I couldn’t help but catch some of the news coverage about this week’s continuing fallout from subprime loans, the resulting stock market wobbles, and the overall tightening of the credit market. CNBC’s ratings must be through the roof. Then tonight I stumbled upon a post on the housing bubble blog Patrick.net about it being a point of inflexion:

I believe we are now at what will be seen as the inflexion point. It took a long time to get here, but the housing bubble is finally recognized as a pass? concept. The real debate now is how much and how long of a correction.

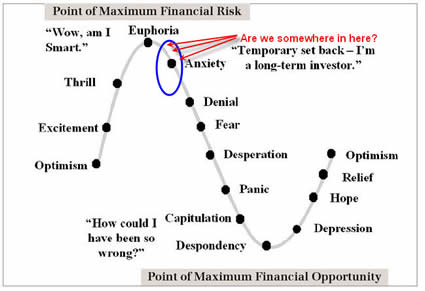

This reminded me of the graph below, which I brought up when I asked If Real Estate Prices Are Cyclic, Where Are We Now?. This was back on January 4th, 2007.

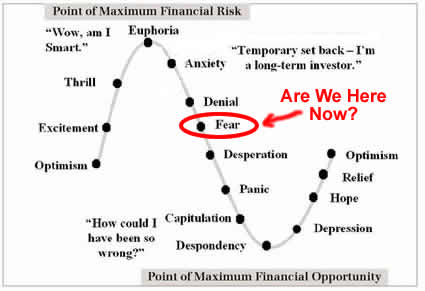

At that time, I guessed we were somewhere around Anxiety. Now, seven months later, where are we now? I’d say we’ve moved past both Anxiety and Denial already, and we are solidly at Fear. Mathematically, the inflexion point (aka inflection point) is where the second derivative changes sign. Guess where the inflexion point on such a sinusoidal graph is?

As this CNN Money article about tighter lending standard suggest, I may be well positioned to benefit from this progression:

In addition, tightened lending standards stemming from the subprime crisis likely mean fewer buyers, pushing down home prices. The one catch is this: You’ve got to be a buyer with good credit, a low debt to income ratio, a healthy down payment, verifiable income, and looking to finance less than $417,000 (the cutoff for so-called jumbo loans).

Bring on the Desperation! 😉

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

“Guess where the inflexion point on such a sinusoidal graph is?”

Wherever the derivative of sin(x) equals 0.

Sorry, critical points are about the derivative. Jon is right. Inflection points are about the 2nd derivative (the derivative of the derivative). Assuming that you mean your graph to be a sine curve in the first place (since it looks like one), it would be where the derivative of cos(x) equals 0.

I think this wave will cutoff the bottom three points, and go from panic to hope…

I hope you’re wrong… I have an awful feeling you could be right.

I have to agree with Andy L. and suggest we’ll have a quick recovery. The Dow will drop another 1,000 points in the next couple weeks and then things will be a-okay. We’ll be in Hope by the end of the year.

Oh, we’re definitely in full-blown panic now. Fear was two weeks ago. 🙂

As a person fresh out of college looking to buy a home in 2-4 years, I say WOOOOOHOOOOOO, bring on a housing market crash.

Market risks they talk about. It’s actually the risks you take. Fear does play a major role in achieving your goals. Are you willing to take them or not.

Success or failure, is not a choice. Neither is it an option. It’s two entities that determine success from failure. Mathematical calculations can be an endless road and an eternal puzzle.

One has to move on if you want to make those dreams a reality. Money, money, money isn’t funny, it isn’t a rich mans world.

You see the way I look at it, it really isn’t a rich mans world. Cause money isn’t everything. It’s your attitude that determines your success.

It’s those good principles, self control, the character, the morals and so on. But most of all it’s the love that one has for each other that tells a story of success.

Look at all those great people who shared with mankind their dreams. Today we experience it in our day-to-day lives. Electricity, Engineering,Medicine, Business, Technology…

What is it that drives a man to success. What is it that makes a man do the things he does that most of the time goes beyond mental or mathematical calculations.

