This post provides updated information and instructions regarding the free FICO score that is available to American Express credit card holders.

This post provides updated information and instructions regarding the free FICO score that is available to American Express credit card holders.

Background. In late 2014, American Express started piloting free FICO scores to select cardholders. In late August 2015, American Express has rolled out the free FICO scores much more widely. See additional information below. In previous years, AmEx cardholders could view their Experian PLUS credit score and credit report once every 12 months.

FICO Score details.

- FICO Score version: FICO Score 8, or FICO 08. This is the most widely used of the many FICO flavors. Score version is directly shown on the website.

- Credit bureau: Experian

- Update frequency: Monthly

- Limitations: Available to all American Express consumer credit and charge cards. See details below.

How to find the score. You can find the score after logging into your online account access. In order to see it, you must be viewing the American Express website in its “new” design layout (see screenshots below). If you are still on the “old” layout, try to unlink any cards for which you are the authorized user. In many cases, this will let you revert to the new design layout. Here are some screenshots.

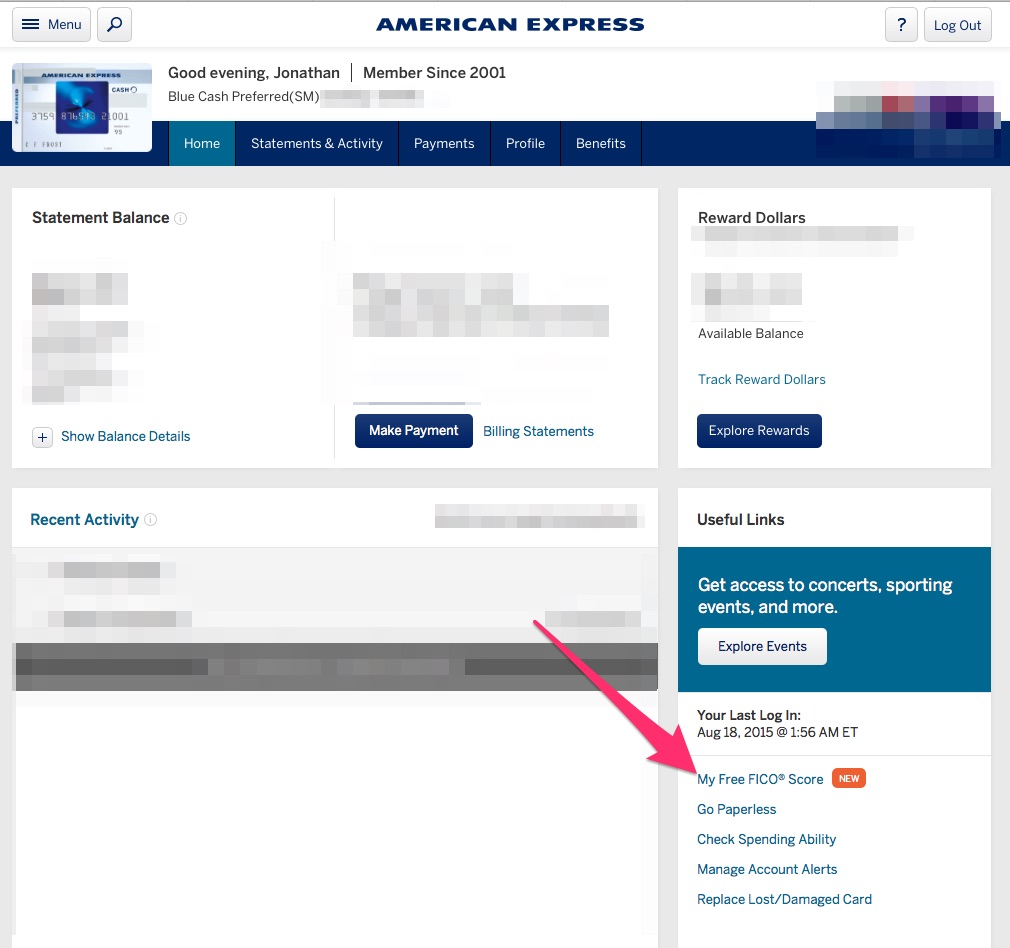

Look for the “My Free FICO Score” link on your sidebar (click to enlarge):

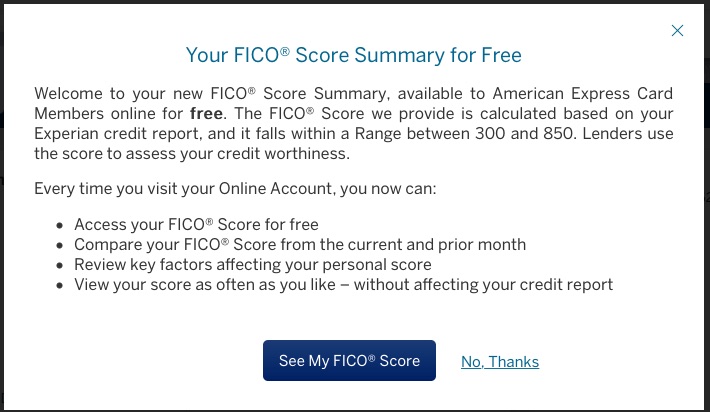

You will have to opt-in:

