![]()

Here’s an update on my $2,000 investment into the Fundrise Income eREIT. Fundrise is taking advantage of recent legislation allowing certain crowdfunding investments to be offered to the general public (they were previously limited only to accredited investors). REIT = Real Estate Investment Trust. This specific eREIT initially sold out of its $50 million offering, but Fundrise has since opened regional eREITs called the West Coast, Heartland, and East Coast eREITs. The highlights:

- $1,000 investment minimum.

- Quarterly cash distributions.

- Quarterly liquidity window. You can request to sell shares quarterly, but liquidity is not always guaranteed.

- Fees are claimed to be roughly 1/10th the fees of similar non-traded REITs. Until Dec 31, 2017, you pay $0 in asset management fees unless you earn a 15% annualized return.

- Transparency. They give you the details on the properties held, along with updates whenever a new property is added or sold.

Why not just invest in a low-cost REIT index fund? I happen to think most everyone should invest in a low-cost REIT index fund like the Vanguard REIT ETF (VNQ) if they want commercial real estate exposure. I have many times more money in VNQ than I have in Fundrise. VNQ invests in publicly-traded REITs, huge companies worth up to tens of billions of dollars. VNQ also has wide diversification and daily liquidity. But as publicly-traded REITs have grown in popularity (and price), their income yields have gone down.

Fundrise makes direct investments into smaller properties with the goal of obtaining higher risk-adjusted returns. They do a mix of equity, preferred equity, and debt. Examples of real-life holdings are a luxury rental townhome complex and a $2 million boutique hotel. From their FAQ:

Specifically, we believe the market for smaller real estate transactions (“small balance commercial market or SBC”) is underserved by conventional capital sources and that lending in the market is fragmented, reducing the availability and overall efficiency for real estate owners raising funds. This inefficiency and fragmentation of the SBC market has resulted in a relatively favorable pricing dynamic which the eREIT intends to capitalize on using efficiencies created through our technology platform.

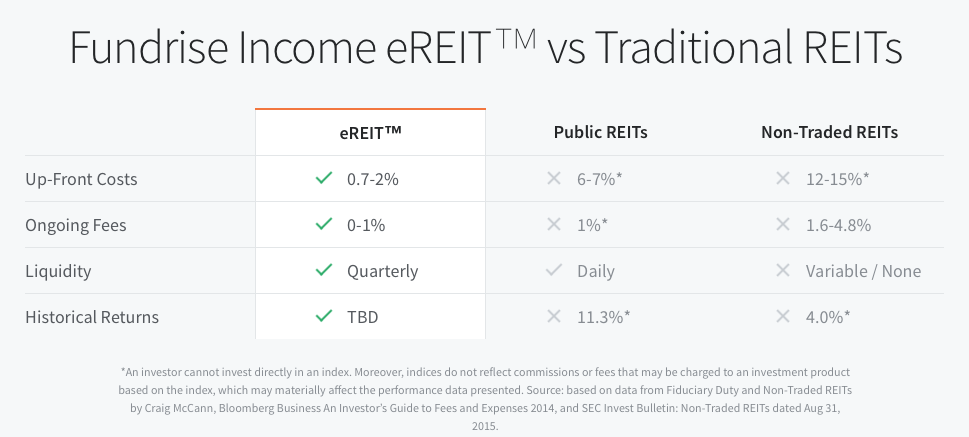

Here’s a comparison chart taken from the Fundrise site:

Quarterly liquidity. As noted, the investment offers the ability to request liquidity on a quarterly basis, but it is not guaranteed that you can withdraw all that you request. In addition, you may not receive back your full initial investment based on the current calculation of the net asset value (NAV).

Update: I tested out the quarterly liquidity window and was able to withdraw my funds in a simple process and without issue.

Dividend reinvestment. I chose to have my dividends paid directly into my checking account. However, you can now choose to have your dividend automatically reinvested across currently available offerings.

Tax time paperwork? All you get at tax time is a single 1099-DIV form with your ordinary dividends listed in Box 1a. That’s it. Every other box is empty. This is much easier than dealing with the 10-page list of tax lots from LendingClub or Prosper.

Dividend income updates.

- Q1 2016. 4.5% annualized dividend was announced. This was the first complete quarter of activity, so the dividend was not as large as when funds became fully invested. The portfolio had 13 commercial real estate assets from 8 different metropolitan areas, with approximately $31.5 million committed.

- Q2 2016. 10% annualized dividend announced, paid mid-July. Portfolio now includes 15 assets totaling roughly $47.25M in committed capital.

- Q3 2016. 11% annualized dividend announced, paid mid-October.

- Q4 2016. 11.25% annualized dividend announced, paid mid-January. Portfolio now includes 17 assets and all of the $50 million has been invested.

Screenshot from my account:

Recap and next steps? It has now been over a year since my initial investment in the Fundrise Income eREIT, designated my Real Estate Crowdfunding Experiment #2. I’ve earned $183.01 in dividends on my initial $2,000 investment. The quarterly dividends have arrived on time, I get regular e-mail updates, and it has been nearly zero-maintenance. I still accept the possibility of wide price fluctuations, as with any real estate investment.