I think you should have had it figured out by now, what words cant explain…

Best Regards,

Sajjid Manuel

Andy L’s sentiment (quite common, I think) leads me to believe we’re still in the denial stage. While many are accepting that inventory levels are far outpacing demand/sales, and the media admits to a housing slowdown, the fact that prices have only declined a very marginal amount (even in bubble areas where the declines are still a long way from historical averages) shows people are still denying that their houses are no longer worth what they were just a year or two ago. They are denying it to themselves that they need to drop their prices. Eventually, prices will fall through the floor as panic/capitulation/despondency sets in. I expect in many “bubble” areas to see prices fall in line with about 130-140 x’s monthly rent (vs. the 165-175 x’s monthly rent many are priced at now). Keep saving that down payment money and be ready to pounce. I give it about 3-5 years and then plenty of bargains will abound.

The points where the derivative are zero are the flat parts of the graph (Euphoria and despondancy).

the inflection points are where the second derivative of sin(x) equals zero, like convexity on a bond.

@siggyboss

actually in the article he was talking about the inflexion, meaning concavity. That usually changes signs when the second derivative is 0, not the first. So you’re looking for the where ( – sin (x) ) = 0 which is right at 0. On his chart its right around the circled area marked “Fear.”

It means from that point forward the first derivative (AKA the slope of the tangent lines) is increasing again and the “crash” you are experiencing is slowing pace and will eventually move back the other way into positive territory.

I’m already looking at a lot of bank short sales, so indeed some people are at desperation. A lot of flips gone bad.

I agree with those saying that we are still ‘in denial’ phase. Just check out all the housing bulls here. The graph assumes people are sensible, I think it will not be a symmetrical sine wave rather it would be an ugly sine wave with lows two times the highs. Hang on tight, the more you keep people in denial, the more it will fall. There are still people fighting for houses in some parts of bay area. No end to this madness. I still see around 1000 advertisements on TV about zero downpayment, no docs, all approved loans. Until these ads stop, there is no ‘Fear’ or ‘Desperation’.

I have to say, while appreciate the idea, and the curve, and the thinking, I can’t help but find it somewhat hypocritical that and indexing, non market-timing investor such as yourself, would then think that it is possible to time the market with respect to a real estate purchase. Market prediction of any sort is virtually impossible (black swans wait around every corner…) and whether it is for bonds, domestic equities, REITs, or the purchase of your house, trying to time the market is usually an exercise in futility. If you buy a house, do so because you love it and want to live there, and will do so long term. Buying because we are in a dip (or crash for that matter) or because you think the market is bound for a rebound, is the same as saying that you know when to buy a REIT ETF or mutual fund – if you knew you could buy it at the inflection point or at the bottom and profit handsomely, you would do so. Real estate markets do take longer to play out than turn on a dime equities, but the principle remains the same. Buy and hold, eventually you will be rewarded.

“I?m already looking at a lot of bank short sales, so indeed some people are at desperation. A lot of flips gone bad.”

Does that “short” mean like shorting a stock where you sell it before you buy in order to make money in a down market?

If so where can you “sell” a house before buying it? What this bank short sales? can you clarify?

Don’t worry, we are definitely looking for the house that we love. Otherwise why spend all this time looking at all. Doesn’t mean we shouldn’t hope for a crash, or take such things into account when negotiating for a price with the seller. I think many people do look at such things. The real estate market does move slowly.

A short sale is kind of a “avoid foreclosure” sale. Nolo definition:

Interesting replies. And I agree with others that I’m surprised with the bullishness of the people on this board, which would lead me to believe that we are in DENIAL. If you go to any housing bubble blog, everyone is looking at the same curve and saying we are in panic or worse. But of course, someone who goes to a housing bubble blog is anticipating and waiting for the drop, and would like nothing better for the market to drop for self-gratification of being right, thus the lower rating. Anyway, if this board represents the common layman, then I would say we are in DENIAL.

I’ve only been investing for a little over a month. Normally I’d be pretty bullish in the market but I’ve learned rather quick that the housing/financial markets are in a big rut. The last few liquidity injections by the Feds signals something is wrong and now they’re trying to not get caught with their pants down. I hate being bearish but unless something dramatic happens, I don’t see a recovery for a while. My guess is if things continue on this heading, we’ll be in danger of seeing a deflationary period instead of the mild inflation the Fed is worrying about.

