I recently decided to convert my Vanguard mutual fund shares into each of their respective ETF equivalents. These were all held inside a Vanguard.com brokerage account. I remember first considering this mutual fund to ETF option way back in 2010 (aspects of that article may now be outdated). Instead of covering all of the possible decision factors, here I’ll just document my own personal factors and my experience completing the process.

Why did it take 14 years for me to convert my Vanguard mutual fund shares?

Back in 2010, here was my rationale for staying put:

- I had no plans to ever leave Vanguard as my primary brokerage custodian. Everything worked well enough; I had no complaints. My personal financial situation was also relatively simple.

- Vanguard was still simple. Minimal annoying fees. Things were somewhat barebones but everything worked for the most part. A human answered the phone relatively quickly. They sent me paper statements for free. My account only allowed mutual funds, no individual stocks. Vanguard had the vibe that “We’re different and that’s fine. People aligned with our views will find us.”

- The expense ratios for ETFs and mutual funds were either identical or nearly idential and both had the same tax-efficiency due to their share class construction. For a long time, the Admiral and ETFs remained at pretty much the same cost. When you buy ETFs, there are also bid/ask spreads and premiums/discounts to NAV to navigate. Any tiny difference in performance could be wiped out by all this “noise”.

- I preferred the simplicity and ease of dollar-based transactions. For example, back then if I had $1,000 to invest in VTI, at the current share price of $256, I would only be able to purchase three VTI shares and the remaining would remain in $232 cash.

Fast forward to 2024, and things were a little different:

- I am seriously considering leaving Vanguard as my primary brokerage custodian. This came after a few frustrating incidents and long hold times, in which I felt that it would be easier on my spouse if our assets were located at a place committed to top customer service. Essentially, an estate planning issue after handling my parent’s finances. There are definitely good and helpful people at Vanguard, but the level of service is not nearly as consistent as with Fidelity. If I consolidated, then there would also be one less major account to manage. Many outside brokerages won’t trade Vanguard mutual funds (besides full sales), so this was the main reason for converting to ETFs.

- Vanguard is trying to grow assets as hard as everyone else. Vanguard still has a low-cost structure, but now it just seems like it wants more, more, more. The CEO is leaving under questionable circumstances without a replacement ready from within, so they are likely hiring an outsider. (Tim Buckley started as Jack Bogle’s research assistant 33 years ago!) The Vanguard now serves me more browser pop-up windows (e-statements) and upsell ads (Advisory services) than both Fidelity and Schwab. For example, Fidelity mails me paper statements for free. This is helpful for older people that may lose track of accounts. Vanguard wants $25 a year for every single account unless I have $5 million. In that case, why not simply own Vanguard ETFs inside a Fidelity brokerage account? If Vanguard hires a CEO from another brokerage company, that just shows the direction the ship is heading.

- The expense ratio spread has widened slightly to the range of 0.01% up to 0.06% (VWO). This is still not a big deal to me, but it is apparent that Vanguard gave up trying to maintain parity and in the future the ETFs will always be cheaper. The trend is a wider gap over time, not a narrower one. I rarely sell (or even buy) these days, so I have minimal transaction costs.

- Vanguard now supports fractional share ownership for ETFs. Today, If I had $1,000 to invest in VTI, at the current share price of $256, I would be able to invest every penny and end up with 3.906 shares of VTI. Therefore, even if I do stay with Vanguard, I can still perform dollar-based transactions. The conversion is not a taxable event, so there is no tax impact.