Update: I tested out the quarterly liquidity window and was able to withdraw my funds in a simple process and without issue. Fundrise is still accepting direct investments into some of their eREITs, but I am now looking to re-invest into their new Fundrise 2.0 system, which has a new $500 minimum and allocates across multiple eREITs. You can sign-up and browse investments at Fundrise for free before depositing any funds or making any investments.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

It’s difficult to directly compare fees between the vanguard reits and the fundrise reit. In vanguards case they invest in other property holding companies which have many layers of management fees and so on. Where as the fundrise fees are pretty much all that stand between the investor and the direct property.

VNQ shows a fees of 0.12%. Are there more fees in addition to that ?

I hold money in Fundrise as well as in VNQ.

Yes, but they are not charged by Vanguard. Take a look at the top holdings of VNQ: http://portfolios.morningstar.com/fund/holdings?t=VNQ

You will see that they are other REIT’s, mall owners, storage owners etc… All of these companies charge fees, in some case very significant fees to manage the actual properties. Whereas with FundRise, there are fewer layers of fees between you and the property.

I’m not advocating for FundRise but just pointing out that it is difficult to compare fees.

The relevant comparison for Fundrise shouldn’t be to Vanguard’s VNQ REIT index fund; it should be to one of the underlying REITs that VNQ holds. Any one of those REITs itself holds a lot of properties generally spread out over a large geographical area.

Thanks for the update. I’ve been investing with Fundrise (in this fund and a couple others) for the same timer period. Regular updated received via email, their support team is responsive via email, and the company seems to be in a better spot after some internal issues. They are also selling part of the company via their platform so you could have participated in a non-public IPO (the way I understand it) of sorts. Keep us updated on liquidating your shares.

Thank you for this interesting post. Does this REIT finance or own the real estate? It is a noteworthy distinction for comparing risk. The Vanguard REIT fund is comprised of REITs that generally own the real estate.

Jonathan

You know that they will deduct the dividends already paid from the investment when liquidating. 🙂

As a benchmark, VNQ is up about 6.9% in the same period.

thanks for the update, it is quite useful. as a result i became quite curious and opened a Fundrise account

I moved some REIT funds into the Growth REIT at Fundrise last August. This fund has a focus on appreciation rather than income generation. My annualized return is about 5.8%. I enjoy the specific updates about property deals, renovations, etc. They are responsive to my questions. The liquidity issue isn’t very important to me. So far I like the platform and I like being connected to my investment, even if it is difficult to compare the value of this approach.

This last quarter I setup DRIP. They ended up putting my growth dividend into the three new funds. I can’t say that is how I would have preferred to structure reinvestment, but oh well. It isn’t terribly important.

Fundrise recently offered shares of itself through it’s platform. I planned to add to the platform through that vehicle, but I missed the boat. The offering closed in a few hours due to demand. I will probably just skip additional contributions now. I am curious to see how far this platform goes, I believe they intend on pushing the concept well beyond the REIT space.

LOVE IT

I have been using Fundrise for almost 2 years now and have gotten approximately 10% returns consistently. I would love to hear the experiences from other users, but I have nothing bad to say about it. It is so simple, put money in and grow your account…..I honestly didn’t think it could be real…..I thought it was some kind of electronic ponzi scheme so at the beginning I was careful and tested it, but the SEC is on every move that they make and its all backed up by real properties and not strip malls or heavy retail that could be killed by Amazon. These are senior facilities, apartment buildings, condos, townhomes and hotels…places designed to generate revenue.I have nothing negative to say about this company……and have yet to find someone that has has a bad experience.

Hi, I did leave those reviews on multiple sites because I was hoping people would post their own experiences….there just aren’t that many reviews of it online and I am honestly trying to find someone who has had a bad experience with it…so yes, I posted it on 3 review sites hoping to hear from other people, but beside being an investor I have no affiliation with the site. I am just honestly concerned about the money I have invested and looking for red flags myself…..so far so good though.

Thanks, Justin. Not trying to slam you or anything. Just doing due diligence before I send them a bunch of money. I appreciate your comments.

I think the author and the people commenting should be a bit more cautious about Fundrise. There are a few terms in their subscription documents that are discomforting:

1- If you want to redeem within the first 5 years you will have to pay penalties. Around 10% if within first two years if I recall

2- The NAV question is very important since it seems the NAV of their funs decline in line with their distributions. There is a dangerous clause in their documents that allows Fundrise to distribute dividends to investors from the fund’s pool of investable money. Basically, taking investors’ money to distribute to other investors. If this is being practiced, then all investors could be in for a very shocking surprise!

3- Lack of transparency: Although they are quite good at communicating and replying. They have been very vague when I’ve asked them to report the source of their dividend distributions as well as further explain why the NAV is in decline while investors are already getting 5%-10% distributions.

Any thoughts and comments on my concerns above are very welcome.

