![]()

Update. I’ve done a significant amount of my banking with Ally for years (checking, savings, and multiple CDs), but the “gateway drug” for me and probably most people will be their Ally Online Savings Account. You can use this savings account as a companion account to your existing primary checking account (perhaps at Chase, BofA, Wells Fargo, etc), or as a companion to the Ally Interest Checking account.

The Ally Online Savings Account has no minimum balance, no monthly fees, and currently pays 1.45% APY (as of 4/2/18). Their interest rates may not be the absolute highest, but they have consistently been within 0.10% of the temporarily top banks, making it not worthwhile to move my money. (See my rate chaser calculator). Let’s go through the important factors.

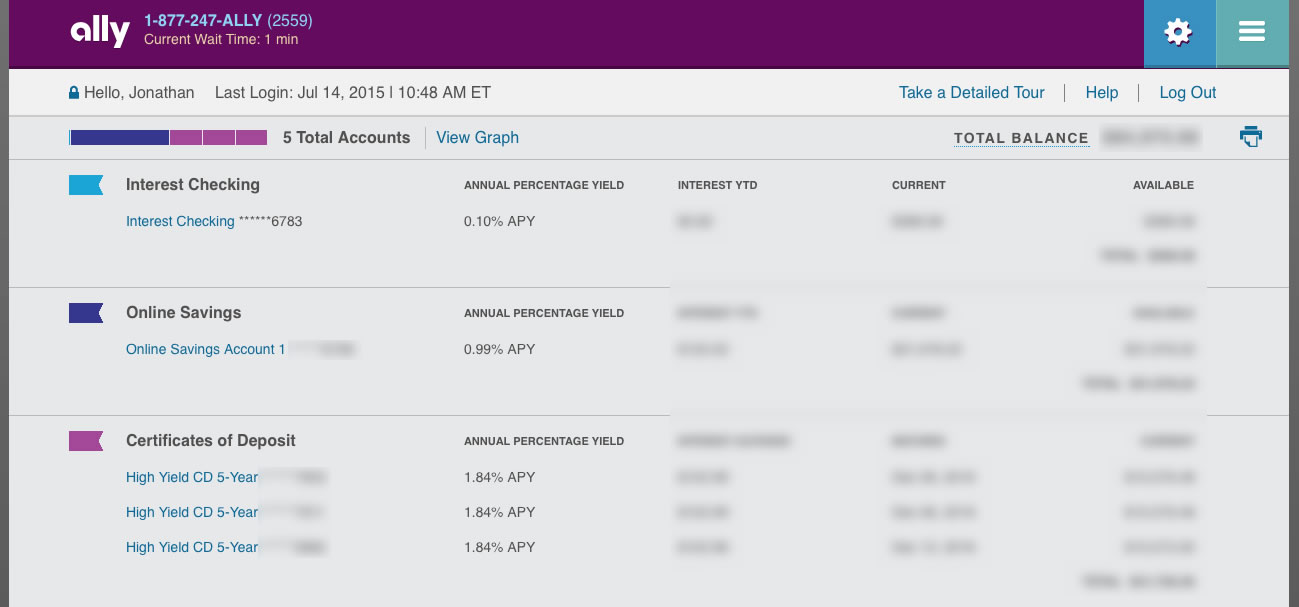

User Interface. Below is a screenshot of the main page after logging in (click to enlarge). I can see all of my accounts and their balances at a glance. The overall design is clean and minimalist, and it was recently updated to be more mobile-friendly.

Customer Service. Ally Bank differentiates itself with their customer service. First of all, they are available 24/7 at 1-877-247-ALLY (2559). When you use their smartphone app or log into their website, you can see the wait time beforehand. Even better, if you don’t want to call them you can just use their Live Chat feature.

Security. Ally Bank supports two-factor authentication with security codes sent via either e-mail or text message. They ask for a security code when you log in from a computer they don’t recognize. However, if you’ve logged into that computer before with a security code, they may not ask you again and you can’t choose to have two-factor authentication to always be in effect.

