![]() When I first reviewed JemStep in 2011, it analyzed your current portfolio and made customized mutual fund rankings. Flash forward to 2013, and they’ve moved into the portfolio management and advice space, similar to previously-reviewed sites like Betterment or Personal Capital. Now it’s called Jemstep Portfolio Manager.

When I first reviewed JemStep in 2011, it analyzed your current portfolio and made customized mutual fund rankings. Flash forward to 2013, and they’ve moved into the portfolio management and advice space, similar to previously-reviewed sites like Betterment or Personal Capital. Now it’s called Jemstep Portfolio Manager.

After signing into my old account and looking around at the new features, I was happy to see they’ve actually gotten pretty close to my wishlist:

- Import my existing portfolio directly from broker. Check.

- Track asset allocation across entire portfolio. Check.

- Customized rebalancing alerts. Not quite. They do give rebalancing alerts, but only customized to their portfolio recommendations, not my personal chosen preferences. See below.

- Detailed performance stats vs. benchmarks. Incomplete? I don’t see this, but I haven’t be able to get past the trade recommendations.

- Reasonable cost. During their initial beta, the service will be free for everyone until March 1st, 2013. After that, the service remains free for those with assets of $25,000 or less. Otherwise see fee schedule discussion below.

Test Drive

The first step is to set a goal. They want things like age, income, target retirement age, risk tolerance, etc. You have provide a preference of mutual funds or ETFs. Given their previous support of actively-managed funds with high recent risk-adjusted returns, I was surprised to see the following:

Jemstep recommends index funds for most investors. Please check this box if you would like Jemstep to also include active funds in its analysis.

I indicated that I was a conservative 35-year old who wanted to retire at age 50 and preferred index ETFs.

After that, they want to see your current portfolio holdings. You can have them import your holdings by providing your login credentials to most financial providers, for example TD Ameritrade, Vanguard, Fidelity, etc. You can also add your holdings manually. For simplicity, I manually input a sample portfolio that was roughly similar to my current portfolio, using round numbers like a $1,000,000 total value and 70% stocks / 30% bonds split.

35% Vanguard Total US Stock Market Index (VTI)

35% Vanguard Total International Stock Index (VXUS)

15% Vanguard Total Bond Index (BND)

15% iShares TIPS ETF (TIP)

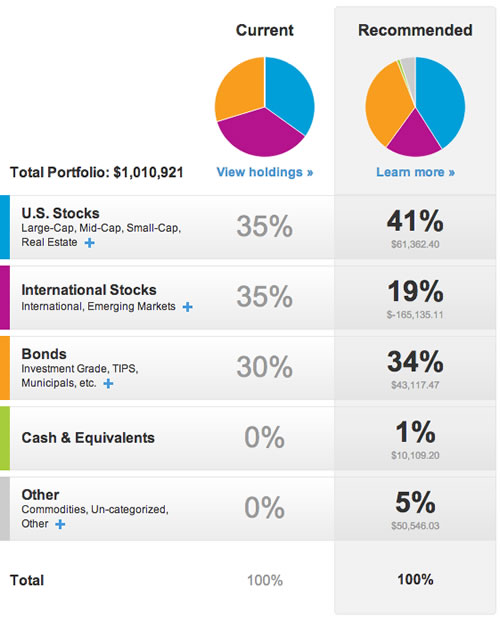

Next, a recommended portfolio is generated. Mine was roughly 60% stocks, 35% bonds, 5% commodities:

35% US Stocks (mid-cap tilt)

6% US REIT (originally included as US stock)

19% International (68% international/32% emerging)

35% Bonds (treasury, corporate, mortgage-backed)

