One of the perpetual debates in retirement planning circles is withdrawal rates, AKA how much monthly income can you take from a portfolio. Once you nail down a withdrawal rate and retirement spending target, then you get Your Number – how much you need to have saved to retire (after backing out Social Security and other income streams). It’s common to start with the static 4% rule, but that rule also includes some drawbacks. An alternative is a flexible withdrawal rule that adjusts based on market returns. When your portfolio grows, you can spend a little more. If it shrinks, you cut back a little. Sounds reasonable, right?

One of the perpetual debates in retirement planning circles is withdrawal rates, AKA how much monthly income can you take from a portfolio. Once you nail down a withdrawal rate and retirement spending target, then you get Your Number – how much you need to have saved to retire (after backing out Social Security and other income streams). It’s common to start with the static 4% rule, but that rule also includes some drawbacks. An alternative is a flexible withdrawal rule that adjusts based on market returns. When your portfolio grows, you can spend a little more. If it shrinks, you cut back a little. Sounds reasonable, right?

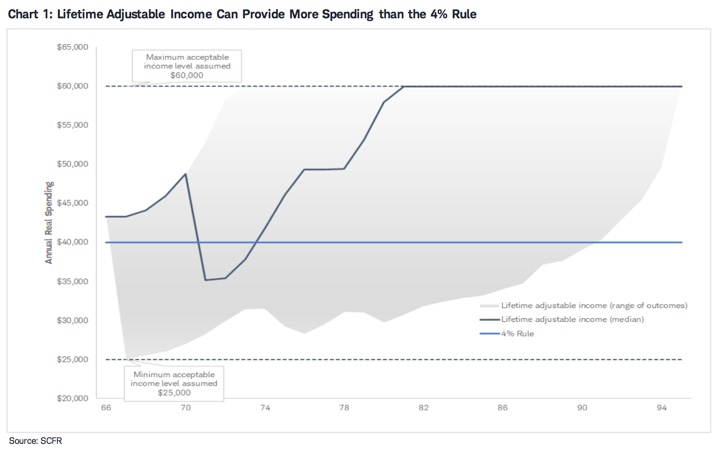

However, I haven’t seen many real-world examples of flexible withdrawal rules. Schwab has helpfully outlined one proposed method in this memo: Lifetime Adjustable Income vs. the 4% Rule: Can You Spend More in Retirement with Less Risk? This provides the underlying basis behind their robo-advisor feature called Intelligent Income where you can pick a comfort level and the software will tell you how much you can withdraw each year and from which type of account (IRA, Roth IRA, taxable, etc).

In this memo, we compare a flexible withdrawal strategy to the static 4% rule. We recommend a lifetime adjustable income strategy, described in this paper, that can be put into action using an annually updated financial plan, using technology or an advisor. Doing so may help increase spending early in, and over a long, retirement and help ensure your money lasts.

Here’s their example structure for flexible withdrawals:

- Set an initial withdrawal rate that delivers an 80% probability of success (savings lasting).

- Adjust spending amounts after each year based on if the probability of savings lasting falls outside the range you decide: here it is below 75% or above 99%. If these thresholds are crossed, increase or decrease spending by the amount that brings the financial plan back to a 99% probability of savings lasting. This results in fewer but more drastic cuts.

- Add “guardrails”. A minimum and maximum acceptable annual (real) spending amount of $25,000 and $60,000, respectively, meaning that we will always withdraw at least $25,000 (or at most $60,000).

Using these flexible rules, the initial withdrawal rate was about $43,000 instead of $40,000. Across all of the simulated scenarios, the average annual withdrawal was basically 20%, or $10,000 a year, higher: $50,000 a year instead of the $40,000 a year (in today’s dollars). Even better, the likelihood of running out of money dropped.

However, you must look past the averages and see that you are now exposed to the extremes. Look at that wide expanse of grey. A significant number of the scenarios involved some extended deep cuts to spending, hitting and hovering just above the $25,000 minimum guardrail. You’ll have to decided if you like this trade-off between probably getting more income but possibly enduring some big cuts. This is why many financially-conservative people would prefer to simply start out at a lower 3% or 3.5% withdrawal rate and adjust upwards if the portfolio keeps growing.

In any case, I found it interesting that Schwab used the probability of portfolio survival rate as the factor used to adjust withdrawal rate. DIY investors can implement a similar system themselves. Here are some tools to estimate portfolio survival probability:

- Vanguard has a very simple one.

- cFIREsim and FIREcalc allow you to enter a variety of variables manually.

- Personal Capital remembers and tracks my actual portfolio and updates this number automatically. That part is free but also offers an optional paid financial advice tier.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

But why spend down capital at all? It seems having a passive income stream from existing assets is the way to go.

It all depends on if the assets you own already distribute income. If you owned Berkshire Hathaway stock, it generates huge amount of cashflow internally, but the money is allocated to buy more businesses. There is no dividend, but it is definitely growing in value. There is nothing wrong with selling a bit of BRK stock to pay the bills.

For the most part though, I do agree that a mix of broad low-cost US and International stock index funds can be treated as a “dividend growth fund”. In Europe, you have more companies saying stuff like “we will distribute half of our profits as a dividend, so it goes up and down”. In the US, you have more “we will try to create a sustainable dividend that goes up slowly but only drops in severe cases)”.

The problem is that your withdrawal rate would be in the 2% range, though. That’s why people spend down capital. “How much have you saved over your lifetime? Just save twice as much!” is not a popular answer 🙂

I guess in the end you can’t eat capital appreciation. I like checks. That gives me the freedom to reinvest as I see fit. I’m targeting a 5% dividend yield. That might not be realistic; You’ve studied this extensively and have a better idea of what makes sense. I’d rather not worry about valuations in my lifetime and let the dividends be sufficient.

I see Vanguard has a 2.65% SEC yield from High Dividend Yield Index Admiral Shares. So it looks like the 2% range for a high quality index fund is about what you get. I play the ponies, so I’m managing about a 4.95% yield so far from high quality select blue chip stocks. But that isn’t for everyone (looks like I got whacked in the recent volatility, but this is a buying opportunity for quality companies, with a long time horizon), and for my retirement funds, I’m using Vanguard funds, VTI in fact, and an international fund (also Vanguard I think) split 50/50. For this, I don’t care about yield, just owning the whole haystack.

But for the brokerage, I think the dividend value approach has merit, and historically undervalued blue chips, relative to historical dividend high and low yields, is the way to go. In the end, what really matters is a disciplined approach, understanding your expenses and income, and planning for the worst.

The insights you share here are always worthy of consideration.