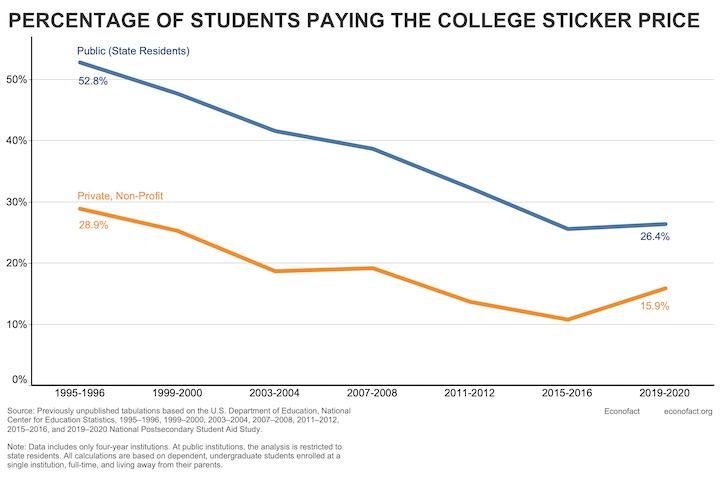

As the published prices for college tuition keep rising to astronomical levels ($100k a year?!), fewer and fewer students are actually paying the “sticker” price. As you can see below, the number is down to ~25% for public and ~15% for private 4-year institutions. This can make it very confusing for a family trying to plan for upcoming college costs.

This chart is taken from the Econofact.org article “How Much Does College Really Cost?” by economics professor Phillip Levine is one of the few articles I’ve seen that analyzes the the data based on household income level.

Colleges use a combination of need-based financial aid and “merit” aid to adjust the pricing of their product to balance their desired class composition and revenue requirements. The chart below shows “Typical College Net Prices At 4-Year Institutions by Family Income, Adjusted for Inflation”. This number does not include student loans and work-study funding.

For households under $100,000 a year, the numbers work out to well over 100% of your annual income for 4 years of tuition at both public and private schools. That seems especially daunting given the rising floor of basic costs like housing, transportation, and food.

Even for a family that earns $100,000 a year, paying for 4 years at a public university will average roughly $100,000 total. If you have multiple kids, that’s getting into the zone of another mortgage. A household earning $200,000 or $500,000 would also pay about the same $100,000 for 4 years of public university.

The private universities are where the higher-income households keep paying more as their income rises. A household earning $200,000 a year can expect to pay $200,000+ for 4-years at a private university.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Is there anything that can be done to ensure you get as much aid as possible?

There are drastic things you can do such as move to the state you want your child to go to so they can get in state tuition. Quit your job so that your income is not so high. Transfer Wealth not sure where.

The question is what is the break even point, where the cost of these drastic change out weigh the massive collage debt?

” number is down to ~15% for public and ~25% for private ”

Looks like you got those numbers reveresed.

Thanks, fixed!

We’ve been looking at a few of the Ivy League schools, as my daughter will be a senior this year and has excellent grades, SAT score, and extra-curriculars (i.e., there’s at least some chance she could get admitted). Although we reside in Florida, we narrowed in on Princeton because we have family in the area and because they claim that their financial aid program is one of the most generous in the country.

Per their website, the cost of attendance is $86,700 for the 2024-2025 school year. Their website states that “Princeton is attainable, accessible and affordable.” I beg to differ. Princeton’s website explains that “Most families will be asked to contribute 25% of income above $100,000 and 5% of assets (excluding primary residence and retirement accounts) above $150,000.” The income contribution limit seems fair to me. However, having to pay 5% of one’s total assets every year penalizes middle-income families who live below their means.

We have chosen to drive old cars, live in a smaller and older house, rarely eat at restaurants, and otherwise live below our means. Based on the savings and investments we’ve worked hard to accumulate over the years, we would be expected to contribute over $82K per year to Princeton. This equates to approximately 45% to 55% of our annual (pre-tax) income. Furthermore, our son will be going to college in two years and if we pay this amount for our daughter, then out of fairness we would need to do so for our son if he were to attend an expensive private school. We would then be paying over 100% of our income for the two years that they would overlap. Note that none of the Ivy League schools offer the merit aid mentioned by the author of the Econofact.org article. In fact, most competitive private schools don’t offer merit aid.

We’re stuck in the middle: not wealthy enough to afford private schools, but with too much in savings to get any meaningful financial aid. We will try to persuade our daughter to attend a Florida state school. With a state-funded scholarship (called Bright Futures) awarded to most high-achieving high school students, the tuition and fees are covered 100% at all the Florida universities.

Thanks for the thoughtful comment. I agree that the state school seems the way to go. I don’t have college age kids yet. However, when they come of age, I’m tempted to require them to pay for the majority of their secondary education (if they choose to go to college). I believe the most efficient choices are ultimately made if the consumer him or herself is ultimately responsible for the majority of the cost.

For example, my parents paid for me to go to college (the entire cost). I ended up going to an expensive private university. I am still enormously thankful for their generosity. However, had I been responsible for the majority of the cost (or, at a minimum, a portion of the cost), I would have chosen a state school that offered more “value.” And, today, at work, I’m surrounded by some very smart and capable coworkers from public universities.

My point is: If you really want to persuade your daughter to attend the less expensive state school (where she’ll likely receive a fine education), I recommend that she be responsible for some of the cost (even if it means she’ll have to borrow). Heck, you could even loan her the money at the market interest rate (I haven’t entirely thought through the wisdom of this…however, at least it will keep the cost of money in the family).

Just my opinion, of course.

Thanks for the response. I agree – ideally, students who choose to attend an expensive private college when they have the option to pick a perfectly acceptable (and mostly free!) state school should foot a portion of the bill. Unfortunately, I don’t see when my daughter (or probably any student vying for admission to top universities) would even have the time for a job. My daughter is in an International Baccalaureate high school program that assigns hours of homework each night as well as long-term projects; participates in math team competitions; plays in two orchestras; leads two clubs at school; does a couple of hours of volunteer work per week – and I’m sure I’m forgetting other activities. Even to be accepted to the University of Florida (Florida’s flagship public university), she needs to have near perfect grades and lots of extra-curriculars. The 2024 admissions acceptance rate for UF is 23%. It is tremendously more selective than when I attended many moons ago, when the acceptance rate was closer to 70%.

All this to say that her time now is best spent focusing on her school work and activities to raise her odds of being accepted to UF. She will likely want to apply to several private (expensive) schools as well. Your idea of loaning her the tuition funds is interesting. If for some reason she digs in her heels and wants to attend a private school, we’ll have to give that one more thought!

For college, the MSRP tuition rates and average costs are almost meaningless to the individual. You could apply to 3 different private schools that have tuition in the $75k ballpark and after aid and scholarships the actual price after aid/awards for them could be anywhere from $0 to $75k for the same student. I think theres less variability for public schools but even there it varies too. Two different public schools in the same state might give the same student considerably different amounts of aid or scholarships. That was all true when I went to college decades ago and it has gotten even more so since.

Annoyingly the only way to know how much aid you would get and what the schools would *really* cost you is to apply and fill out the financial aid form and wait.

So.. what you need to do is some solid research to find out how much aid schools actually give and what the NET cost is for people in your income level. And then apply to multiple schools and be more flexible on which one you go to. Applying to multiple schools is a bit of work but we’re talking about 10’s or 100’s of thousands of dollars here so that bit of work is well worth it.