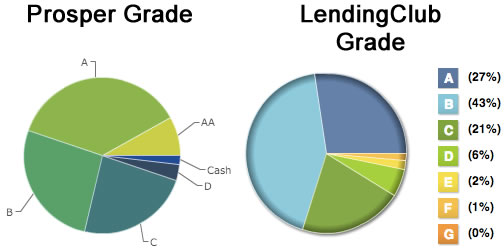

Here’s my portfolio breakdown:

With LendingClub, the dollar-weighted average interest rate is 12.24%. In terms of credit grade, 91% were in the top 3 grade (A, B, C). 97% were in the top 4 grades (A,B,C,D).

With Prosper, the dollar-weighted average interest rate is 14.05%. In terms of credit grade, 73% were the top 3 grade (AA, A, B). 97% in top 4 grades (AA,A,B,C).

In general, the Prosper portfolio appears to be slightly more risky but also has a slightly higher average interest rate.

(Side note: Why slightly more Prosper notes than LendingClub? Prosper’s automated Quick Invest feature makes it faster and easier to reinvest your money. LendingClub takes a little longer and often the loans that I want to invest in don’t end up funding so the money gets put back into my account uninvested. Since I only check up on this account once a month, this results in being less fully-invested.)

Portfolio Late Loan and Default Rate Comparison

As you can see with this older reference chart from Prosper back when they had lax credit guidelines, default rates tend to rise consistently throughout the holding period, with a slight tapering off near the end of the loan period. I am only including this to illustrate overall trends, not specific default rates.

With LendingClub, so far I have invested in 257 loans. 232 are current, 22 were paid off early, 1 is 30+ days late, none are 30+ days late, and 2 were charged-off. That means 1.2% (3/257) were 1 month late or worse at this point.

With Prosper, so far I have invested in 267 loans. 239 are current, 19 were paid off early, 1 is under 30 days late, 6 are 30+ days late, and 2 were charged-off. That means 3.0% (8/267) were 1 month late or worse at this point.

Portfolio Adjusted Value Comparison

Based on past history, I adjust my loan principal by conservatively assuming that all loans that become 30+ days late will default. Sometimes loans will go from late back to current (plus possible late fees), and sometimes there will be some additional money recovered on charged-off loans.

With LendingClub, I had $4,920 in loans and $405 in cash as of 8/11/13. $21 of late loans gives us an adjusted balance is $5,325.

With Prosper, I had $5,299 in loans and $94 in cash as of 8/11/13. $129 of late loans gives us the adjusted balance is $5,264.

Here is a historical chart of the adjusted balance of LendingClub vs. Prosper. I had to adjust some values due to the fact that LendingClub reports accrued interest while Prosper does not.

At this point it is still too early to draw any conclusions. Your results may be different from mine. But for now, both portfolios are returning a positive return on the order of 8% net of fees. I tend to like Prosper’s website better, but in terms of relative performance Prosper is a currently behind LendingClub in terms of having more late loans in the pipeline than can be compensated for by the higher average interest rates being charged.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

This is interesting. I am new to this and hope you don’t discontinue your experiment because a real life case study will help a lot of people decide whether they want to undertake this. Of course, it is your money!

Are there any origination fees in these loans that go to the lender (not the platform)? Also, how timely is the tax reporting from the platforms–do they report interest income before April 15th or do they cause you to get an extension? Also, when one of these loans goes into default, is there any recovery or are the defaulted loans a total wipeout? What kind of collections efforts do the vendors have, or do they just rely on the idea that defaulting will hurt the borrower’s credit rating?

Thanks.

I’m very interested in this experiment. Would you consider running it for a few more months please.

Also, I’ve looked to the PF blog community and haven’t found an answer yet, are you aware of anyone that has invested hundreds of thousands in Lending club? I’m currently earning 9.44% with 20k invested, nothing late. I’m just waiting for it all to come crumbling down with defaults.

@John Wilks,

I’m interested in this too. I had not considered investing in any of these services before this most recent post, but I’m very intrigued by Lending Club. I’m actually thinking about putting ~$20k in as a test, and hopefully not losing my tail.

My main concern was that both LC and Jonathan recommend investing in a lot of small loans to minimize risk. Makes perfect sense, but how time consuming is picking these loans?

Do you have any recommendations or strategies?

Very time consuming. I Set filters to only provide safe loans. Then I check every half an hour. With there were automatic investment options.

I’ve invested in Lending Club since 2009 and have had pretty good return so far. I only have ~$7k in there now as I’ve been treating it as an experiment. $5800 deposited over time, and $1573 in interest, with all of it being reinvested currently. I’m not trying for a fantastic return but its definitely better what I’d get from a CD or savings account.

The breakdown of my loans: I’ve had 558 total, 5 in funding, 402 issued & current, 131 fully paid, 2 in 31-120 days late status and 18 that have been charged off. I prefer B grade loans (51.7%), then A (36%), then C (11.3%).

I’m careful on what types of loans I pick. Only 3 year, no delinquencies, 2 years min employment, originating in my state if possible. I prefer debt consolidation or home improvement loans over those for wedding or business – with the 3 year time period the marriage or business could be finished before the loan is paid off.

Thanks for the write up. I have about $15k in Prosper and same in LC, over the last year or so. I tend to stick to 36 mo loans and prefer high int rate B’s, and all C, D, E…. excluding business loans or vacations and so forth… I just dont want to loan someone $$ to go on vacation 🙂 Anyway, I am seeing similar results as you generally, so it is good to see that your facts and details pretty much validate my general results (I havent analyzed to the degree you have, so thank you). I’d be VERY interested your experience in selling notes in the secondary market. Im not sure I quite understand the best practices in terms of selling my notes (and pricing them, etc). Or buying notes on secondary market for that fact. I have FolioFN setup but havent used it.