Awards. Ally Bank was named “Best Internet Bank” and “Best for Millennials” by Kiplinger’s Personal Finance Magazine in July 2017. Ally Bank was named “Best Online Bank” for the 5th year in a Row by MONEY® Magazine in 2015.

FDIC Insurance. Ally Bank is a member of the Federal Deposit Insurance Corporation, FDIC Certificate #57803. As with other FDIC-insured banks, this means your Ally deposits are insured by the FDIC up to $250,000 per depositor, for each account ownership category.

Funds Transfers. With no physical branches, online savings accounts should have maximum flexibility as they are often secondary accounts (given most megabank checking accounts pay either no interest or a sad 0.01% APY). Ally Bank allows you to link any other external bank account using the standard routing number and account numbers. As long as you initiate the transfer before 7:30 pm Eastern Time, transfers both in and out are free and can take as little as 1 business day. You can link up to 20 different accounts (it used to be unlimited; but other banks limit to 3 or even just 1). This is about as good as it gets for online banks. Here’s their updated timing chart (see details here):

The transfer limits are also relatively high. On my accounts, I see that I have a $150,000 daily limit outbound and $250,000 daily limit inbound, with a total monthly limit of $600,000 outbound and $1,000,000 inbound. Keeping in mind that all savings accounts from any bank are limited to six withdrawals per month.

ATM Debit Card. You don’t get a debit card with their Online Savings Account. You can get a debit card with either their Checking or Money Market accounts, but note that those have lower interest rates.

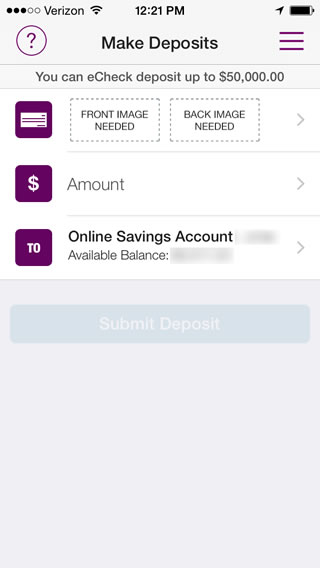

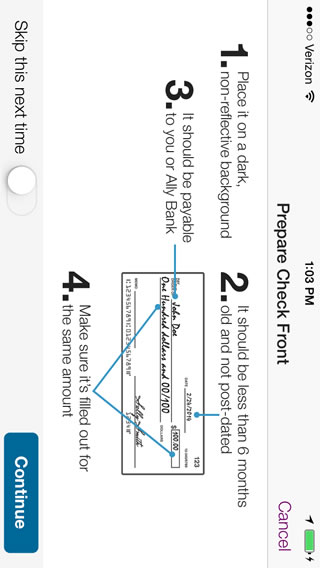

Mobile check deposit. You can use the Ally smartphone app to deposit checks using your smartphone camera. (This is in addition to using your computer scanner and/or free postage-paid deposit envelopes.) I’m not sure if this is the same for everyone, but my deposit limit is $50,000 which is higher than many other electronic deposit programs. I’ve used the app to deposit multiple checks without issue. Screenshot below.

Mobile app. Available for iOS and Android… you can do all the important stuff – see transactions, transfer funds, deposit checks, pay bills. It can remember your username, but you must type in your password every time. I usually just use my Personal Capital app for checking balances. The overall design is acceptable, and the ATM locator is helpful if you have the Ally Checking account with free AllPoint ATMs and $10 in fee rebates each statement cycle for any ATM.

Details

- Interest Compounding: accrued daily, compounded daily, credited monthly

- Minimum to open: $0

- Minimum requirements to avoid monthly service charge: None

- Number of external bank account links allowed: 20

- Routing Number: 124003116

Bottom line. The Ally Online Savings Account is a solid offering with with no monthly fees, no minimum balance requirement, and a historically competitive interest rate. Additional features like a flexible funds transfer system and solid 24/7 customer service help differentiate themselves from the competition. It works fine on its own as a “piggyback” or companion account to your existing checking account.