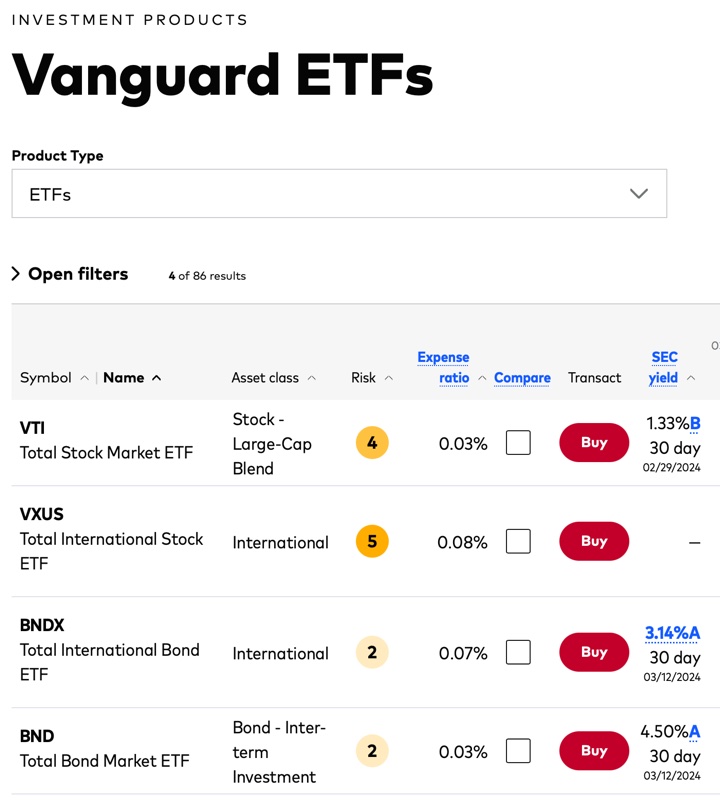

Which Vanguard mutual funds can your convert? Although it hasn’t been updated since 2019 and thus may be outdated, this Vanguard PDF listing which mutual funds are convertible to ETFs may still be useful. Here are the specific mutual fund and ETF pairings (with expense ratios) that I converted and their expense ratios as of March 2024:

- Vanguard Total Stock Market Index: VTSAX (0.04%) to VTI (0.03%). Difference of 0.01%.

- Vanguard Total International Stock Index: VTIAX (0.12%) to VXUS (0.08%). Difference of 0.04%.

- Vanguard Small-Cap Value Index: VSIAX (0.07%) to VBR (0.08%). No difference.

- Vanguard Emerging Markets Stock Index: VTIAX (0.14%) to VWO (0.08%). Difference of 0.06%.

- Vanguard Intermediate-Term Treasury Index VSIGX (0.07%) to VGIT (0.04%). Difference of 0.03%.

Again, the absolute differences in expense ratios aren’t that significant in my opinion unless you are talking in the millions. But the direction of the trend is pretty clear, and I do hope to have millions in each eventually. 🤑

Quick rundown of actual conversion process:

- Download all cost basis information. You should log into your account and download all of the cost basis information for all your mutual fund shares. This is especially true for non-covered shares. The cost basis for covered shares should carry over, but it’s better to be safe.

- I had to call Vanguard on the phone to initiate the conversion. Use the phone in your account or try 866-499-8473. (I could not find a way to do it online.) It took a couple jumps to find the right person, but after that the process was straightforward. As long as the request is entered before market close, it should go through at the end of that same day. Otherwise, it’ll be the next day. You will acknowledge that this is a one-way, non-reversible conversion. Again, you are not selling anything, so there is no taxable event.

- The next day, my shiny new ETF holdings were available in my account. and I was also able to confirm that all of the tax lots for cost basis carried through without an issue. The conversion was done at the net asset value (NAV) of the funds at market close. All of my mutual fund shares were converted, and I was issued fractional shares of ETFs.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

If you are looking for the cheapest way to invest in bonds, isn’t it best to buy the bonds directly, at least treasuries? I know with Fidelity there is no cost to buy treasuries.

For similar reasons, I did the same last year and moved all of the ETFs to Fidelity. I do maintain Vanguard accounts for their money market funds. The expenses are lower, so the yields are slightly higher than Fidelity. It also allows for some mental accounting, to have my emergency/contingency fund in a separate bucket from the long term investment bucket.

I currently use both Fidelity and Vanguard and while I prefer the former’s customer service, I find it’s easy to make charitable contributions of shares with Vanguard and I haven’t taken the time to study up on Fidelity’s forms.