Just like a poster above, I’m getting out of college soon and hope the housing market does stay in the current slump. I don’t want to wish negative things on the hard working Americans though.

just to follow up, though it is wholly anecdotal, I was out tonight w/ several friends and colleagues (i.e., teachers) and had to sit through one person’s assertions that “though the market isn’t as ‘intense’ as it was, our house is still worth $210,000.” She was crowing about the incredible “gains” they’ve realized vs. their initial buying price (while I was trying not to gag/roll my eyes). I didn’t bother to point out to her that that number (210k) was over 200x’s monthly rent (I live in a bubble area, obviously… where prices have even decline 10% and are still that high), or that our area has seen an incredible spike in foreclosures and has an endless inventory of new builds from builders like Pulte. Not to mention these new build are seeing enormous price drops… still, I held back, because you just don’t make/keep friends (or keep the conversation light over a nice meal) when you challenge people to accept reality. I agree that if you’re a “buy and hold” investor, there’s not a *huge* difference between trying to buy toward the bottom of the dip vs. the top. But, seriously, real estate is cyclical (though, admittedly, the cycles are difficult to peg down) and it is obvious that in some areas, RE is vastly overpriced. The only thing I have to add to those like enonymous is… would you rather buy my friend’s house right now for $210k (their overinflated estimated valuation) or wait 3-5 years, rent at a substantial savings (especially when you factor in the savings on property tax/maintenance), and then buy the same house for ~$140-160k? Sure, if you “buy and hold” the 50k might not make a *huge* difference to some people, but given the power of compounding (and the fact that responsible investors are banking/earning interests on the savings they are reaping from renting), that $50k = $100k in 7 years, 200k in 14 yrs, 400k in 21 yrs, 800k in 28 yrs, and $1.6mil in 35 yrs (retirement). That is, if you buy into the whole mantra that money invested for retirement, earning ~7% returns, will double every seven years. I’m a bit dubious on those numbers, but I think the points stands that there IS something to trying to at least buy when prices are more in line with historical averages. The fact that so many people have disregarded these fundamentals is one of the reasons we’re in such a mess. Oh, and while I understand many people’s desire to see a crash so they can get a deal, I don’t think many of you realize how bad things will get if real estate truly tanks. How will you buy anything if your job suddenly disappears, even if it isn’t directly reliant on RE? Even a job like mine (teaching), with an enormous demand (largely because the wages are so bad) isn’t completely stable when the economy suffers due to declining tax revenues, especially those raised in relationship to property taxes. I feel like a broken record, but I think more ppl need to listen to “Dr. Doom” (Peter Schiff) about the RE crash and the merciless misery it will pass onto the dollar: link

I feel like some of you bulls are catching a knife on the way down, but think it’s some kind of a steal. More power to you, but I’m saving and living rent free with family until prices are back in synch with historical averages.

re: Jorge

People have compared this housing bubble to that of Japan’s housing bubble 20 year ago. fyi, the average home prices in Japan have been decreasing for the past 20 years. Actually, I believe last year was the first year that the average home prices in Japan inched upwards. Of course, in 75% of Japan, home prices are still falling, and its only Tokyo and large cities that are making the “average” prices of the entire country increase.

Also, Japan is still pretty much in a deflationary cycle. Hence, the free money that they are giving away to try and make people spend…i.e. interest rates at 0% for the longest of times. Low interest rates sounds good, but it didn’t help revive their economy, i.e. tough for young people to get a job.

So be careful of what you hope for, as the current slump could last 20 years….or it could last 6 months…what do i, or anyone else know. But I do agree that I don’t want to wish negative things on others, especially my parents generation who are relying on 401ks and equity in the homes to retire.

