I couldn’t help but catch some of the news coverage about this week’s continuing fallout from subprime loans, the resulting stock market wobbles, and the overall tightening of the credit market. CNBC’s ratings must be through the roof. Then tonight I stumbled upon a post on the housing bubble blog Patrick.net about it being a point of inflexion:

I believe we are now at what will be seen as the inflexion point. It took a long time to get here, but the housing bubble is finally recognized as a pass? concept. The real debate now is how much and how long of a correction.

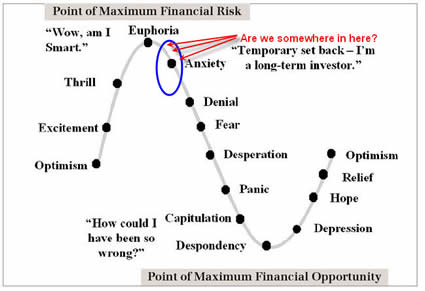

This reminded me of the graph below, which I brought up when I asked If Real Estate Prices Are Cyclic, Where Are We Now?. This was back on January 4th, 2007.

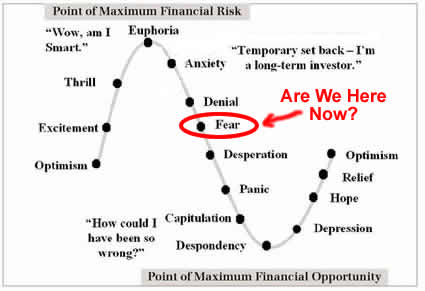

At that time, I guessed we were somewhere around Anxiety. Now, seven months later, where are we now? I’d say we’ve moved past both Anxiety and Denial already, and we are solidly at Fear. Mathematically, the inflexion point (aka inflection point) is where the second derivative changes sign. Guess where the inflexion point on such a sinusoidal graph is?

As this CNN Money article about tighter lending standard suggest, I may be well positioned to benefit from this progression:

In addition, tightened lending standards stemming from the subprime crisis likely mean fewer buyers, pushing down home prices. The one catch is this: You’ve got to be a buyer with good credit, a low debt to income ratio, a healthy down payment, verifiable income, and looking to finance less than $417,000 (the cutoff for so-called jumbo loans).

Bring on the Desperation! 😉

In an effort to gather even more information for Google Maps and to promote advertising on it, Google is offering now work (as an independent contractor) under the role of Google Business Referral Representative:

In an effort to gather even more information for Google Maps and to promote advertising on it, Google is offering now work (as an independent contractor) under the role of Google Business Referral Representative:

Starting a new job means signing up for benefits. In terms of health insurance, this has usually boiled down to choosing either an HMO or PPO plan for us. I still have never been offered the option of a High Deductible Health Plan (HDHP) with a

Starting a new job means signing up for benefits. In terms of health insurance, this has usually boiled down to choosing either an HMO or PPO plan for us. I still have never been offered the option of a High Deductible Health Plan (HDHP) with a

Unless you have unlimited ATM access to the Bank of Mom and Dad, most of us keep some money around for the unexpected. I haven’t been worrying about this much, as we have over $80,000 in cash split between our savings accounts at Washington Mutual (5% APY) and

Unless you have unlimited ATM access to the Bank of Mom and Dad, most of us keep some money around for the unexpected. I haven’t been worrying about this much, as we have over $80,000 in cash split between our savings accounts at Washington Mutual (5% APY) and  The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)