I understand that revealing our net worth is not enough to fully explain our entire financial picture. That is by design; I like keeping the picture fuzzy. Blogs are very hard to keep anonymous, and I’ve been doing this since 2004. This is why I continue not to share our respective salaries, occupations, employers, and geographical location. Besides, I am not here to be better than you, or the next dude. Anyone out there could earn more than me, save more than me, or spend less than me. I’m only trying to track our progress, and to consistently try to make our situation a little bit better each day.

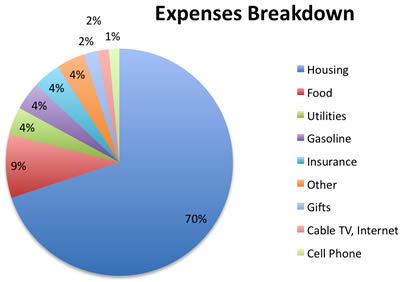

But I’ll give in a little bit. I think tracking expenditures is a good idea for everyone, so I might as well share what I have discovered. Besides, I’ve already revealed that our goal for an Emergency Fund is 6 months of expenses, or $30,000. That means my wife and I spend $5,000 a month? How? Here’s the lovely pie chart:

Housing: We spend $3,500 a month housing, 70% of our total monthly expenses. (Note that this is not the same as 70% of income!) This includes principal, interest, taxes, and insurance (PITI). Yes, it is obscenely high. The median price of a home in our area is over $500,000, so don’t go thinking we live in a multi-acre 5,000 square foot estate. At the same time, incomes here are also a lot higher, especially in certain fields. So there is a give and take.

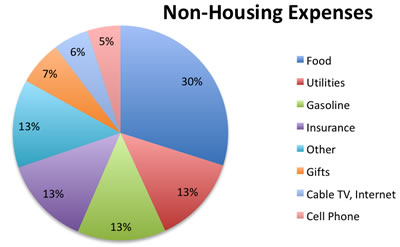

Given that this one area skews the graph so much, I made another graph of all non-housing expenses:

Food: $450/month includes both groceries and dining out. This is where the “fat” is in our spending, and we know it. We love food and do our best to “consciously spend” and enjoy every dollar put into this pleasure. I’m okay with making many simple foods at home, but I still go out when I want to eat freshly baked naan, perfectly seasoned pad thai, authentic pizza, or hand-wrapped tamales.

Insurance: $200/month includes two cars and umbrella liability insurance policies. Our deductibles are $1,000 to keep costs low, but our liability limits are high ($250,000/$500,000) due to the requirements of the umbrella policy.

Utilities: $200/month includes electric, gas, sewer, and water. Gasoline: $200/month. Cable TV + Internet: $80/month. Cell Phones: $75/month for two lines.

Gifts: $100/month. This might be somewhat unique to us, but given our big family events like birthdays, weddings, graduations, usually end up costing us $100 per month.

Other: $200/month usually covers the other smaller categories including clothing, entertainment, and pet expenses.

That ends up with the total being $5,005 per month. $3,500 to housing, $1,505 to everything else. Health insurance is provided by our employers. Non-monthly expenses like home improvement projects, travel, charity, car purchases/depreciation, or medical procedures are not included.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

$450/month is pretty good for groceries and dining out. That’s only $7.50/person-day. I’m guessing that you bring your lunch to work and eat a lot of meals at home (you might as well since you’re paying so much for it). We’re in a similar situation as far as monthly expenses, and our goal is to keep it under $500/month for food. Some friends of ours spend over $1000/month just on restaurants.

$450/month is actually amazing! How do you do it? We usually spend almost twice that per month on my wife, my son and I.

I am a longtime reader and seldom comment. You really don’t have to give into the pressure of people trying to get you to reveal your income and savings rate. I know that nobody forced you to produce this particular post, so thanks for sharing. I honestly feel you have given enough by providing your money saving tips, deals, and other financial information.

So, everyone ought to be thankful that you take the time to work hard at this blog and I am sure many do. However, if people don’t like it that you don’t spill all of your beans, they are more than welcome to visit the thousands of other financial blogs that are out there. I am constantly amazed how people are never fully satisfied, as if they could do better or better yet, take the time to gather the information themselves and distribute it for the benefit of us all. Oh well…my 2 cents. Thanks for all you do.

