The beginning of the year is a good time to check on the new annual contribution limits to the various available retirement accounts. Our income has been quite variable these last few years, so I regularly adjust the paycheck deferral percentages based on expected income for the year. This SHRM article has a nice summary of 2022 vs. 2021 numbers for most employer-based accounts.

The beginning of the year is a good time to check on the new annual contribution limits to the various available retirement accounts. Our income has been quite variable these last few years, so I regularly adjust the paycheck deferral percentages based on expected income for the year. This SHRM article has a nice summary of 2022 vs. 2021 numbers for most employer-based accounts.

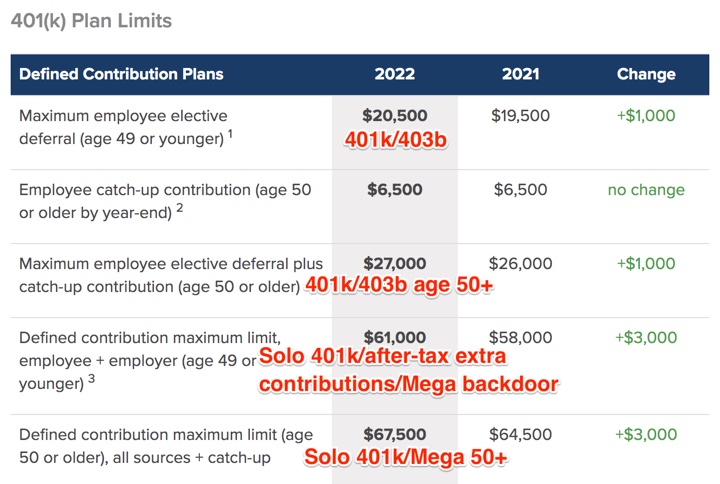

401k/403b Employer-Sponsored Accounts.

For example, I would break down the applicable limit down to monthly and bi-weekly amounts:

- $20,500 annual limit = $1,708 per monthly paycheck.

- $20,500 annual limit = $788 per bi-weekly paycheck.

If you are contributing to a pre-tax account instead of a Roth, you could also use a paycheck calculator to find the detailed impact to your take-home pay.

The higher numbers are for those folks that have the ability to contribute extra money into their 401k accounts on an after-tax basis (and potentially perform an in-service Roth rollover), or those self-employed persons with SEP IRAs or Self-Employed 401k plans.

The investment options in 401k plans have also improved on average steadily over the years with lower fees and costs, allowing your money to compound even faster.

Traditional/Roth IRAs. The annual contribution limits is unchanged from last year, $6,000 with an additional $1,000 allowed for those age 50+.

- $6,000 annual limit = $500 per monthly paycheck.

- $6,000 annual limit = $231 per bi-weekly paycheck.

Most brokerage accounts (Vanguard, Fidelity, M1 Finance) will allow you to set up automatic investments on a weekly, biweekly, or monthly basis. As long as you have enough money in your linked checking account, the broker will transfer the cash over and then invest it on a recurring basis. You may even be able to sync it to take out money the very same or next day as when your paycheck hits.

Health Savings Accounts are often treated as the equivalent of a “Healthcare IRA” due the potential triple tax benefits (tax-deduction on contributions, tax-deferred growth for decades, and tax-free withdrawals towards qualified healthcare expenses). This assumes that you have a high-deductible health insurance plan, you can cover your current healthcare expenses out-of-pocket, you can still afford to contribute to the HSA.

Even though I’ve been parroting the “standard personal finance advice” to raise that contribution percentage and save as much as you can in your 401k for years and years, it still holds true. There is some true mind trickery when the money never touches your bank account. The easiest way for me not to eat potato chips is not the have them in the house. (My nemesis is that Costco mega-sized bag of Himalayan Salt Kettle Chips…) The easiest way to make sure you don’t spend the money that you want to invest, is to never have it touch your bank account.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

And definitely be mindful of the limits; If you bust, you need to cure it immediately to avoid an excise tax on over-contributions for every tax you you’re in violation, and you pay a penalty on any gains regardless. Both excess contributions and gains must be withdrawn. This is particularly messy if you have stocks rather than a CD or similar which is the IRS example. The form you file also must be notarized.

Good warning!

One thing I’m not sure (maybe Jonathan can have a blog on that at some point?) is if it still makes sense to contribute to a non deductible IRA if you can’t do the IRA roth backdoor. Would it be more beneficial to (say) contribute $6k to the non deductible traditional IRA vs. putting that $6k to a normal taxable account?

I think it comes to tax treatment:

– taxable account earnings -> treated as short/long term capital gains

– earnings in the trad IRA -> treated as income

I’m assuming that the reason you can’t do a full backdoor roth IRA is because you have existing pre-tax IRA assets with significant unrealized capital gains? One thing I would explore is the ability to roll over an IRA into your current 401k or even a Solo 401k if you have any self-employed business income. Then you could do the Roth conversions.

I did some posts on non-deductible IRA way back in 2006 before the income limit was removed for Roth IRA conversions. Basically, it depends on what you plan to hold in them. If you put tax-inefficient assets like REITs and bonds in it, the non-deductible IRA will likely beat a taxable. If you put a low-turnover ETF like VTI that doesn’t distribute any capital gains prematurely, then the taxable may win.

https://www.mymoneyblog.com/should-i-contribute-to-a-non-deductible-ira-better-than-taxable-account.html

You’re totally right. I can’t (easily) do the backdoor roth IRA due to pre-tax IRA assets with significant gains. I did look at moving those to my 401k but that is tricky as well. (Short story is that I’ve been using Betterment “tax-coordinated portfolio” where I have a Roth IRA, a Trad IRA and a taxable account all coordinated….taking out the Trad IRA portion would likely mean creating large tax events for the rebalancing of my taxable account).

Thanks for linking your article on the subject. It’s fantastic and answers all my questions! It’s also crazy how a 2008 article can still be so relevant.

Also note that my situation is pretty unique but if congress eventually removes the IRA Roth backdoor, then it will become a question for way more people.

If congress does away with backdoor Roth IRA, what happens with post tax 401k contributions when you retire from your employer and want to do a rollover/rollout? My original plan was to roll the pretax contributions to a Trad IRA, the earnings from the post tax contributions to a trad IRA, and the post tax contributions to a Roth IRA. If you cannot roll these post tax contributions into a Roth IRA account type, what kind of account would they go into?

You probably know this but if possible, you would first want to ask for an in-service rollover to a Roth IRA now so you can avoid paying taxes on any gains.

Otherwise, I can only assume that it will all be treated like a non-deductible “regular” IRA. You’ll owe taxes on all withdrawals, even if you contributed post-tax money initially.

How are they keeping the IRA contribution limits unchanged after 6% inflation last year? The Social Security wage base max went up by $4200. SMH.

Two tips on HSA contributions:

1) The over 55 catch up contribution amount is PER SPOUSE but each spouse has to put it in their own HSA. So spouse A can put $7300+1000=$8300 in theirs and spouse B can put $1000 in their HSA.

2) Each spouse is allowed one “Qualified HSA Funding distribution” from a non-Roth IRA to their HSA per lifetime. This works best if you are retired and not getting any employer match. If you have a 401k, you can do a non-taxable rollover of the contribution amount to a rollover IRA then rollover that to HSA from there. You dont get the tax deduction for the contribution amount, but you remove that taxable amount from your IRA/401k so its a wash (over time).