The big financial news over the weekend was the failure of both Silicon Valley Bank and Signature Bank. They failed, the FDIC took over and fulfilled its duties, and then the uninsured business owners convinced the Fed to backstop everything (aka “bail them out”).

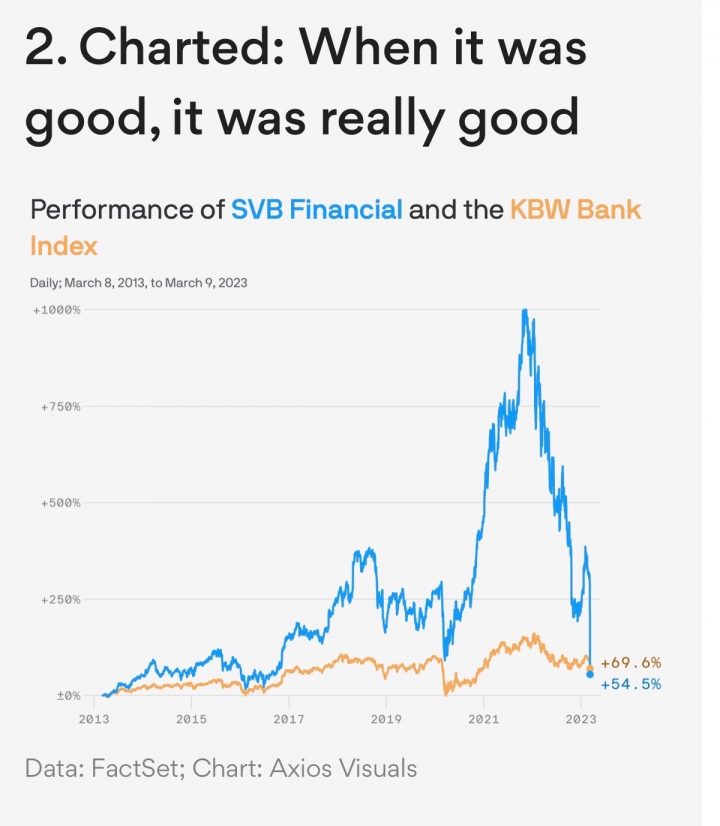

As a simple individual investor trying to keep his family assets safe, my first takeaway was simply that you can’t expect to see a bank failure coming. Silicon Valley Bank was the cool kid for a long time. Here’s a chart from Avios of its stock price vs. an index tracking bank stocks overall:

Most of Silicon Valley Bank’s deposits were from start-up businesses, but individual households had accounts with them as well. I don’t mean to pick on DepositAccounts, but they are a respected site and they gave Silicon Valley Bank a Health Grade of A:

How is the average investor supposed to do any better? This is why I don’t care about health grades for banks from anyone. I don’t need to examine their investment portfolio, underwriting standards, or stock price. As a depositor, either they have FDIC insurance, or they don’t.