Ha, after reading the frugal couponers who feed their 6 person families for $200 a month, I feel like $450 is huge for two people…. 😉

Most meals are at home for sure, but I still go for lots of cheap eats joints. Heck, my favorite Indian spot rests on two wheels and two concrete blocks…

Josh – Thanks for the kind words. I’ve been sitting on this post for a while, waiting for Mac access so I could make the pretty graphs. You probably know that I’ve posted about my budgeting and expenses already in the past, so this is still pretty consistent with that. I don’t think I’ll ever share exact salary breakdowns.

Jonathan-

I assume that the things you mentioned as not included in your monthly expenses such as charity, car purchase/repair, medical procedures, etc. are accounted for somewhere else in your budget? I’ve been trying to figure out how to account for these less-frequent expenses in my budget without driving myself crazy and was wondering if you had any tips on that.

And since we’re on the topic of being nosy, when do you expect to do another portfolio update? Just curious… 🙂

Anyway, thank you for sharing all that you do…I know reading your blog has greatly improved my financial situation!

Just wondering where home repair bills fit into this. I just spent $200 to fix a plumbing leak and $1000 to do some tuckpointing and put a concrete cap on a chimney. Right there is $100/mo. just for home repair. Maybe you have a newish home and don’t need to repair much yet. I guess these expenditures would go under “Other”, or would you consider that to be “Housing”?

Yes, like Michael, I also spend more like double your food budget every month. That is really good — considering you love food too. I’m sure the place with two wheels has good food, but I actually love Indian cuisine in my favorite restaurant with the far eastern harp music playing. It’s not really expensive, but there’s no way I could buy regular food and eat out for less than $200/wk. Regular shopping is about $125, and eating out for the rest.

I was going to say, $450 isn’t very astounding; we feed a family of 4 for about that in a HCOLA. We eat quite well. We just don’t eat out very much. (I do admit before kids we spent much before because we mostly ate out. So, good for a 2-full-time working household. I’ll give you that. 😉 )

Interesting – thanks for sharing.

You mean you don’t make all your money from this blog? 😉

When I was single, I was been able to pass on a budget of $100/month for food. But it’s rough. However, married, it’s actually cheaper when you share food costs, so 100/month/person is actually decent eating.

Johathan,

Thanks for sharing this information with your reader. I guess after you pay off your house, you will be able to live only on $1550 in 2008 dollars. That’s amazing.

How big is your house? Can you afford to rent out a bedroom to someone else in order to increase your alternative income?

Thanks for sharing, I am ignorgant to the taboo people place on discussing income.

I have an estimate by totaling the monthly expenses and monthly savings. Assuming you and your wife pull in roughly the same salary, I would simplying the equation.

Total individual salary = [(savings+expenses)*12]/2

Living the DINK (dual income, no kids) lifestyle has been very good to you.

I’m envious and need to convince the old lady to combine our money and start the notion of my/her money is OUR money.

By the way Jonathan, I posted it on the make a goal page here on your blog, but I wanted to let you know, your advice has helped me.

I recently bought a house with lots of equity. All the discussion about net worth, investing and thinking through good financial decisions has really helped. I suddenly have a very positive net worth (it was quite negative before).

The substantial equity puts me in a great position in all other kinds of financial situations. I also have a credit rating of 725-750 (depending upon which company). I am not even sure how that happened, but it has something to do with managing my finances 😉

If nothing else, this blog at least forces me to think about my finances every day, and that helps me make better decisions with my money.

Interesting insight–thanks for providing it! Although our situations are no where near similar I consider you/this a benchmark for my own progress. Thanks again.

Unrelated: what did you use to generate the graphs? Is that Numbers?

Holy Poop! 450/month on Groceries and Dining? My wife, myself and toddler, spend 900/month.

My wife stays home. I brown bag everyday for lunch.

How about a blog post on your grocery/dining?