You can also combine it with the Ally Interest Checking Account (my review) which offers ATM fee rebates (up to $10 per statement cycle), free online billpay, and the ability to use the savings account as a free overdraft source. Ally also has certificates of deposit which offer competitive rates at times.

The Best Credit Card Bonus Offers – May 2024

The Best Credit Card Bonus Offers – May 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - May 2024

Best Interest Rates on Cash - May 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

In my mind Ally’s only downfall is their very temperamental mobile check deposit feature, my other banks use industry leader Mitek for their mobile check deposit while Ally continues to use a finicky homegrown solution that repeatedly rejects images.

Interesting comment. I have tried them along side two other banks that offer check cashing through the mobile app, and I have found Ally to be the easiest to use. That does not mean they are the best when compared to all others, but they are my go-to when depositing a check, especially tough ones (i.e., checks that look like mail/postcards).

Have been using ally since the time they were gmac bank. It’s the best account I have. The unlimited external account linking is a HUGE benefit. They’ve also consistently been among the top interest rates.

I also give high marks to Ally. They are the only online bank I still use from the heydays of 4%-5% interest rates on Money Markets and CDs. Though I do find it humorous or depressing, going on 5 years now to see them touting 1.5% interest rates as if its something to get excited about as about to enraged. We can thank Janet Yellen, Ben Bernanke and our friends on Wall Street for that.

Big fan of ally bank. Unfortunately the same can not be said of them about me. They have shut down my two savings accounts. I had been making many transfers between banks moving money around…far more than average person, but nothing illegal. Their customer service was great, until the shutdown… where they did the usual tricks of delaying the 30 day notice of the shutdown, refusing to give out even basic answers (like can I open a checking account with them) and so on.

Just curious, but what reason did Ally give you for shutting down your savings accounts? And why so many transfers between banks?

Ally didn’t give a reason. Banks almost never give reasons, just 30 day notices. I wasn’t expecting a reason, but I was hoping they’d at least tell me if I could open a checking account with them (I didn’t know if they were unhappy with the savings tranfers, or the transfers in general).

All of the transfers were due to manufactured spending. Basically depositing money orders in other bank accounts, transferring them to ally, and transferring them out of ally to the bank where I’m purchasing them. I thought ally was a pretty safe cog in the wheel, but apparently I was wrong.

Just wanted to add a quick confirmation that Ally does not like being used solely/primarily as a transfer hub. If you repeatedly move money in, just to move it out again immediately, they will close your account. I can see their side that such behavior appears like potential for fraud, even if it it isn’t. It would be nice if they outlined their policy more clearly. I’ve moved some big amounts through Ally when I really needed to, but it was maybe once every 6 months and I still use them for day-to-day activities.

Also want to add that in my experience the bank doesn’t care about the positives of your relationship, if the right person sees any potential concern, you are history. I had been a good Ally customer for many years, I had my work direct deposits there, and I regularly had 20K plus in my accounts. BofA chopped me off after about 15 years with them, and again I had my direct deposits there. They are judge, jury and executioner, and they’ll hit you with a 30 days notice letter out of nowhere (that always takes at least a week to arrive in the mail).

I was using them for some pretty decent MS, due to their system of allowing many checking accounts all under one user account. I was moving in over 5 figures per month and was never questioned about it. I made sure that I moved the money in and then paid from Ally. No middle-man operation due to the time the transfers were taking. Apparently that may have been my saving grace.

Another nice thing about Ally Bank is that they have no fee for incoming wire transfers. That’s a great saving if you’re someone who receives wire transfers on any kind of regular basis.

I have had the occasional difficulty with check deposits, where their software doesn’t recognize or accept a check I’m trying to deposit, but overall my experience with them has been great!

