Each December, I run the numbers to see how much more I can contribute to my Self-Employed 401k plan, aka Solo 401k or Individual 401k. Fidelity, Vanguard, and Dinkytown (used below) have calculators to figure out contribution limits to various types of retirement plans (Solo 401k, SIMPLE IRA, SEP IRA, Profit Sharing Plan).

Each December, I run the numbers to see how much more I can contribute to my Self-Employed 401k plan, aka Solo 401k or Individual 401k. Fidelity, Vanguard, and Dinkytown (used below) have calculators to figure out contribution limits to various types of retirement plans (Solo 401k, SIMPLE IRA, SEP IRA, Profit Sharing Plan).

In general, as long as your income isn’t too high ($275,000+) and you aren’t deferring salary from another workplace retirement plan, the Solo 401k will allow you to defer the largest percentage of your business income. This is because the Solo 401k allows you defer as much as $18,500 (2018) in salary as an employee as well as 20% of your net self-employment income as an employer (both sides of your business) up to $55,000 total (2018). For example, if your income from your side business was $5,000 and you had no other salary deferral elsewhere, you could put 100% of that into a Solo 401k. (If you are age 50 or over, you can also add a $6,000 catch-up contribution to the salary deferral limit.)

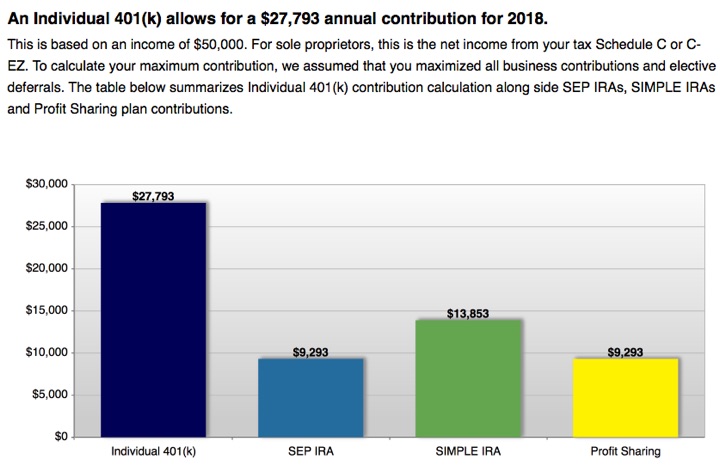

Here are sample numbers for a $50,000 net income to your self-employed business. This assumes you are a sole proprietorship or an LLC taxed as a sole proprietorship. The math for a single-owner corporation is slightly different.

At $50,000 net business income, you can defer 56% annually ($27,793). This is exactly $18,500 more than if you went with the SEP-IRA.

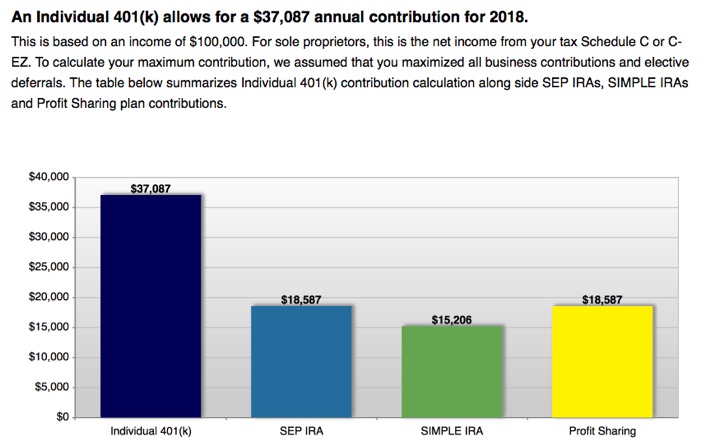

Here’s the comparison for a $100,000 net income to your sole proprietorship.

At $100,000 net business income, you can defer 37% annually ($37,087). Again, this is exactly $18,500 more than if you went with the SEP-IRA.

Now, the Solo 401k does require a bit more paperwork. For example, you will need to file the IRS Form 5500-EZ separately every year once your Solo 401k assets exceed $250,000 to avoid steep IRS late penalties. SEP-IRAs have no such annual requirement. Therefore, if you don’t intend to take advantage of the higher contribution limits of a Solo 401k, I would consider sticking with the SEP-IRA. But if your goal is a high savings rate and maximum tax-deferred funds, look into the Solo 401k. I would compare the offerings from Vanguard, Fidelity, and Schwab. (Mine is at Fidelity.)

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I’ve had a solo 401(k) for about 5 or 6 years now, and I love it for all of the reasons that you covered.