I don’t think what you put out there really explains much. I do this for myself too every month and I include things like house repair, as mentioned above, along with vacations, car repair bills and whatever else I can think of to see REALLY what I WILL be spending. I know you don’t have to do this and I am surely not criticizing you but your public budget is just a subset of your everything budget and I think people would like to see exactly how you do plan for other expenditures.

Also on food, I cannot believe that you only spend $450 a month. With a wife and two kids I am happy to be under $1200 a month. Eating Indian food from a cart on the street, while it may be super tasty :), is not the healthiest way to eat. You may be saving money now but you may pay for it later.

This is a help to reverse engineer income, but I don’t understand how income is personally identifiable. Or why it is such a taboo topic. That is unless one wraps his/her self worth up with the money they earn.

I make $49,500/yr. That’s up from $47,000 last year. I was happy with my raise.

Do you know who I am now?

Interesting to see other people’s food bills. For the previous 12 months we’ve averaged $350 for our family of 5. This includes eating out perhaps an average 2-3 times per month. But we have a garden and raise some of our own meat.

I budgeted $250 for groceries and another $100 for dining out. I eat out on average 2 times a week (mostly on the weekends), cook quite a bit and brown bag my own lunch. However, I mostly buy organic/natural food, so that might be a reason that my numbers are not lower.

klein, I have no idea who you are. But you also didn’t write this blog for years that has little bits here and there of personal information. The income or where he works could just be the ticket to figuring it out, and this his superhero cover is busted. Busted!

One thing I’ve always wondered though, Jonathan… do you keep this secret from your wife? and is your name really Jonathan?

I agree with the statement about income being irrelevant when the poster is anonymous, especially when the number is very average. Since no one else has, I’ll take a guess then: $110k.

It would seem with that income that the house you purchased is incredibly expensive. My income is in the same general area and I consider my comfortable zone for buying a house to be $400k and would sacrifice a little to get $350k. Am I insane? I’m surprised a lender would even give you a loan for 38% of income!

See, he gives a little and people want more.

Food is always the amusing argument on the Internet. Someone posts their food budget and the people go wild.

I spend $1000 a month! I spend $100 a month! What’s wrong with you!

FYI – The utilities figures don’t add up ($200/mo + $80 + $75 is already more than $200/mo).

Thanks for this post! Pretty figures! It’s always interesting to see how someone else’s expenses stack up against your own.

Uri – Actually your math is wrong. His net income is roughly $5k in expenses plus $6-8k in montly savings (estimated from net worth updates), so a total of $11-13k. That likley excludes his bonus and other non-montly income. Work backwards to get the gross income and you end up with ~$200-250k in gross annual income depending on his state tax.

I am in a similar income bracket but have higher expenses in comparison. Main differences are food (more than triple J.’s expense), but I also have cleaning lady, travel. dry cleaning / ironing of shirts & pharmacy expenses that drive my total expense to ~$2k above Js (if I would assume equal housing costs). We could definitely cut food costs by 30-40% or so, but getting to <$500/month would be brutal. So kudos to Jonathan & wife for keeping their costs down inspite of high income.

Yes, I too am figuring around $110,000 combined. Maybe a little more with the things he said he left out. This allows me not ‘to judge’ him, but to put myself up against him and see that, in fact, if I were making the same on my own, or had a spouse that contributed the difference, I/we would probably be doing similarly well on the saving front alone. That’s all I was really interested in knowing.

As for “he gives a little and people want more” of course, I would want more, and I see no problem. I genuinely appreciate what “Jonathan” does. But the instant that you start writing (and keep writing) a blog that gains popularity, whether you wanted it to or not, put adsense on it and continue the high volume of posts (which allow comments) that keeps readers coming back often (Excellent, high quality posts, I might add) you are beholden to at least hearing their feedback.

He doesn’t have to do anything he doesn’t want to do. I am glad for this post, but if he wanted to continue to ignore my requests, or even to delete my comments, that would be up to him and I would consider this blog just as good.

Just as you have the right to condemn my comments, I have the right to ask for something from a blog to which I subscribe. I also make it a point to click on the Adsense links often, by the way.

Actually his family probably clearing around 200k or more a year. You have to factor in taxes and his investments. His take home pay is roughly 10-11k (spends about 5k and saves almost 5k).

