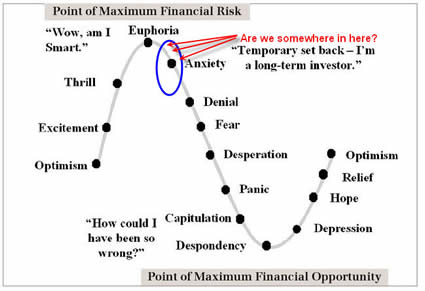

I’d say I’m somewhere between anxiety and denial now. If you can’t tell, I’m thinking of buying a house in a large West Coast city sometime late in 2007. Hurry up despondency! 🙂

This chart would be funnier if it didn’t hit so close to home. “Temporary set back, I’m a long-term investor”. That’s me! Image via Mish’s Economic Analysis.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Geesh I’ve gotta hand it to you Jonathan you are the charts and pictures master! For the A.D.D generation your blog by far beats the blan cluttered P.O.Ses out there and liturally sets a new standard for the P.F. Bloggers to try and follow and/or keep up to.

Keep up the awesome work and oh by the way if you ever get a chance could you set up a “page vs post” (instead of doing a post since it won’t be finance related) for all that you’ve learned about wordpress. Since you have by far one of the best designed blogs I’ve seen out of the hundreds. Also how did you make your comments colored, I’m just now trying to hope into the world of CSS and horribly simple PHP so any help would be appriciated.

The last mania in housing prices in CA peaked in early 1991 and bottomed in mid 1995. The price of my house went from a purchase price of $250,000 in late 88 to $300,000 in 1991 when I went through an appraisal to get rid of PMI as I had only put 10% down when purchasing. The price of my house bottomed in 1995 at around $200,000. So four years from peak to trough. I think we have a way to go if the past is any guide.

Since you expect real estate prices to go down so much, does that mean that my Real Estate Fund that is part of my 401k should expect much lower returns as well? Just wondering if I should lower my contributions to Real Estate and/or transfer from my real estate fund to something else. Love the post though so thanks man.

There’s no reason to listen to me about housing prices, I’m just antsy because I want to own a house. 😉 People have been talking about an RE bubble for years now, what’s to stop it for continuing for another year? The Fed might keep rates the same, we could be having the same exact discussion in January 2008. The only thing that I’m pretty certain about is that the party can’t go on forever.

Also, REITs aren’t always correlated with residential housing prices. Much of their revenue is from collecting rent on commercial properties.

Outside this macro economics discussion, there’s a micro level discussion as well. As many investment books stated, you can make money even in flat or down market. The same with real estate. Yes, when things are going down hill (party is over), everything is hard to move. On the other hand, people got to live somewhere and trust me, most people who moved into their own house do not ever want to rent again. So the demand for housing will never die out. Owning a house is a classic American Dream, owning Goggle stock is not.

In addition, there are many housing related factors that don’t seems to be related to simple economic trends. For instance, natrual environments, travel distance to work, school ratings. All these tend to stay the same and remain factors to housing price. All these unique geographic variables will translate into the risk and fluctuation of housing prices.

For example, an earlier commenter said his/her house in CA swing from 250k in late 80s to 300k in early 90s, then drop down to 200k in mid 90s. I suspect a similar house in a premium neighborhood will have much smaller variation during the same period.

I found this fascinating as house buying for most people is a one-time deal and you can’t really diversify (unless you are really an investor who’s trying to buy 6 houses at once.)

You have to treat it as an investment, otherwise, it makes no sense why single or childless couples would ever want to buy houses in a good school district.

Jonathan,

If you’re looking to buy your first home in California you should hit up your local real estate agent that has had at least 20 years experience. In fact, find at least 2 or 3 agents with that much experience. I say 20 years because that would allow them to have experienced the full real estate cycle (relatively speaking).

Take Manhattan for example. Manhattan will always be a market of its own and rarely is it affected by what’s going on nationally. If you come across anyone who’s comparing real estate prices in L.A. to San Francisco, that’s like comparing apples and oranges. It’s the same as comparing Manhattan to Brooklyn. Don’t forget the 3 L’s, location, location, location. (Manhattan is an anthill, an Island a true destination point for the world, but I still love Brooklyn)

You can’t treat real estate like the stock market, as if you’re waiting to buy a stock at a significant discount. If you’re buying real estate for investment, then you should pay attention to how much you pay per square feet. However, if you’re buying to live in for the next 10 years it should not matter what the price is, as long as you can afford it comfortably, because you never know where the local real estate market will be in 10 years.

Even if you hear on CNBC that the real estate market has bottomed out, you have to ask yourself if it pertains to your home city. If you hear that the Dallas Real Estate market is crashing does that mean major cities like Manhattan or San Francisco will crash too?

I know Manhattan’s real estate market intimately and I always compare it to the global real estate market. If you choose London or Tokyo, Manhattan is just catching up in price per square feet.