Yes, and the amazing thing is that you can do the employee part ($18,500) as ROTH IRA.

Jonathan,

Good timing! I was just thinking about this yesterday.

Maybe you know or have seen it discussed somewhere. How will the retirement plans such as Solo work with the new Sec 199A 20% deduction? Can they be stacked?

If putting money into Solo or similar plan reduces the income that is subject to the pass-through deduction, it is no longer such an amazing proposition. With Solo you are saving money at your marginal rate – say around 30% including Fed and State – so the real saving would be only 10%. While it is still not bad, personally I’m happy to lose the flexibility of using this cash at 30% savings but not at 10%.

The article states: “This is because the Solo 401k allows you defer as much as $18,500 (2018) in salary as an employee.”

Does this mean if I work at a company that does not offer a 401k plan and I am a W-2 paid employee of that company that I can open up my own Solo 401k plan and contribute up to $18,500 of my salary a year? I did not think this was the case but that is how I’m reading the statement. If so, that would be great. Would I just transfer monies on my own to the Solo 401k account I set up? Any special reporting or forms I would need to fill out come tax time?

Thank you

No, it has to be self-employment (business) income where you are the employer and employee. You should read the statement as “This is because the Solo 401k allows you defer as much as $18,500 (2018) in salary (from a self-employed business) as an employee (of that business).”

I’ve been funding my SoloK this way for years, and it *is* great. It turns out that it’s even better if you have an S corp instead of an LLC. With an S corp, you can sock away up to 25% of your salary (instead of 20%), up to $36.5K for 2018. For me, being over 50, I can put away $24.5K + $36.5K = $61K for 2018.

You do need to pay payroll tax on that income, but you end up coming out at least a little bit ahead, given that you avoid self-employment tax, especially if you pay some of your after-tax compensation as dividends. You do need to pay yourself a reasonable salary, and it ends up being driven largely by how much you want to contribute to your SoloK…

What if I’m employed full-time with an employer-sponsored 401K plan. And I also have my side-business via LLC. Can I still take advantage of Solo 401K?

@bill: even with an employee – sponsored 401K, you can still participate in a SoloK. The catch is that you still have the 18.5 K limit, and you need the income in your business to meet the 20% number

I had no idea you could do this – WOW! I really need to look seriously into this. It could help me save tens of thousands! Thanks!

Is it true that you need to have a ADMINISTRATOR for your Solo401. I have mine opened at Vanguard, and have to pay a 3rd party to administer the fund. They’re actually NOT doing anything for me at all (I do my own investment and everything else……). But they are charging me quarterly for being a administrator of the account.

Yes, you do need an administrator (to provide a Plan document). I believe Vanguard charges $20 per year, per fund, which seems relatively reasonable as you can trade them without commission. Fidelity does not charge any fees or commission on their NTF mutual funds, but there are commissions for ETFs and stock trades.

My understanding the business owner can be the plan administrator.

I should rephrase. You need someone to supply you with updated, and legally compliant Plan Documents. Technically, I am the plan administrator for my Solo 401k from Fidelity. Fidelity supplies the Plan document and updates it regularly as needed to comply with all the legal requirements, as they are complex with big penalties for errors. They send it to me, and I sign it. Supposedly there will be some updates in 2020.

You can also get the plan documents from a lawyer that specializes in Solo 401ks and then go invest your money in apartment complexes or something unique, but you usually need to keep paying annual fees for them to keep the plan document updated. It’s probably possible to DIY if you are a lawyer, but honestly I don’t think the risk is worth it unless this is your specialty. I don’t have any reason to look further as Fidelity gives me a Solo 401k with no annual fees and I can buy virtually any stock, ETF, mutual fund, or bond that I would want.

Solo 401k EIN – Many financial advisors and tax accountants are giving several different set up advice. Some state the Solo 401k should have your business EIN, some say your SS# and some say a separate EIN # . Do you know what is the difference in reason/usage for the EIN set up using a Business EIN oppose to a Separate EIN?

Solo 401k Contributions – There’s Employer contributions and Employee contributions. Do you know if it matters which one funds first? Also, does the 941 change though the contributions are tax deductible?

Is it also tax deductible for the employee?

I appreciate any guidance

Still somewhat confused on this topic. I am fortunate to have a 401K through my partnership at which I receive a K1. I am able to fully fund this to the max including the full employee and EmployER portion up to ~$58K (or whatever it is now).

I also have side gig EIN sole proprietorship. Lets say the side gig nets 30K/year. How much of that can I put away into EmployER portion of Solo401K? And can I do more with a “mega back door roth”?

Thanks