FYI I wish I could keep my food costs to 450. Groceries alone cost me almost 800 bucks a month. (My wife loves organic…. ie whole foods and wegmans)

For those guessing around $110k combined, I think that is pretty low, unless you are saying $110k after taxes, which I think would be pretty close but my guess is closer to $120-$130k after taxes, which would be somewhere around $200k before taxes and other deductions.

This is very helpful for comparison, Thanks! For those (including yourself) that think you may spend too high a percentage of your income on your home, don’t forget that rules of thumb are for folks who don’t budget as well as you do (and banks that can’t know your spending habits). As long as there is no cash flow issue (you are still saving adequately for retirement & emergencies), and there is enjoyment gained from the more expensive house, higher spending on a home is great! I’d guess from the numbers you spend only a quarter of your after tax income on things that lose value (that $1505/month), the rest goes to savings/investments (which will grow in value) & your home (which will give you shelter/enjoyment and maintain its value).

You all also have to take into account taxes. So if you figure $110K takehome, it’s probably more like $220K gross.

I too wonder about the taboo against sharing one’s salary. I am more than willing to share my salary ($46K), and not because I’m arrogant; I actually make below market salary for my field. I just support the public and free exchange of information.

We are spending like 10-15% on housing in the Midwest 😉

Me too. My combined is roughly 230k per year in the DC area. Though I dont nearly save as much as jon

I’d like to echo Dee’s comment here: Just wondering where home repair bills fit into this.

I similarly don’t see anything for a car. I see Gas and Insurance, but what about tires and brakes and oil changes and all of the other things that happen. Unless you plan on abandoning your cars when they die, you’ll be paying for your cars (and your house) for the rest of your life.

Will you be happy having to make a down-payment on your next car from your savings? When the water-heater breaks, is that coming from the savings too?

It seems odd that you’re building an “Emergency” fund, but you don’t have any money allocated for “Eventualities”. (and maybe you do have such a fund, at which point it would definitely be an educational number for many readers).

Since people are sharing, I’ll share my expenses. 3 little kids, single earner ~ $70k.

This is based on take home salary (after taxes and payroll deductions like 401k). These are my averages. It is different every month.

House 28%

Food, gifts, clothing, entertainment, etc 23% (my wife gets paid twice weekly by my salary to do the household budget as she determines)

Insurance 9% (have private health insurance)

Gasoline 8% (probably more now)

Save 7%

Give 7%

Utilities 5%

Phone/TV 5%

Preschool 3%

YMCA 2%

If something like a house repair or other expense comes up usually some of the savings and the giving are the first to go, sad to say. Those should be first, shouldn’t they?

well if you guys STOP subscribing to this blog and STOP clicking on his ads, I am sure his income would decrease 🙂

$226,000 combined gross income.

Less $31,000 401k contribution.

= $195,000 TAXABLE INCOME

Less Taxes = $54,475

http://www.irs.gov/formspubs/article/0,,id=164272,00.html

= Net Income of $140,525

I looked at monthly expenses of $5,005/month.

And I also took into consideration your liquid assets & liabilities (cash and credit cards).

Your net liquidity grows on average by $6,739/month (using a running average of 2008).

Change in cash – Change in credit cards.

So (5,005 + 6,739) * 12 = TAKE HOME PAY

AM I CLOSE?

I find the reactions to your food budget interesting with the majority of the comments exclaiming that $450 for 2 is quite low. I frequent a budget board, and someone spending that much would get absolutely crucified as a spendthrift! This is pretty telling… your readers have average higher income than the ones on budget boards. :p

I think it’s helpful and motivating to know what salary base you’re working with when you’re talking finances and savings. I’m so used to anoymous personal finance boards that I feel absolutely no taboo talking about salary. In fact it’s a requirement on the boards I hang out at!

I swear though that Jonathan mentioned he and his wife both moved to the Seattle Washington area and they both made 6 figure incomes after changing jobs. Boggle… did anyone else catch that?

I forgot to include state income tax (9% seems accurate using California & Oregon as a baseline) and OASDI (6.2%) & medicare (1.45%).

So take $226,000 / (1-.09-.062-.0145) = $271,145

So, somewhere between $226k and $271k gross income…before investment income….?