If people are using this for long-term saving, they might as well use Ally’s CD:

http://www.ally.com/bank/high-yield-cd/

It’s higher yield and their early termination penalties are pretty ok. I guess for people that expect to just leave a security deposit around for a while but still want the flexibility to get the money back in case of an “emergency”

Been using Ally for a while now. Once they added the mobile deposit option via mobile app it made using it even more convenient. The app can be finicky, but I don’t deposit enough to complain about it too much….

The purple is a psychology thing that implies wealth, according to (http://www.vandelaydesign.com/the-psychology-of-color-in-web-design/).

“Purple has long been associated with nobility, so it is no surprise that dark shades of purple imply wealth and luxury. Lighter shades suggest fields of lavender and are associated with spring and romance.”

I do love Ally bank. I just wish they had plans to support Apple Pay. I may leave them soon for that reason.

Agreed. I make sure to call at least once a month and inquire about it.

Agree – and Touch ID – I told them I would close all my accounts if they do not have that feature by the end of the year. For an online bank, they are now super late on new mobile features.

Love Ally. I’ve had the their MM and online checking for quite awhile now. Interest on the MM is .85 and I don’t use it’s debit or check features….hmmm.

ALSO: It’s a bit buried in your article, but Ally checking reimburses you for ALL US ATM fees, no exceptions. (not sure on foreign ATMs tho).

Yes you’re right they won’t reimburse foreign ATM fees. However, in my experience in Europe and parts of Asia the ATMs often don’t charge fees on their end. Instead, usually your own bank gets charged a fee behind the scenes and passes it along to you via a $5 foreign ATM fee or similar. Ally Bank doesn’t charge such a fee on their end, so in those cases you’re still getting money without fees.

Any idea why banks don’t let you do online transfers on weekends? It seems stupid to have computers work only during business hours M-F.

My understanding is that it has to do with the antiquated ACH (automated clearing house) protocol has almost every bank uses. If you’re up for a longer read, check out this article about a bank trying to speed things up.

http://dealbook.nytimes.com/2014/12/13/small-bank-in-kansas-is-a-financial-testing-ground/?_r=0

Since you touched on the UI of the website, you may want to mention that substantial changes are coming soon: Their Beta site is at http://www.ally.com/learn/earlyaccess/

Thanks, I don’t recall them telling me about this, but I may have overlooked it. The new UI looks a lot like their smartphone app. I like the bigger text elements and the overall feel, just hope all the fancy stuff doesn’t slow everything down.

I use Ally for several CDs, but have only used ING Direct / CapitalOne 360 for online savings. Happy enough with their interface, especially for multiple accounts, and with the small difference in rates I’m not ready to move yet.

One thing that’s always confused me about my CDs at Ally, though: why does the interest accrued only get added to the balance every 3 or 6 months? I’m pretty sure that when I had CDs at ING Direct the interest was added on monthly.

Hmm, funny timing. I noticed sometime in the last week Ally raised their savings interest rate to 0.95% APY, but as of today 12/19/14 the rate has been upped again slightly to 0.99% APY. Wonder why.

If may be in direct response to SallieMae bank and others upping their rates to 1%.

so glad the interface is changing. I actually stopped using them because I had to click 2 times just to get account balance. Long live ING Direct……

How are the rates compared to DCU( Digital Federal Credit Union) Bank ?

The number of allowed external accounts is 20 not unlimited.

Thanks Gaurav, I was recalling outdated information. I have updated the review. It used to be unlimited but they changed it to 20 max a while back.

Have used Ally as my main bank for years. Do prefer it to ING Direct etc. However, one peeve I have is Ally doesn’t provide outgoing international wire transfers (only domestic allowed). If any Ally staff see this, do please consider offering that service. After all, this is the era of globalization!