Although you can now buy fractional shares of ETFs at Vanguard, I don’t believe you can sell fractional shares without selling your whole position. But it seems you can gift fractional shares.

I have had a DAF with Fidelity for 15+ years. It is super easy to use, and the minimum charitable contribution is $50, lower than Vanguard’s minimum.

Does Vanguard now allow automatic monthly set $ purchases of ETFs? That was the last thing holding me back from making this change. (I get that I can still do auto mutual fund monthly buys and periodically convert)

They don’t, that’s why I still have the mutual funds. As of mid March 2024

They do now, I started a couple months ago. Two things of note:

a) In order to set up an automatic investment into an ETF, it needs to be an ETF you already own.

This is easily done by purchasing $1 worth of that ETF in order to establish ownership, then later set up the automatic investment.

b) You have to set up a separate automatic investment transaction into ETF’s; “separate” meaning that if you also want to have an automatic investment into mutual funds, these transactions need to be set up separately. I think not a big deal.

c) The automatic investments are funded either from the account’s settlement fund, or I believe the funds can also be drawn from your bank account.

d) I am not sure if an recurring automatic investment transaction for an exchange (i.e., from a mutual find to an ETF, or vice-versa) is possible, nor have I looked into it. Probably in order to do this, you would have to set up an automatic transaction to sell X shares, with those funds going to your settlement fund.

Then, a separate recurring automatic purchase of the ETF, drawn from the settlement fund.

Jonathan, thanks for sharing this update. Does Vanguard have ETF version of Target Retirement Date funds as well?

I’m an estate planning attorney and believe Vanguard has the worst customer service of all the financial companies we regularly deal with. I often tell my clients they should have a very good, identifiable reason for being with Vanguard, because of the pain their loved ones will have to go through working with Vanguard compared to other similar companies.

How long has this been your experience? I ask because I was my father’s executor around a decade ago and Vanguard’s process for setting up the estate account was significantly better than all of the other financial companies I had to deal with. I unfortunately had to deal with many of them as he had a little bit in a lot of places.

I can definitely believe this is the case today.

My recent interaction with settling my mother’s estate with Vanguard was a nightmare. My attorney was on the phone line in a conference call for 57 minutes which cost me $500. When Vanguard disconnected the attorney related “was that as painful for you as it was for me”. Terrible service. A different brokerage rep related with good service it should take about 10 minutes. When I get time I am definitely considering moving from Vanguard for many different reasons. Just look at the limited number of Funds you can convert to ETFs compared to the number of Funds Vanguard has. You are working with information off the website that is date May of 2019.

What is holding me back to convert all my funds to etf is there is no equivalent target date ETFs. I don’t want to deal with the hassle of rebalancing individual ETFs to achieve my diversification. I can only achieve this with mutual funds so far.

I things change please let us know

Hey, that’s a really interesting article! Also, many of the comments are relevant! But please remember everything posted on here is really not correct! Why? Because vanguard will always remain the absolute lowest seller. True, there are index funds at Fidelity and other places that say they charge a lower annual fee. However, most of those places still try to charge administrative fees to make up that cost. In addition, vanguard has by far the widest selection of index funds to match all of the customers needs! Sure they’re not sending paper anymore because they’re trying to save the shareholders money. Remember vanguard is owned by us to shareholders and that will never change! And no I am not a paid shill for vanguard just a very loyal customer

Being in mostly target date mutual funds makes moving to another brokerage sound difficult… don’t love the customer service situation at Vanguard but not sure it makes sense to move yet.

I currently have split my funds between Vanguard and Fidelity. I have been very disappointed with Vanguard customer service the past few years and am thinking of moving to Fidelity too.

Many thanks for this article. I’ve long wondered what I was missing not moving to ETFs. This article breaks it down.

I haven’t noticed a problem with Vanguard customer service, but then when do I need them anyway?

I did a couple dozen RMD QCDs the past two years, and think Vanguard’s system is fairly painless. We request the check made out to the charity, Vanguard sends us the check, we scan it in case of audit, and then mail the check to the charity. For this alone I’m staying with Vanguard.