I vote C) Barry Bonds. I happen to know he gets take away Indian all the time.

By the way, Barry, which graphics program to you use? The pie charts are pretty slick.

For a family of three, I spend $200 a month on groceries and food, but we do not dine out much, and that’s about 25% of our total income at this point because we have one income. Then again, I was spending that when it was only 10% of our monthly income. This was a great post, and I am glad to have found it!

How about dropping some coin on vacation/recreation, dude? Hawaii? Cancun? Trips to Europe? Life’s too short!

Also, not really that interested in how much money he makes, but my guess is that as he gets older and his income increases, he will spend more on groceries/eating out. When I was younger and first bought a house, it was a much larger % of my income than today. I was also much younger. And at least for many people I know, when you’re in your 20’s, eating Big Macs is fine. And as you grow older, your tastes change and you’re more concerned about proper nutrition, and thus seem to spend more. Also, you might prefer to go to Mortons on an occasional Saturday night as opposed to Olive Garden. (Not that there’s anything wrong with Olive Garden.)

Jonathan: you’re doing pretty well at $450/mo. My wife and I are a little younger than you and we have a 2 year old. For the last year, our grocery bill was $4500 and eating out bill was $4550, so it averages out to about $750/mo. We eat out for dinner once a week and eat out for lunch maybe 1.5x per week on average (this includes the weekends — we rarely eat out on weekdays and we brown bag our lunch). I don’t see how people can feed families on $200/mo unless they are eating junk like beans, rice, and home made kimchi. I even use coupons and about 75% of the stuff I put in my grocery cart is on sale.

To share a little more, my household earns around $125k gross (entry-level engineer and accountant 3 yrs out of college) and we take home $81k, of which $10k goes to our Roth IRAs. We spend the other $71k, including $2000/mo on our mortgage. Note: we already have our emegency fund in place, so we don’t save anymore besides the $10k to the Roth and a maxed out 401k.

I make less per month than Jonathan spends on housing/month! My wife and I have a mortgage and spend <$200 on food/month and that includes eating out. It’s not too difficult to do in the midwest, in my opinion.

midwest, I cant speak for. I live in LA area, and and someone who works full time and has a spouse who works full time, I can definately say I really look forward to my Saturday night dinners out! I definatley hate working all day Mon -Fri and having to think about what’s for dinner, go to the store to get it and cook it and clean up afterwards! I am not buying a large carton of Kraft mac-N-Cheese at Costco to eat all week. My husband and I will end up overweight and with heart problems from too much fat if I do!

To some of the posts on house repair and / or car repairs / replacement:

I am a long time reader of this blog and love it.

I maintain my budget and track my savings in Excel. I used to have separate accounts for different things with ING Direct, but then I switched to other, higher paying accounts and had to club everything in one saving account.

In Excel, I track my monthly balance like this:

E****** Bank account:

Emergency fund Capital Fund Impulse fund Total

Activity: +200 +350 -1000 -450

Balance 33749 21933 317 55999

I have no debt other than my mortgage, a four year old car with 43k miles on it that cost me $17k cash down. I keep adding to the capital fund more right now because I am rebuilding it after a very necessary bathroom remodel / repair). Just bought an HDTV (that’s where the impulse fund comes in – a TV, or a Playstation, or a bike, and maybe a kayak in the future). I plan to use cash for my next car, and hope to be able to build the capital fund so that I can be prepared for any major home repairs that may come up. Interest I earn on the account gets allocated to the three balances directly; I do not factor that into my “activity” for the month – that is just deposits and withdrawals.

Other than this, any savings I can manage after maxing out my 401k go to paying down my mortgage. I took a 30-year mortgage for the lower payment (which gives me flexibility), but hope to have it paid off in about 15-16 years.

Home improvement projects, and travel are also not included. These things are highly variable from month to month and also year to year, so it can be tough to budget well. I usually just pay for them as needed out of monthly cashflow or savings.

Travel – Thinking about Thailand-Cambodia-Vietnam in early 2009 to avoid monsoon season. Been distracted by house projects this year.