I’d add that it’s also inconvenient to receive incoming international wire payments at my Ally account, as Ally doesn’t have a SWIFT code for receiving international payments. As a result all incoming payments are routed through an intermediary (JPMorgan Chase), and I lose $25 on every incoming payment (even if the amount is less than $100!). Ally: If you can’t offer outgoing international wires any time soon, please at least make your existing SWIFT code available to receive incoming wires so that your customers can be spared this horrible $25 fee for receiving international wire payments.

I have trouble with checks being rejected. It is certain types of checks it seems that the app just doesn’t like.

But the password is the big announce. I have an iPhone 6 with the fingerprint scanner. My CapitalOne app just needs a 6 digit pin to deposit a check. But for Ally I have to go to my computer and find my password (it would actually increase your risk to have a memorable password, so this encourages poor security).

Does Ally Bank allow for Sub-Accounts / partitioning of funds / etc? For instance, I have 10k but want to reserve $5k as emergency, $3k for new car fund and $2k general savings.

CapitalOne 360 / ING Direct allows for this and it is a real ‘sticky’ feature – as in, I won’t leave because of this single item. I love the ability to be saving toward particular goals and not have my savings all jumbled together. In my case, I have about 10 sub account to cover emergency fund, future big purchases, kid college savings and travel funds. It’s great.

I’m also wondering this^

Yes, but perhaps not exactly in the same way as ING Direct.

1) You can open multiple online savings accounts as each has no minimum balance and no fees. You can even open up a bunch CDs as they also have no minimum deposit requirement.

2) You can edit the “nickname” of each account so that each one has a unique name like “college fund” or “travel”.

I’m not 100% sure on this, but I believe that ING Direct sub-accounts don’t actually open a “new” savings account for you, but Ally does. Just a small difference. Hope that helps!

Can I recommend the Barclays Online Savings “Dream Account”? You can deposit up to $1000/month. If you have continued deposits for 6 months, you get a bonus on your interest. If you have no withdrawals for 6 months, you get a bonus. You can have up to 3 (IIRC) of these specialty accounts – currently paying 1.05%. I dumped CapitalOne this year due to their conitnued low rates.

In this age of low rates, I think .30% is reason enough to move, along with the small bonuses you get for being a good saver (since you are capped at $1000/month deposits you almost have to have continued deposits for 6 months so at least you’ll get that bonus)

I was slowly transferring the money from CapOne360 to Barclays, but if you schedule a transfer on a weekend or holiday, the transfer (on Barclays end) gets rejected – you can either pick a middle of the month date OR move your money over to a savings account and “drip” it into the Dream account. So far, no rejected transfers. 🙂

They also offer regular savings accounts of course and CDs. Not sure of the limits on number of accounts, but I would guess it would be reasonable enough for most people’s needs.

Just an FYI.

I have been a customer for long. However, I don’t like the fact that they only allow you to see 18 months worth of transaction (either via statements or transaction search). They should allow up to 7 years. I recommended this feature to them but they kind of ignored it. It would be nice to see 18 months of monthly statements + 6 years of year end summary type statement that most credit cards offer.

FROM FIVE STARS DOWN TO ONE. The best thing about this bank is going away in August 2015. They offered free ATM usage throughout the US. If you used an ATM at any bank, grocery, gas station, c-store, etc., your fee would be reimbursed to you at month-end. They also had some network where you could use certain local banks’ ATMs at no charge, without having to worry about fee reimbursement. There are 2 such banks within 5 minutes of me where I have always used their ATM for free. Well, no more of that!

They emailed notices today saying that starting 8/15/15, ATM fee reimbursement will be limited to $10 per statement cycle. So if I go somewhere that charges $3.50, after my 2nd ATM withdrawal in one month, I’ll be paying my own ATM fees. Now, that might make sense for a brick-and-mortar bank, but for an online-only bank which HAS NO ATMs, that’s garbage. Their new 43,000-location AllPoint network is also garbage. If I wanted to park my car and go inside a CVS or specific grocery store (neither of which I ever, ever shop at) in order to use an ATM for free, then maybe I’d stick with Ally. Otherwise, I’m outta here.