1% Cash

5% Commodities

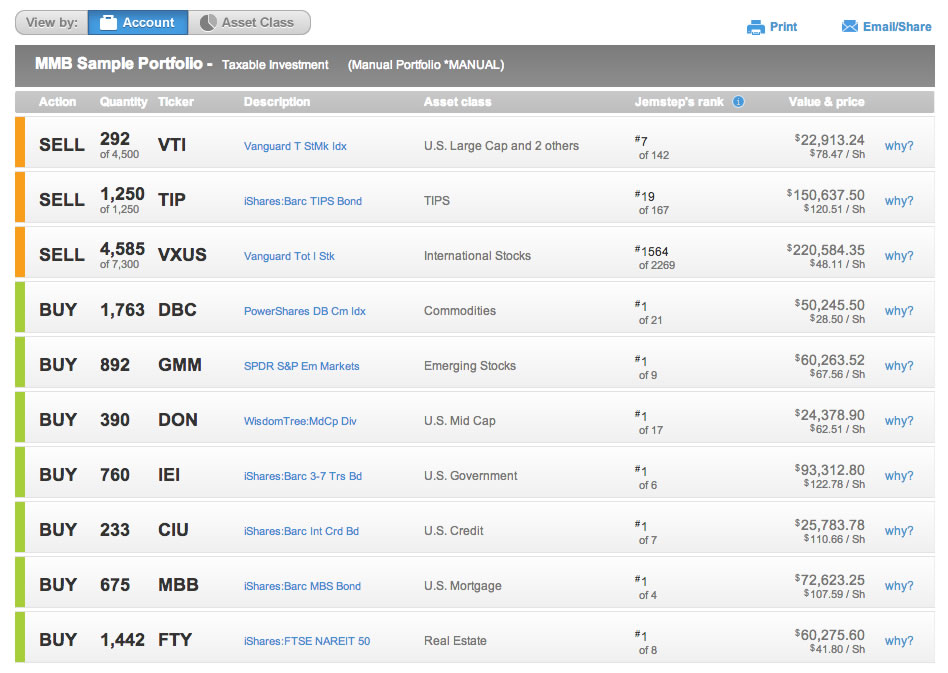

Finally, they provide specific buy and sell instructions, complete with number of shares to trade. Here’s a screenshot that also includes the ETFs that they recommended.

(click to enlarge.)

(click to enlarge.)As you can see, their index ETF recommendations are still based on their previous Jemstep ranking system, which still takes into account past performance even though they are passive ETFs, and thus you may not necessarily by buying the cheapest ETFs. However, the real benefit of Jemstep may be to those folks currently with “financial advisors” that quietly place their clients in inferior funds because they are in-house products or other business arrangement. With Jemstep, at least they’ll see that their fund is both expensive and performs poorly relative to other options.

I did find one possible error. Jemstep’s software not seem to recognize that my holding of VXUS (Vanguard Total International ETF) is already 24% emerging markets, and categorized the entire fund as “international stocks” which believe is actually “developed international stocks”. I tested this by replacing VXUS with VEA, which only holds stocks from developed markets in Europe, Asia, and Australia… same result of “international stocks” and same buy/sell recommendations. Therefore, the instructions to sell a chunk of my VXUS to buy GMM (SPDR S&P Emerging Markets ETF) may not be necessary.

Otherwise, I would say that in general the recommended portfolio fits in within the boundaries of current, popularly-accepted asset allocations. They chose to add US REITs and commodities exposure, but no special allocation to gold (there’s a bit of gold futures in the commodities ETF).

Fee Schedule Analysis

Jemstep’s Portfolio Manager service charges a flat fee per month depending on the value of your retirement assets. (During their initial beta, the service will be free for everyone until March 1st, 2013.) Here’s a screenshot:

(Note: If you pay upfront for an entire year, you get 2 months free or 16.6% off)

The tiers are set up a bit awkwardly, in my opinion. Traditionally, fees are expressed as percentage of assets on an annualized basis (on top of the expenses from underlying investments). Viewed in this manner:

Up to $25,000, there are no fees.

$25,000-$150,000 in assets, fees are $17.99 per month, or between 0.86%-0.14%.

$150,000-$300,000 in assets, fees are $29.99 per month, or between 0.23%-0.12%.

$300,000-$600,000 in assets, fees are $49.99 per month, or between 0.20%-0.10%.

$600,000+ in assets, fees are $69.99 per month, or starting at 0.14%.

So while your fees do only rise along with your assets, on a percentage basis you’d be paying more at $305,000 in assets than at $110,000 in assets. Also, it’s not really clear why they have to charge more when your assets rise. They don’t hold your assets in a custodial account, you’re still with your own brokerage and making all the trades yourself. The computer doesn’t have to work any harder to crank out the buy and sell recommendations when there are more commas involved.

That said, a million dollar portfolio would only be paying a flat $840, or 0.084%, or 8 basis points. Actually, if you’ve got a million dollars, you could commit to a year upfront and then you’d only be paying $700 a year, or 7 basis points. So the sweet spots are the small portfolios under $25,000 which are free, and larger portfolios. As always, you could do the ongoing rebalancing yourself if you were willing to spend a few hours a year with a calculator. But the point of these services is to provide value for the people who don’t want to DIY.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Johnathan,

This seem somewhat similar to Vanguard’s target asset mix tool where you can answer their questions and you’ll get a portfolio distribution recommendation – which you can apply to your vanguard assets to help you with rebalancing.

I’d be interested in your opinion – how does Jemstep compare to Vanguard’s free automated advice?

Hi Jonathan,

Thanks for your review of the new Jemstep Portfolio Manager. As always, we appreciate it and hope the service proves to be of real value to your readers.

I just wanted to comment quickly about the rationale behind the pricing. You are correct that typically such services are expressed on a percentage basis of assets under management. However, we did some user testing and users felt more comfortable actually knowing the Dollar amount upfront, and so we set a fixed fee depending on level of assets.