Uh-oh. Catwoman is raising the Bat signal, says I need to help fold the laundry…

I appreciated the tip on making gifts a budget item so you can save for it throughout the year. It seems I’m either scratching around for cash whenever we need to give a gift or dipping into the emergency fund. Not the best way to go about it. Monthly saving for expected gift needs is a great fix.

Somebody made a good point above…expenditures and income will change as you age. I am expecting to see semi-annual trips to some Napa Valley day-spa followed by a dinner at Greystone on your budget in a few years 🙂 (not French Laundry though! That will wait for a while methinks 🙂 )

Jonathan,

I am suprised you have an umbrella policy – not for the blog i assume? whats the rational? I got one due to my rental properties, but not sure I would keep it if I didn’t have the rentals.

Jon, I really appreciate you sharing the details of expenses. I am a long time reader of your blog. I think people wanting to know your salary wanted a broader perspective of how you balance your budget and you have responded spot on. I hope next time you fill pressured you think deescalation. I know why you have this blog. Seriously, the point of the blog is not solely net worth tracking like some of the other blogs but to include ideas/philosophies/tools/musings to help readers reflect upon theirs. I hope the readers get this. Number and percentages comparisons are easy but to reflect on your situation and needs is harder.

i too am a long time reader and seldom comment. i would like to echo everything josh said in his first post. this blog is VERY helpful and informative. but i will say that i don’t think that people are asking necessarily to be nosy-i think they are just genuinely curious and want to see how they are doing in relation to someone who is clearly lightyears ahead of the average person in fiscal responsibility and knowledge. i know this helped me, and i need to do the same thing for my household and see where i need to trim the fat. thanks again for the post and for your blog in general.

John,

Does your 3500/mo housing expense include prop taxes and home insurance? Or, is your home insurance in the 4$ slice of the insurance pie?

Hi Jonathan,

Love your blog – been reading it for years; it’s been such an inspiration to my fiance and I. What program do you use to make your pie charts?

Jonathan,

Which carrier did you choose for two-line family-plan mobile phones of just $75/month?

My experiece with AT&T/Cingular is current $86/month and with T-Mobile was $90+/month last year — T-Mobile was evil to frequently charge additional $40-50 per month.

Besides, which company is your Cable +TV $80/month? Do you have a home phone?

Andy

@Andy: Jonathan likely gets a corporate discount if he works for a large company. My wife does, and we pay $67/mo for a family plan w/Verizon. We also got 2 free phones which normally have a “$129.99 2-yr contract price.”

@Andy: If you read Jon’s older post you will notice he has Sprint’s SERO plans which are $30/month and includes tons of minutes and unlimited data + additional cost for txt msgs, I believe. So its two such lines + taxes.

I did an analysis of estimate net income based on net worth month last year o so. At that time, Jonathan and wife was brining home ~$5500; but, now that they both work full-time, and Jonathan still has his side-projects and makes money here on this blog, the net income is ~$12,100. Matadam and matt are probably close. But, if we’re on “the price is right”, you cant go over. Either way, I still find it amazing how we spend alot on housing. I live in a metro area; rentals and condos/houses are expensive. While old-school says you should spend no more than 30-35% on housing expenses, I think the new thought is now anywhere from 40-60%. Old-school said housing usually includes utilities. That’s sad but true. Real estate now is pricey; incomes havent caught up. We are all spending more for gas, transportation, groceries, food, services,. 3 years ago we were spending less for these items;.

Many have already commented on your food budget. To me the amount also seems reasonable, and with rising grocery costs, keeping it at $450 per month would be a good achievement. Also there will now be increasing pressures on mortgage rates and utility bills. Rather than look to cut your monthly expenditure, it might be more realistic to maintain it at current levels.

Daniel: It looks like Jonathan uses Excel for Mac for this pie charts.

Hey Jonathan – I’d be interested in a discussion on Umbrella personal liability insurance as that’s something I’m thinking of right now

Good idea. I do all of this on excel, but I need to do graphs to get my wife on board.

