Housing prices. Are they still falling? Stable? Best time to buy ever?

Barry Ritholtz of The Big Picture thinks that housing prices have much further to fall. Here’s part of his analysis:

Today, residential real estate confronts numerous headwinds: Credit, once given to anyone who could fog a mirror, is now tight. Hence, demand is far below what it was during the past decade. Home prices are still unwinding from artificially high levels, and remained over-priced. Inventory is elevated. Unemployment remains high. A huge supply of shadow inventory is out there: Speculators and flippers who overpaid but have held onto their properties await modestly higher prices to sell. Bank owned real estate (REOs) continues to increase. We are barely halfway through a decade long foreclosure surge.

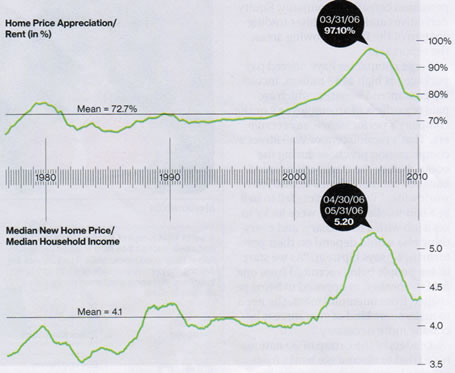

He also shares some historical data from 1977 to 2010 that support his view. The top graph below is home price appreciation divided by rent as measured by CPI. If the ratio is rising, it means that home price appreciation is rising faster than rent. If the ratio is falling, it means that rent is rising faster than home price appreciation. Then there is the price/income ratio, illustrated by the bottom graph below. In both cases, we are currently still above the historical mean.

From 1977 to 2010, the median US home price was 4.1 times median household income. But as the chart below shows, Home prices are still above that mean. Oh, and that mean is artificially elevated due to the 2002-07 boom. Same with home prices relative to rentals, or housing value as percentage of GDP. Further, we should not assume that prices will merely mean revert back to historic levels. In most markets, a near 3 standard deviation price move is resolved not by reverting to the mean, but by by careening far below it.

Data source: Ned Davis Research

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Glad to hear he’s still repeating what Patrick.net and others have been saying for years and years:

http://patrick.net/housing/crash.html

http://www.housingbubblebust.com/

Both of these websites look a little quackish, but have been dead right.

And not long after, Ben Jones started this blog:

http://thehousingbubbleblog.com/index.html

@John – Perhaps, but I don’t feel like those sites are unbiased. I get the feeling that if housing does turn around, they will be the last to admit it.

I haven’t been traveling a lot these days, but I know things in my area of the DC aren’t staying on the market long, if they are decent homes. Most homes in my neighborhood are selling within 1-2 weeks. I bought my home a little over a year ago and prices have not changed much. Prices have come down, but mostly in the condo market. Single family homes I don’t see sitting long, besides real high end homes or neglected homes.

Agreed. The bubble sites seem like they have something to profit from a housing crash.

Thanks for sharing the analysis. It does seem like prices should come down some more.

Prices are being supported by ultra-low interest rates. When those rise, house prices will move lower.

I wonder if the current chart numbers are skewed due to large unemployment and pay cuts. i.e. if the economic recovery happens – housing may be priced right (for normal employment conditions). i.e. Salaries may need to move up as opposed to housing dropping further to restore historical averages.

I think if they did a similar chart to #2 but compared the multiple of median income level to mortgage payment, housing would look fairly priced or better. As said above, low rates are supporting the market. In the eighties mortgage rates were sky high and even if rates normalize they probably won’t go that high again and stay there, so today your monthly payment supports a much higher home price than in the 80s, something a complete analysis of home valuations needs to consider.

As a real estate investor and buyer of sheriff sale homes and foreclosures for many years now ,I have to say that while prices for homes in my area being sold ‘person to person’ have had a nosebleed, the prices that homes are being offered at the sales by the banks is ridiculously higher than normal.

I realize this is due to the poor lending practices they have led and now they are upside down on these homes (which what they have created would have happened whether there had been a downturn in the market or not).

The homes simply are not worth what they are trying to recover and may never be again in the future. We are finding that some of these loans are well over 100% LTV more likely creeping into the 110-120%. The lenders in this area caused this problem, as all over the country as well.

What will happen in the future is anyone’s guess as the books on the banks part now is pretty darn ugly but I think they are just seeing the start of the real mess to come. We are going to have so many homes flooding the market in the years to come that I think the values are going to stay pretty darn low for a long time into the future.

Let’s hope that I am mistaken…

House prices have been supported by government programs like the first-time home buyer credit. This has kept prices above long-term trend which tells me that the decline is far from over. A boom usually ends in a bust and not in an orderly decline. Let the market clean itself rather than give us the illusion that the bust can be controlled. Why control the bust when officials let the boom run rampant? If anything, try to control the boom. Then you won’t have to work ten times as hard to control the bust.

The risk in housing is still to the downside in the US because people are still too leveraged. What would happen if interest rates spike to say 8-10 percent?

It all depends. There are so many sites that thrive on the schadenfreude of ‘home debtors’. They want nothing more than for housing to go to $0 for whatever reason.

In the end, it is a lifestyle decision, not an investment. If you wait forever, you will have wasted some years. For me it is simple math. If you find a house, go to the courthouse and find how much the house sold for about 30-50 years ago. Go to the government inflation website that calculates the increase of any number based on inflation. Do some analysis on the area to see if the economy has been stable/growing/ghost town over the long term. Does it all check out? Then you are not buying an inflated house. You might be off a few thousand, but does it really matter over the course of 15-40 years?