Setting pricing tiers like we have done has the unavoidable effect you described, where the percentage AUM could in a few instances be higher for a higher level of assets, but has the benefit of certainty and works well for users across the board, being a fraction of the cost of wealth managers and lower on average than other alternatives we looked at.

The service is aimed at helping people lock in more money for retirement and with the pricing structure set at these competitive levels, we hope readers will give the service a whirl and let us know what they think. All feedback is welcome and helps us continually refine the service.

Kind regards,

Kevin

Joint CEO, Jemstep

Always nice when the CEOs comment on things…

This appears to be a niche service for people who have their money tied up at multiple providers either because of 401Ks or some other reason.

It seems more logical to move all your money to a service like betterment or wealthfront, where you can get a portfolio that rebalances FOR you for a mere .15% to .25%.

Jemstep is removing some of the work, but unless it goes all the way and makes the trades automatically, you are just paying a lot for something you can do with a free google spreadsheet.

Also, I would add that these generic asset allocations these providers try to fit you in are not optimal.

I’m not one for market timing, but any “suggested allocation” for an older person typically recommends an aggregate bond fund. Anyone holding long-term government bonds right now is crazy… All these pre-fab allocations are giving you really poor investment advice. (Bonds are fine, just keep ’em short term and TIPS like Jonathan does…)

@Ace – Do you have a link to that tool? I don’t know exactly which tool you’re talking about, but from what you are saying Vanguard will provide you an asset allocation (AA). Target asset allocations are pretty easy to find free all over, and it’s not always easy to know which is better (well, it’s impossible to know, but it’s hard to decide on one over another).

But what Jemstep does additionally is determine your current asset allocation in real time, and also tells you exactly what to buy or sell in order to reach their recommendation AA. These may seem trivial, but that and the additional step of doing the trades for you are actually pretty critical as people tend not to do these things, especially in boom and bust periods.

@Kevin – As always, thanks for your reading and your quick response. I understand your point of view. I just wanted to do the conversions for my own edification and for comparison with your competitors which do charge on a percentage basis.

@Maury – I agree, I would love to see a service that takes into account your entire portfolio using account aggregation tools, AND manages all the money it can for you in a custodial account.

Jonathan-

Isn’t that more or less what Personal Capital is supposed to provide? They use (I believe) Yodlee’s aggregation services, and they’ll manage your portfolio for you a fee — across multiple accounts. In my case they weren’t able to manage the 401k’s my wife and I have, but they encourage you to consolidate remaining assets into an account that they manage.

I went as far as talking to one of their advisers, but the fact that they suggested pick individual stocks for their US holdings made me somewhat nervous. Plus, truthfully, I am interested enough in this subject that I already take an active roll in tracking and periodically rebalancing our portfolio.

Cheers,

Ben

@Maury Thanks for the feedback. I’d like to highlight a couple of key points in response to your comments which hopefully also help other readers gain a deeper insight into our new service.

– Jemstep’s service is aimed primarily at those investors who still want to retain some control over their investment portfolios. We developed the service in a way that allows them to keep their investments in their existing accounts and they do not have to transfer the assets to Jemstep. Importantly, liquidatIng your holdings to transfer them over to, say, Betterment, could result in a big tax bill. This is averted with Jemstep and our recommendations take all of your existing holdings into account.

– Our allocations are more personalized than meets the eye. For example, inherent in our asset allocations are personalized glide paths – the transition to a more conservative allocation over time – which depend on a user’s age, starting assets, savings and risk profile – all optimized for poor market conditions.

– Our recommended buys and sells take into consideration fund quality (comparing over 50 different attributes of every fund) and fees, plus your own tax situation: we consider your cost basis and quantify your capital gains or losses. We also ensure you are holding the right assets in the right type of account (taxable vs tax advantaged).

– Finally, when it comes to bonds, we don’t recommend long term bonds. All of the recommended bond funds have a duration of approx. 4 years or less. and for older more conservative investors we include a relatively heavy weighting in TIPS.

In an effort to simplify the user experience for our users and make the service easy to use, much of this is not readily apparent but I hope this brief note serves to highlight some of the depth behind our recommendations

@Ben – you are correct that with Personal Capital, you transfer your assets to them to manage – this is similar to a traditional wealth manager and more suited for people who wish to wholly delegate the management of their portfolios to a third party. Jemstep helps you self-manage all of your accounts (including your 401(k)) by giving you the exact list of investments that you should buy and sell in each account – all of this happens online and you need not speak to an advisor or transfer your assets out of your existing accounts. The services are pretty different and both work well for different types of investors.