Also: really, really super-frustrating, slow, and dumb customer service. The people who answer the phone don’t know anything. I don’t mean that sarcastically. Ask them anything, and they have to put you on hold for a long time to find out the answer to your question. Who are they asking!? Why don’t they know simple things? Then if you need more details, guess what? You’ll be put on hold again while they “check some information” or “find that out for you.” It takes forever to get simple information out of them. All my calls to Ally have lasted five times as long as I thought they should have needed.

I’ve been using an Ally money market account as a savings account for years and the only thing I will say I had trouble with was confirmation of receiving a wire request form and actually getting the wire issued. I faxed the form in, however their customer service agents aren’t in the same location as their wire department and as such have no way to confirm if yours was received. I talked to multiple agents over multiple days with some telling me they’d call me back after confirming it was received, had others tell me it was received when it wasn’t and that the wire would be issued the next day (which obviously wasn’t either). It was a lot of roundabout action before they would give me an e-mail address to send it too as a last ditch effort to beat a deadline for a refi and to not extend closing.

Otherwise, I use it all the time as a higher interest rate savings account and it seems to work great.

I know you can have multiple savings accounts at Ally, but can you have multiple checking accounts?

Yes, i have multiple.

As of Oct 2015 Ally’s live chat has been unavailable whenever I tried in the last couple of days. I wonder what’s going on. I always prefer chat to phoning.

I’ve been hesitant to use Ally because I don’t know how difficult it would be to close the account. Do you have any information on this? Does it take awhile to get your money out? Do they transfer to a new account or do you have to wait for a hard check of some sort? Thank you!

@Carolyn:

I don’t know whether it’s easy or hard to close an account with Ally since I have never closed my accounts. I have bank with them for 5 years. No issues. Since the rates are very competitive, it doesn’t require a minimum and direct deposit, there isn’t a reason to close them.

I, myself am ready to move a big chunk of Ally Savings to Everbank and open a Yield Pledge Checking Account. Must be a first time account. They offer 1.6% for 6 months. $1,500 to open. I already have their 1.6% Yield Pledge Savings Account. Better than any 6 months CD right?

I was wanting to open a savings account with ally. I am a student right now and just want to open an account to save money in. Starting off with about 150 or so. I was going to leave the money alone and add as I can. But I was wondering in maybe 5 years or so if I would be able to pull all my money out and about how much the fees would be more or less. Any advice will help. Thank you.

Jonathan, thank you for this. I’m an old ING Direct user finally considering the switch from Capital One 360 to Ally, now that Cap One has rejiggered their user interface in ways I don’t like. I’m hoping I can find this info out from someone on this thread without going through the signup process and trying it out myself:

(1) Does Ally allow a “memo” line for all transactions like Capital One 360 does (and ING Direct before that)?

(2) If so, when viewing list of transactions in an account, how many clicks required to see the aforementioned memo?

(3) How does Ally display scheduled (pending) transactions? On the same screen as past transactions?

(4) Does Ally require a credit check? (I have all bureaus currently frozen, would have to pay $5 each to temporarily unfreeze)

Dan — Late reply, but I’m doing a transfer into an Ally savings account right now and here’s what I see…

(1) The transfer form has a “Note to Self” line, with the hint text saying “Viewable in Activity for up to 120 days.”

(2) I don’t see the note to self that I wrote for a previous transfer anywhere when viewing the Transaction History for the account. (I know I wrote the note b/c I saved the confirmation page to a local PDF file.) The Activity page they promised the note would be visible on is part of the Transfers section of the site, not account info.

(3) Under Bank Account Transfers > Activity, there is a section for Scheduled, followed by a section for History.

(4) Dunno, don’t recall.

Also, the note to self does NOT appear in the transfer request email that Ally sends you after you submit the form. Don’t they realize that some people would like to record and see *why* they made transfers?