My advice to anyone who is buying to live in long-term, 7 to 10 years, don’t worry about where the real estate market is right now. Buy it, enjoy it, and realize that you’re not dumping money into the landlords pockets through rent.

Also, anyone who thinks they can predict real estate markets more than 3 years out is fairly ambitious, unless you’re widely known as a guru.

best of luck folks,

PJ

I have just started my financial journey (got a Job 4 months back) I have to do loads of financial planning before I can reach the optimism stage. You can say I am in a gestation period.

I greatly appreciate your housing posts since I would also like to purchase property in the near future (probably not until 2008). I am also looking to buy in an expensive city. I feel pressure to hurry up and get in the market before the neighborhood I want to move into gentrifies and I can’t afford it–it’s one of the last affordable areas left in the city. I hope your chart is right–that would mean prices will be on the lower or more reasonable side right around when I’ve scraped together enough for a down payment!

Buying as soon as one can afford it, within the traditional parameters is a given.

The sticky point is that we really can’t tell if it ever will be affordable, and how does one relate to a goal which is not proven to be feasible? In other words, although one should save for a short term goal like a down down payment in safe vehicles such as short term bonds, CDs and money market funds, what if in 5 years you still can’t afford it? A potentially huge opportunity cost.

Morgan – I would not reduce my REIT holdings. 1) They aren’t directly correlated to real estate prices. 2) If your assets properly are properly allocated and the REIT’s do go down, that means you’ll be buying more shares. Market timing and asset allocation usually do not mix.

I think I need Tolak to elaborate more on what he/she is saying. I’m not too sure I understand his/her point of view and I’m interested in knowing.

A couple of questions: Why would anyone set up goals that are “not proven to be feasible”? I think the point of financial planning is to set up a strategy so that they are feasible. This website is offering strategies.

The point of saving money is to have enough for a down payment. If buyers can do 20% down and make it through the first 3 to 4 years of mortgage payments you should be fine thereafter. You would probably refinance if rates are lower after 3 or 4 years. If not, then you should be fine regardless.

What if in 5 years you can afford a home because the housing market is down? If you’re assumption is that the R.E. market will continue to climb in 5 years then I agree it would be harder to afford, but as I said earlier it’s tough to accurately predict real estate more than 2 or 3 years out. I think owning a home is always possible because the housing market moves in two directions, up and down. The point is to be prepared to buy a home when you can manage it.

It’s only my opinion and I’m interested to hear more about Tolak’s point, but overall the comment sounds like there’s no hope, where I know there is hope.

Remember that a primary residence is first and foremost a place to live, not an investment. You will have some level of emotional attachment to your home and that does not mix well with “investment”.

tolak references housing price increases outpacing your cash/cash flow increase. This is always an ongoing risk but you should be able to make some decent judgements here. Are you a social worker of 10 years and unlikely to make a career change? Odds are your history of 10 years will predict your future income and cash. If it your rate of income increases doesn’t exceed 2-3%/year, you are probably always going to be behind the curve and should probably lower your price point. Are you fresh out of law school and still working a non-legal part time job? You can probably safely assume over the next 5-10 years your rate of pay is going to significantly outpace home prices/inflation and might want to wait and save.

But a key point here, particularly for those wanting to buy in expensive markets is: do you NEED to live there, or WANT to? Even living somewhere else cheaper as an interim step to a) save more faster and b) let markets/incomes stabilize is worth considering.

My take on the current state of the RE market and I am in now way an expert. The numbers in most markets indicate that Supply is increasing and Demand is decreasing and foreclosure rates are up. Why? I believe that the market became over saturated with these Card Board Box, cookie cutter homes that builders were popping up at record paces and were letting people into with 100% financing (hence increase in foreclosures). Now that interest rates have climbed a bit naturally demand is going to decrease. Now, what do I think this means for RE Funds, RE Investing and buying a primary residence. As mentioned before, RE Funds cover many aspects of the RE market. So, when less people buy more people must rent. I have not seen a down turn in my RE Fund, in fact it is still providing me an incredible rate of return. As for RE Investing, I believe the time is coming for buy and holds. Property is going to get cheaper and the supply of foreclosures is increasing. I believe it’s beginning to be a good time to hold because more people will need to rent and vacancy rates will go down. I do believe flipping will still be profitable, but the margins may decrease since it will be harder to sell. As for a primary residence, I would look for something a bit unique, something with above average quality that separates itself from rest of the market. Anyways, just thought I would share my take on the situation.

when I bought my first house in 1999 I felt pressure to get in because real estate prices were the same as they had been 10 years prior. It was pretty obvious that something was going to happen soon. I had to basically pry my fiance’s wallet open to make it happen (I had money too but he needed to be in agreement about the whole thing of course).