@Jonathan – just wanted to circle back to you on the review and say that the items on your wishlist are very much part of our ongoing roadmap. Detailed performance stats vs benchmarks are currently available on the website at the fund level and is on the roadmap for the portfolio level too. Would love to speak more about some of your other points and ongoing refinements in the works- might be worth emailing you rather than clogging up this space more than I already have:)

Thanks again to everyone – we are passionate about this space, so the feedback is appreciated!

Kevin

Joint CEO, Jemstep, Inc.

Where is the value received in the ongoing fee? Does Jemstep send email blasts when recommendations change?

@Evan – much of the value is derived from periodic rebalancing to make sure you stay on track with the recommended portfolio. We send email alerts (and alerts on your dashboard) at least on a quarterly basis to show users the optimal “buys” and “sells” to rebalance effectively. We also update our recommendations if users change their profile, add more funds or accounts etc. In essence, we monitor your profile, portfolio and the market to make sure your portfolio is optimized.

The second aspect relates to the “glide path” embedded in our recommended portfolios. As users get closer to retirement, our portfolios automatically transition them to a more conservative portfolio – we similarly send alerts as to how to modify the portfolio to achieve this in the most tax efficient, cost effective way with the best quality funds.

The fees do not appear to have gone into affect on my account…is there a cut-over period or am I going to be billed if I don’t cancel?

@James The fees have not gone into effect yet and the service will continue for free until we are out of the “beta” period, which will probably last another 2 weeks or so.

In any event, you won’t be billed unless you have explicitly signed up for Premium Services with your credit card, so no need to worry about that:) The credit card completion process will only go live once we are out of beta and are charging for the service.

Hope that clears things up for you.

Regards,

Kevin

Joint CEO, Jemstep

The concept is nice and it has been there in one form or another since ages. But the real issue is that average investor is an arm chair investor and NEVER self motivated to DIY. Its like your new year resolution, Jan 1, exercise/diet/weight loss. March onwards, you are making a profit for the 24hr fitness as you never show up.

My real question is for the money being charged (and its a lot of money if you have 500K+), what extra things Jemstep can do which other free sites/advisors such as Vanguard/Fidelity etc are not providing. BTW, Fidelity also has a very good tool and so does JPMorgam with financial engines (atleast used too – but I have not seen it lately).

For the money being charged, which looks like a lot like AUM kinda fees (and as someone mentioned, the computer is not doing any extra work just because the account has extra zeros in it), can Jempstep go and above beyond then simply sending an email per qtr (really ?? just one .. for that money being charged??).

May be organize a subscriber meet in cities, go their home and beat some sense into them ??

My experience with Jemstep is that it is inconsistent in pulling account information from retirement accounts. When I refresh my accounts in Jemstep, one account assets has varied over 80%. This, in turn, triggers an asset allocation rebalance.

On another 401K account, Jemstep recommends selling Funds “Wells Fargo..Fund” and “JPMorgan..Fund” and “buying the lowest cost U.S. Diversified Bonds fund in this account.” Isn’t that what Jemstep is supposed to do – recommend specific buy/sells?

I realize that I could manually input the data but that somewhat defeats the purpose of automation.

Jemstep support is working on the first issue and is very responsive. I like and see value in the model but the inconsistent operation of the software is a bit unsettling – especially at the current prices.

Marc – I’m glad our support team is on the issue, and I am sure it will be resolved soon. Regarding your 401k, Jemstep has a growing database of investment options for over 70 well-known companies. If your company plan hasn’t yet been listed on Jemstep, the facility exists for you to manually add the investment choices in your plan (one time only) and Jemstep will instantly tell you what to buy and sell to optimize your 401k account as part of your broader portfolio – and will continue to monitor the account for you. You can also email or fax the plan options to Jemstep and we’ll upload it onto the system.

Regards,

Kevin (CEO)

I like Jemstep compared to some of the other sites since it doesn’t ask me to transfer my money. That said, this is my 3rd attempt to aggregate my external accounts and the feature just doesn’t work. It takes a really long time for the account add process and most of the times it fails. Do others have similar experiences??

I’ve used Jemstep for about two months so far. In terms of initially aggregating the accounts, it did take some time to properly reflect each account and timed out on a few accounts initially (we have about 6 accounts with two different brokerages). They were very helpful over online chat and it was resolved before I researched then followed the buy and sell recommendations. Since then, the daily holdings it reflects for each account have sometimes slightly lagged behind what my brokerages show by a half day or so (for mutual funds amounts rather than ETFs). Usually the refreshing is fairly quick, but I will double check after depositing new funds/when they send me an email to rebalance that everything is in sync before acting on the recommendations.

Nitin – I’m sorry to hear you’ve been having issues with the account aggregation component. Please will you email support@jemstep.com and they will contact you to help you through the issue. I have asked our support manager, Leena, to look out for your case and give you assistance.

Kate – thanks for the response.

Kind regards,

Kevin

CEO, Jemstep