The Accidental Slumlord

A writer whose lives in Massachusetts buys a two-unit rental property in Pocatello, Idaho for $62,750 during the housing boom. Read what happens when he actually visits his house and deals with his tenants.

OptionsHouse Brokerage – $3.95 Stock Trades

Another new discount online brokerage with cheap trades, but actually won #1 in Trade Experience in recent Barron’s Broker Survey, beating out E-Trade. Offers flat-rate pricing at $3.95 for stock trades regardless of number of shares, and $9.95 flat for options (no per-contract fee). $1,000 to open, $100 balance needed to trade. Anyone try them?

New research sheds light on the habits of successful savers

Includes a lot of expected characteristics, but worth a skim to see how you compare.

AMC Theatres A.M. Cinema

“A.M.Cinema, a new program providing early-morning guests the opportunity to see first-run movies at the best ticket price of the day. The program invites moviegoers to visit their local AMC theatre before noon Fridays, Saturdays, Sundays and holidays to enjoy ticket prices of $4, $5 or $6 depending on the theatre and market.”

F*** my job, Selling Everything!

Found in the Best of Craigslist section. Have you ever had the urge to simply sell everything you own, cash out your investments, quit your job, and just travel the world until the money runs out? This guy did.

Credit Bailout: Issuers Slashing Card Balances

People are haggling directly with credit card companies to lower their amount owed. However, the articles neglects to go into detail about the impact on credit scores. I suspect that there will still be significant damage to your credit if you “settle” in this way.

Tuesday 10: Good stuff from other personal finance blogs

- How much do people spend on clothes by Jim at FreeBy50

- My IRA asset allocation at GreenPandaTreehouse

- Things You Own End Up Owning You by David at MyTwoDollars

- On Spending Consciously by Patrick at Cash Money Life

- Pay attention to your money by Single Ma at Fabulous Financials

- Retired at 31: An Early Retirement Story by FrugalTrader at Million Dollar Journey

- Tax Deductible Mortgages in Canada by Mr. Cheap at FourPillars

- Mid Year Financial Checkup by Madison at MyDollarPlan

- Fun Fund Sell-o-Meter by J at BudgetsAreSexy

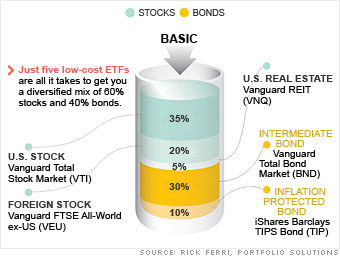

I saw that Vanguard has a new account called the

I saw that Vanguard has a new account called the

You can also earn points by taking surveys, playing flash games, using specific grocery coupons, using their Search toolbar, shopping through their online mall portal, and other activities. I primarily just stick to the e-mails, and run through them in batches when I’m waiting for some process to run.

You can also earn points by taking surveys, playing flash games, using specific grocery coupons, using their Search toolbar, shopping through their online mall portal, and other activities. I primarily just stick to the e-mails, and run through them in batches when I’m waiting for some process to run.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)