Nice! I enjoyed your net worth updates and expense breakdown. This is a lot of detail actually and as much as I’d love to do the same thing, I am *truly* unable to give this kind of financial data out. More and more people I know personally have found my blog out and are reading it and well, it’s too dicey to let people you know find out about your finances… 😉

But great job on the expense management! I struggle to keep a lid on our expenses. I also found your net worth growth quite impressive! It won’t be long before you hit a million! 🙂

I’m amazed that you only spend $200/mo on utilities. My electric bill alone last month was more than $200 and I think my house is comparable in size to yours. Then again I live in TX. I would say I spend $300+ on utilities at a minimum. A little less in the winter.

@amadeuz: keep in mind you are probably running your AC everyday in the summer. i’m in boston and i’ve never spent more than $50/mo in the summer for electricity (in a 1600 s.f. house), but i expect to spend around $800-1000/mo this winter to heat my house w/oil (we have a toddler and will keep the thermostat pretty snuggly).

Hi! Thanks so much for this blog. It gave me more insight to what I might expect in the future. I’ll be moving to Kansas City by the end of this year and had no idea how much to budget for what!

(Please don’t shoot! We’ll be peace-loving immigrants who will do our part for the community and we promise to recycle and not mess up your beautiful country!)

According to everything I’ve read (besides for the fact that the residents don’t like immigrants), my husband will get a rather good salary, however, I can’t seem to make everything fit into the budget. Am I over-spending on certain things? Does anyone know if Kansas City is expensive? What I’m especially not sure of, is the utilities. 3 bedroom house, sewer, electricity, water…. is $200 too much, too little? Please help?

Yana: Does anyone know if Kansas City is expensive?

Depends where you’re coming from 🙂

I just moved to Kansas City from Western Canada and the prices are very reasonable. $200 is about right for sewer, electricity & water, but you’ll have to factor for heavy monthly differences. This summer we had 10+ days of 40 Celsius (100+ Fahrenheit) where it’s basically a sauna outside. Obviously we spent a lot of money on Air Conditioning that month.

If you’re a renter, you can easily get the 3-bedroom in the $1100 to $1300 / month range. But do account for location. Kansas city covers a very big area, so you’ll want to pay attention to your work location when picking a place to live.

If you have kids and you’re not planning on private school, you’ll likely want to live on the Kansas side of the line. Kansas City is half in Kansas and half in Missouri. The Kansas side (Johnson County) is one of the top school districts in the country.

Oh yeah, and be prepared to own a car (and maybe a second one) if don’t already. The public transportation in KC is pretty anemic and the city is built “out” not “up”.

I don’t want to clutter up Jonathan’s blog any more. Feel free to post on my (less trafficked) blog if you have to some specific questions.

I’ve always found that this type of analysis is fascinating! I think a lot of people would be surprised where their money ends up going. Especially on the small things – such as everyday lunch at your canteen, or a pint here and a pint there!

It all adds up and just means people on a budget have to do just that – budget!

I have tried a few tools to do this out there, but none quite capture the simple “in and out within 5 mins” routine.

I just signed up to your blog and I want to say thanks

I am learning and enjoying the information.

Im finding the responses for more information around Jonathan’s salary comical LOL. This is exactly why I don’t share any of the sort on my own blog, especially as Digerati noted with more friends/family reading. I don’t exactly want to share that information with them unless asked personally face to face.

BUT I must confess that I did come here looking for salary information as I remembered that Jonathan and his wife are DINKS. I did want to compare salary and expenses as my husband and I toy with the idea of buying a larger home taking advantage of the recession deals in our area.

Im always impressed with Jonathan’s savings rate as Ive been following this blog from it’s inception. Just trying to figure out with the purchase of a new home which is double the price of our current and $1500 more (mortgage note), how his expenses stack up against ours.

Hi – very nice site! I like the analysis – especially so that I can compare what we’re doing to others.

Our monthly grocery bill varies, but on average is around $500 for a family of three. Eating out just adds to this, by around $300 per month – this is the one thing that we’ve found tough to keep down.

How does everyone else manage?

Mo

there are 115 million households in the U.S. $200/mo for utilities times 115 million households equals $23 billion per month we spend on utilities. that’s $276 billion a year, $1.3 trillion every 5 years, & $2.8 trillion every decade. “What’s on second. I’m not askin’ ya who’s on second! Who’s on first. I don’t know! Third base!”