Right now, as you are showing in your diagrams, there is no real pressure from any upcoming event. You also don’t have a child to send to school. I say that the longer you wait over the next 2.5 years, the happier you will be with your decision. You can stick all the extra money you might spend on taxes, repairs and everything else into some kind of good interest bearing account and you will be much better off right now. I know, over the long term it doesn’t matter, that’s true. But over the short term, you will show a profit if you wait. And hey, you’re the guy who made me apply for 2 credit cards just to get $150 and an i-pod — so you must see the logic in waiting too.

I do not agree with the real estate chart below. What I know is that we are in a new real estate market like never before and that we will never revert back to a time where one’s mortgage payment will be significantly less than what they are renting their property for (with 20% or less equity).

As rents keep going higher and higher this will have an impact on property values. While now housing prices are on the decline the higher rent values will stop this trend soon enough.

In terms of where we are now in the scale I do not agree with, it would be between fear and depression. Many in LA are past the anxiety and denial stages. That was over 6 months ago.

One should also keep in mind that there is a belief long-term interest rates may go down in 2007.

I always look at buying a house and treat it like buying a rental property. I try not to be emotional about any buying decision (and thank God that I have zero pressure from my wife)

If you can pay cash, what is your potential return / net income from that investment (ie potential rental income – expenses).

I’m currently renting a brand new condo for $1900/mo ($23k/yr). The owner purchased it for $650k. After property tax, HOA, maintenance, insurance, property mgmt fees (total $12k/yr), my landlord only nets about $11k / year, a measly 1.7% yield pretax.

His only hope of additional gain is thru capital gain. But who will be the greater fool of buying a piece of property with such a low rental yield?

Assuming he has the cash, he would earn $32.5k pretax in a 5% CDs.

Price will revert back to the mean.

Check out MISH’s Japan’s real estate chart: link

Eman wrote: “What I know is that we are in a new real estate market like never before…”

Transation, circa 1999: “What I know is that we are in a new economy like never before…”

Hilarious! You are kidding, right? There are many parts of the country where you can *still* buy houses for less than renting, or at least for a comparable price. Just because CA, FL, NV, AZ, and Washington DC are in bubble zone doesn’t make it the “norm.”

I completely agree with Brian. I know this sounds trite, but “norm” or “normal” is a relative term.

I don’t completely agree with NapoV, but then again I’m completely ingorant of California’s R.E. Market. NavpoV is right about showing a weak return if his landlord bought the condo at the middle to top of the R.E. Market. However, if his landlord bought towards the bottom of the market, then the upside could be fair and the measily 1.7% return per year (also known as cap-rate) won’t matter as much. The real return is when he can selling it and make 25% or more.

FYI: You ideally want a cap-rate of about 6% to 8% or more, but usually it’s around 4%-5%. Most investors I know who buy multi-unit rental buildings use cap-rate as one form of evaluating investment property.

Although NapoV’s landlord is earning approximately 1.7% return on his condo, I have a few friends who can only afford small studios and the hope to cover costs (mortgage+maintenance). In other words, they aren’t being greedy and only need the property to pay for itself. At the end of the day you’re wealthier for it because when you sell, you’re pocketing your initial downpayment and whatever you paid off in mortgage (or more like whatever your renter paid for you) and you’ll have a larger cash account to put down on your next purchase. Maybe you’ll purchase a multi-unit building. At that point, cap-rate is the name of the game.

1.7% is weak and 4% is ok. If you want high percentage returns, then NapoV is correct to suggest stocks or interest bearing savings accounts, but nothing beats owning property and when you get good at it, you’ll start finding 6%+ cap-rate investments. Try living in your own multi-unit building and knowing all your tenents are paying your rent. That’s the best feeling.

Best,

PJ

To all house hunters, I’m going to recommend something that drives Realtors insane:

Don’t make an offer on anything until you’ve seen at least 50 properties. This sounds insane but it is absolutely practical.

Want to learn how the housing market is in your city? Visit 50 – 100 properties and trust me, you will! You will learn EXACTLY how much something is worth.

Can you hold out that long? Also, house hunt all spring/summer/fall, then make your offer around Thanksgiving. Anything that’s still for sale during the holidays HAS to be sold.

the commenter above “clicclic” has a good point about sales during the holidays. right around thanksgiving there was a condo for sale near a big tourist attraction and it’s still for sale only “price reduced” sign is now up.

i went to a real estate investing seminar a few months ago (it was free and offered by a mortgage company that also takes people on tours of properties or weekend trips). and they said the pacific northwest is very iffy for real estate investment. the job growth is stagnant and the economy isn’t growing … but then just plain ole joe people tell me if you’re holding out long term it doesn’t matter what history says.

i’m still waiting for the bay area housing market to burst (it’d solve a lot of my parents’ marital woes). even houses comparable in size in suburbia are going for the same price as it is in SF. i dont know who’s interested in buying a million dollar plus home in suburbia when they can live in the City.

I just wrote a members only blog on Active Rain about how the seller must go through the 5 stages of Death before becoming realistic about a price. I like this graph too!