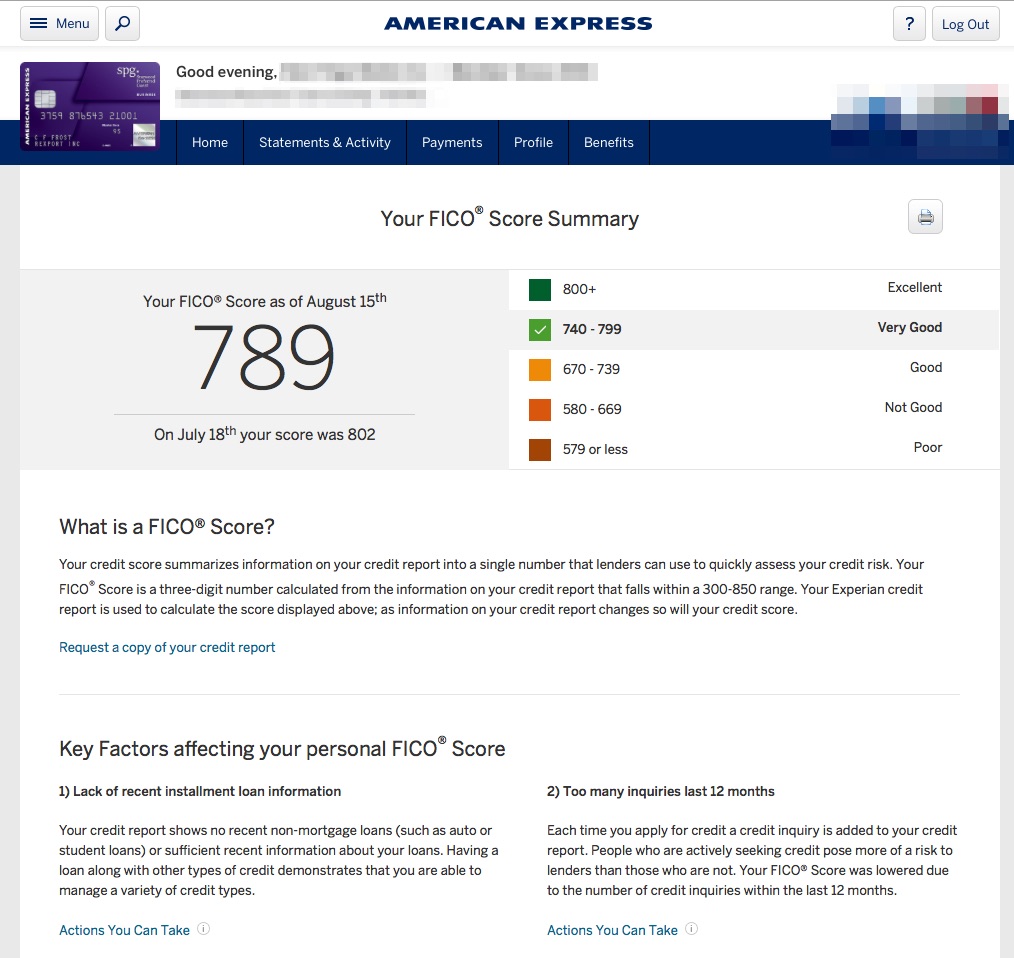

Here’s what your score report looks like (click to enlarge):

Fine print:

The FICO® Score we provide is the FICO® Score 8 based on data from Experian and may be different from other credit scores. FICO® Scores and educational content are delivered only to Primary card members who get a monthly statement and have an available score. This information is intended only for the Primary card members own review purposes. American Express and other lenders may use different inputs like a FICO® Score, other credit scores and more information in credit decisions. Because it is continuously updated, your FICO® Score may not reflect the most current data on your credit report. This benefit may change or end in the future.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

The following quote from FICO is what is troubling to me & confusing to those of us who understood 850 as the top score and what distinguished FICO from the FAKO scores (especially the FAKO scores that went as high as 950)..,

“The versions range from 250-900 (compared to 300-850 for base FICO® Scores) and higher scores continue to equate to lower risk”

The fact that FICO scores can now go above 850 is what makes me think, “now even FICO has FAKO scores”!!

Hi Jonathan, I always appreciate the new information that you find and share. About the FICO score, though, I though I’d point out what I learned this month buying a condo — it doesn’t mean much to the mortgage companies. At least three of them (Quicken Loans, Capitol One and Assurance Mortgage) told me that it is considered a “soft” score. A “hard” credit pull is a separate process and goes through a unique algorithm. Funny how my 800+ FICO score didn’t equate to an 800+ from the banks — more like 697.

This was a great heads-up. I have been wondering for years. The only way to get it previously, for free, was to get turned down for a loan, at least that is what I have been lead to believe. This new service by AMEX is a really good idea. Thanks for your wonderful blog and I love your picture with your baby.

There is a significant discrepancy (~50 points) between my AMEX credit score (Experian) and the Capital One credit score (Transunion). Which score is the one used by financial institutions for loans and what not?

Thanks.

I don’t think the Capital One score is a FICO, while this AmEx one is a FICO 08, and also your TransUnion report might contain different information from your Experian report.

any free fico scores from any entity for the average layman without being a card holder or member of anything?