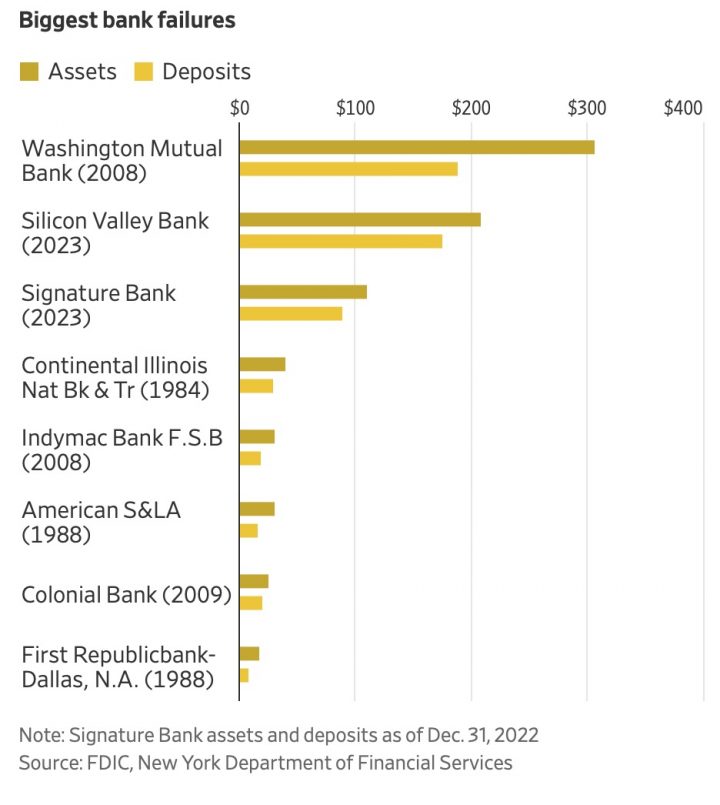

Big name banks can fail even if their assets are greater than their deposits. Silicon Valley Bank and Signature Bank are now the second and third largest bank failures ever (even inflation-adjusted), and only behind to Washington Mutual during the financial crisis. From WSJ:

I wonder how the list will look in a year?

As an individual, there is no reason to exceed the FDIC insurance limits.. FDIC insurance provides great peace of mind. Don’t waste it.

Got anywhere close to $250,000 in a single bank account? Know that the FDIC insurance coverage limit applies per depositor, per insured depository institution for each account ownership category. You may actually achieve more than $250,000 of total coverage at a single bank, depending on how you have titled your accounts. Here are the official online calculators:

NCUA Electronic Share Insurance Calculator (ESIC)

FDIC Electronic Deposit Insurance Estimator (EDIE)

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Hi Johnathan,

Thank you. Do you recommend having more than SIPC covered in your brokerage account or 401k account?

Jason K

>> aka “bail them out

This is not true. FDIC didn’t bail them out. Instead they’ll be using the bank assets to sell and payout as needed. No tax payer money was used here, nor is the money coming from FDIC directly. In other words, it’s not a bailout. It’s a win-win for everyone involved: FDIC, bank customers as well as taxpayers

Great Point – NO Tax Payer Money will be used for these two bailouts – Oh, what about the future banks that will be closed down and seized by the FDIC this upcoming Friday?? How about the following Friday??

BTW, this bailout will be covered by higher rates that FDIC will charge ALL other banks who have FDIC coverage.

So, while you’re technically right, that taxpayers will not pay directly…Bank Customer (i.e.. Taxpayers) will pay in the form of higher interest rates, fees, etc…to cover the cost of higher rates that the FDIC is now going to start charging banks!

Enjoy your WIN-WIN!!!!

Still pushing your ridiculous Fintech phony banks?

What is your take on the insurance provided by Fidelity and Merrill gor their individual and corporate accounts?

Thanks for your ongoing service. You provide a rational perspective and resources I can understand.

Thanks for this timely article.

I was thinking about what you may write about this all weekend.

When CNBC came on the air LIVE last night (Sunday Night) to discuss this bank failure (After Janet Yellen flip-flop’d on her “We will not bail out these banks”) and what to expect Monday morning…all while using soft tones in their voices I noted, I kept thinking….what’s Jonathan doing this weekend. What are his plans going forward with his assets??

Seeing the president come out this morning, while re-assuring, was also NOT re-assuring as he was explaining, in his angry voice, how taxpayers would NOT be held responsible (but didn’t mention the fact that banks would have to pay more for FDIC insurance – and thus anyone who banks will see higher fees from this mess). He tried to shift blame from taxpayer to depositors, hoping no one would notice that depositors are usually taxpayers…we’ll just pay in a different way than taxes!!!

Also, I didn’t like it when he tried to immediately shift blame to the prior administration, when his Treasury, under Yellen, could have rolled back anything they did not agree with in the prior administration…and I’m wondering, where is all the Stress-Testing going on??? Especially as the Fed is over in the other room raising rates…as banks sit there and look at their 0% bonds!

This ain’t over…and I fear the worst is to come.

This is like 2008 all over again, first it starts out with a little landslide, before the whole mountain falls down!!!

Yeller has the power to reinstate Dodd-Frank? I wouldn’t think so.

I’m not sure which Yellen comment you were commenting on?

So, Janet Yellen, as a US Senate approved head of the Treasury Department has a constitutional duty to enact the Dodd-Frank laws and enforce them with her various regulatory oversight abilities and agencies. Yes.

2nd Yellen comment

Yellen, as a US Senate confirmed head of the Treasury, could have reinstated any banking regulation she felt so compelled to strengthen or point out was law was flawed in her congressional testimony over the past two years – she did not. She had a Dem. House, Senate, and White House that could have passed anything she wanted…