I’m sticking with Vanguard MMF for now, though do wish they’d mirror Fidelity’s free paper statements.

I all but full with Schwab, minimally with Vanguard. (Used to also have TDA accounts before they are now Schwab). Like ThinkorSwim.

I do also have minimums with Fidelity. I hesitated to move to Fidelity because there were instances where agents are didn’t have time a couple of times to help my elderly family member and seemed to easier to disconnect ) .

Schwab agents are more courteios.

Except for cash savings in a Money Market Fund, all I have at Vanguard is my Roth IRA which I have had for a couple of decades or more. My Roth IRA is just Mutual Funds.

Currently, I have recurring deposits every fortnight to reach the maximum IRA contribution each ear. Can these recurring investments be made into Vanguard ETFs?

If only Mutual Funds can receive automated recurring contributions, for those with an ETF equivalent, I suppose I could sell the Mutual Fund and buy the ETF every so often. Since it is a Roth, no tax information needed

Jonathan, do you know if one can buy fractional shares of vanguard PTFs in another brokerage such as Fidelity or Merrill edge? I use Merrill edge as my default brokerage due to its time with Bank of America and the perks associated with being higher status which you have profile before such as better cash back on their credit cards and so on.

I have had similar bad experiences at Vanguard lately. Was trying to move an elderly family member away from an abusive financial advisor. She’d had an account at Vanguard for about six months. Deposited some dividend checks into it. He called Vanguard and had her account flagged for fraud when she said she wanted to move. Was supposed to be cleared up in a few days. She’d wait weeks for a call back from Vanguard’s fraud department and never once received the call. Months went by. She finally had to make a complaint to the SEC to get her funds reissued to her. Basically EFF Vanguard and Raymond Jaymes.

But wait…there’s more. Lol. I won’t go into it. But yes. Vanguard is terrible these days. Schwab has been awesome.

Confirming that I did this myself and it was very easy. The hardest part was getting through the automated phone tree though I did get connected to the right person immediately.

One thing to be aware of if there are pending dividend payments in the near term (I think next few days) your conversion will be delayed until after that.

Vanguard charges me $25 per year not per month for paper statements.

You are right, it’s $25 per year, per account.

One thing with conversion that people should be aware is to do it after dividends are posted to the account for the given fund. Several years ago when I did my conversion the rep suggested this and asked me to call them a couple days later for one of my funds to convert.

I moved to Fidelity where I hold a combination of vanguard and ishares ETF. Quite happy with my decision.

Also an unintentional downside of moving to ETFs is that tax loss harvesting becomes harder now as you have to do so during the trading hours and grapple with bid/ask spread and market changes while you’re selling/buying ETFs.

Since I saw people try to go with Fidelity just today I tried to do a partial transfer to Fidelity from my Schwab account.

Well, it took about one hour and I was transferred to five different departments.

Initially, I submitted my application online but then apparently they have a known IT system issue they hold you on the phone for a lengthy time trying to walk you through and use different browsers, and different devices to resubmit your application for a partial transfer.

I ended up hanging up on the phone but the agent never called me back after putting me on quite extensive wait time.

Good luck to everyone.

I fear vanguard may go under? Dont know if my fears are real… poor customer service, disregard for customer wishes. Dont care attitude towards competition. These are all signs of a business that sooner or later will fold. Remember – Kmart, it folded despite its size.

How best to protect our investments in vanguard?

I do not want to move to fidelity ….do not want to keep all eggs in one basket.

Is SWPPX comparable to VFIAX in terms of cost? But if switch it will be a a taxable event so I am doomed.. any options? Are my fear real?

I also have an account with Interactive Brokers. There is a learning curve with them as they are best for trading. I did move some of my mutual funds to them and the process was smooth.

They have many ways to invest (forex, options, futures, etc.) even holding international currencies, I bought Swiss Franks and held them there. The agents are available 24 hours since they have offices Worldwide.