I wish I wasn’t in debt or I’d be house hunting like crazy! That’s one of the best aspects of the cyclical nature of markets is the down-turn or correction – the opportunity to make some potentially great investments.

re: Nathan

Japan is losing people, would make sense for housing to continue to drop as demand falls. A good way for them to counteract this is probably to destroy housing stock as the population decreases, maybe use the land to grow biofuel instead. I also heard from a friend that used to live there that a house over there isn’t considered an investment as they basically tear it down and rebuild every 30 years. The US on the other hand is growing in population, eventually demand will catch up with supply if supply stops or slows for long enough.

Our parents will be fine, they have the political clout to make things happen for them. If that doesn’t work it means everyone is suffering greatly but at least they won’t be alone since at that point their kids will probably be living with them.

Hi Jonathan

Can you throw some guidance on how to look for forclosures, bank shorts in your area

Re: timing

Market value (prices) and intrinsic value often diverge. Timing discount to market value is speculation, whereas waiting for discount to intrinsic value is investment. (Paraphrasing — perhaps mangling — Benjamin Graham, but I think these truisms apply to any financial operation, including real estate transactions.)

>Japan is losing people,

Yes, Japan, for the first time, last year was the first year deaths outnumbered births, ie population decreased.

However, 15 years ago, a declining population wasn’t on anyone’s mind in Japan. So that wouldn’t explain why they were in the midst of an already 5 year housing slump/deflationary spiral.

Anyway, I’m not trying to argue that the US will become like Japan. I was just pointing out to a poster who was hoping that the decline would continue until he graduated from college that the markets don’t always work like that. Its not always so nice and neat that in a year or two, the market will bottom and then take off again.

As for using land to grow biofuel, you do know that there is 120 million people living in the size of California, and that of that small land, 2/3 or more is mountainous and practically uninhabitable. Using the same argument, housing in the US shouldn’t cost more than $25k or some low figure because there is so much land in the US, too much.

>I also heard from a friend that used to live there that a house over there isn?t considered an investment as they basically tear it down and rebuild every 30 years.

YES, this is true. But what I said was wrong but point is still the same. Land values, not housing prices, rose for the first time last year. They keep track of the value of land, per square meter, if I’m not mistaken.

@ Sam S – Short selling – is a general term that indicates the seller is expecting the price of the underlying asset (be it stocks, homes, commodity, etc.) to fall. It just so happens that it’s mostly associated with stocks — probably because stocks are the most commonly traded form of asset ownership.

The chickens are just now beginning to come home to roost. Expect flocks… The volume of (sub-prime) Adjusted Rate Mortgages sold in 2002 & 2003 that “adjust” after a 3- or 5-year period pales in comparison to the volume that sold in 2005 and early 2006. So the number of foreclosures can only be expected to increase significantly through 2010 — especially if interest rates aren’t drastically cut. And since the overly-generous rate reductions of the recent past play a significant role in what’s happening now, i don’t expect any major cuts over the next 3 years.

Jonathan, definitely consider CW’s poignant comment:

“I feel like some of you bulls are catching a knife on the way down, but think it?s some kind of a steal. More power to you, but I?m saving … until prices are back in synch with historical averages.”

I bet all those people who signed onto ARMs up to a couple months ago will be very relieved to hear that this will be short lived. Otherwise they’d be forced to foreclose just like those who signed into them 2 yrs ago! My point is that there are people in alot of these “categories”, from the anxious/denial/fear ARM holder, to the fear/panic seller, to the capitulation/despondent/depressed foreclosure to the hopeful prospective buyer. The only thing that is certain is that there is no thrill, excitement, or euphoria in this market, and there’s a long way to go before it gets there again.

I support what Nathan says…we are in denial in the hot areas of the US, although to generalise in a country of 300m is just silly. Denial in a market looks like a Mexican Standoff – the market cannot find a balance between supply and demand so the price does not change but transation volumes fall…just like we have not in California and Florida. So the question is…who blinks first? In a “normal” housing market crash, drievn by economic recession and unemployment, the supply side blinks as foreclosures and people’s natural need over time to move house (kids, jobs etc) motivates them to do a deal…and we are onto local capitulation and wider panic. Remember that the typical total hosue price cycle takes 14-15 years and the typical downturn is -5 years…with the low point of the REAL (i.e. inflation adjusted) house price bottom coming in year 4. That’s 2010! Enjoy the ride down…