Here are additional details on the quarterly liquidity. The penalty on withdrawals within 5 years varies from 1% to 3% of NAV. This is not meant as a short-term investment.

https://www.mymoneyblog.com/fundrise-ereit-liquidity-redemption-process.html

Meh. One of my own investments (not with Fundrise) has tied up money for 15 years. As in no early withdrawal penalty; rather, no early withdrawal possibility. It’s no big deal; there’s no reason why a financially responsible adult should need 100% of his investments to be liquid.

I’m just starting to look into Fundrise as an investment opportunity. It may be an unfounded concern, but Justin Cox’s evaluation above is word for word the same one he left at another review site. It is also nearly exactly the same as a third review site. Is this an employee leaving the same reviews? If so, red flags should go up.

RH raises some good points. Here are some additional cautions from https://www.fool.com/investing/2016/06/23/is-fundrise-as-good-as-it-seems.aspx

“All funds carry fees, but Fundrise’s fees appear particularly conflicting.

At virtually every step along the way, the fund’s managers will seemingly collect another fee from investors. When the fund managers find a deal to invest in, they carve out an origination fee of up to 3%. The company’s filings state simply that “we will not be entitled to this fee,” referring to the investors in the fund. Management thus has an incentive to offer loans with higher origination fees (which flow to management), offset by lower interest rates (which would result in less income for fund investors).

Likewise, managers collect ongoing management fees equal to 1% of the funds’ net asset value on an annual basis, in addition to servicing and property management fees, which can add up to 0.50% of assets.

But that’s not all. Fund management also stands to collect every time Fundrise sells a property on behalf of its investors, collecting 0.50% of the gross proceeds after repayment of property-level debt. Notice that this fee rewards management for activity, not investment returns. Buying and selling a property at a loss would theoretically generate earnings for fund managers at the expense of capital losses for its investors.

Perhaps worst of all, there are higher fees charged to the eREIT when management makes an underwriting error. Tucked away on page 16 of a regulatory filing is the notice that a special servicing fee is assessed on non-performing investments at a rate of 2% of the asset’s value annually. It goes on to warn that “whether an asset is deemed to be non-performing is in the sole discretion of our Manager.” “

What makes me suspicious is the allure of returns in the 10 – 12% range. Risk vs. return is like the law of gravity: immutable. A ten-year treasury paying 2.5% comes with almost no risk. A company’s stock paying a 4% dividend comes with some risk. Junk bonds paying 7% come with a ton of risk. The Saudi government said it would seek returns for its sovereign wealth fund of 9% — a lofty goal. I don’t know of any asset class that can offer consistent 10-12% returns without enormous risk. If someone can explain how Fundrise has repealed the principle of Risk vs. Return I’d love to hear it.

Tom,

I have some of the same concerns. In looking more closely at their estimated breakdown of the returns, they state that the annual dividend is 5-6% and the increase in “share” price should average 5%/year. I think that’s where the 10-12% comes in. I spoke with one of their representatives at length (Maddie), who spent a total of about an hour on the phone with me over 4 calls. She was very careful to keep reminding me that there is no guaranteed ROI. But with the breakdown between dividend and share price increase, combined with a bit of luck that the real estate in which they invest doesn’t tank, 10% sounds possible. She said they carefully vet their investments and try to balance them between rent-producing (like senior apartments) and value appreciation properties that they intend to re-sell. Keep in mind, too, that they charge 1%/year for a “management fee.” That does take the 10% down to 9.

With all those caveats, I have gone ahead and am trying an investment with them in their Long-Term Growth fund. I’ll try to remember to update this site as I see what kind of returns I see…or don’t.

Because, according to their prospectus, they can use other investors’ money to pay you your dividends! I have received approx 9% annual distributions. Instead of making me happy, it’s made me very concerned. I don’t know if any real estate investment that can simply churn out 9% NET within a year of investing in it. Something fishy is going on there. Don’t but any substantial amount of your savings in there! I won’t trust these numbers until they provide viable explanations as to the source of their distributions.

Well, to give you guys an update….I am coming up on my 2 year anniversary with the platform. I have about $23k invested into it and receive a quarterly dividend between $549-$597. Instead of re-investing this as there is an option to do, I instead put this into a savings account. Over the life of my investment I have generated an exact return of $3,510.12

So far so good….

So about 7.5%/yr or so averaged out. Hopefully, they’ll sustain it and it won’t end up with references to Bernie Madoff. I put in $25k this week to see what happens. I’ll try to keep my returns updated here.

I’d read someplace, wish I could remember where but of course I can’t, that Fundrise’s returns stemmed from lending to less than creditworthy borrowers. If you think about, junk bond issuers pay higher rates to compensate lenders for the higher risk. Right now Fundrise returns are coming in above junk bond returns. Something doesn’t add up. Fixed income investors across the spectrum have been sifting like gold panners, looking for nuggets of decent returns balanced with liquidity and risk. It’s hard to imagine that Fundrise lies there like the unseen nugget in the pan, overlooked by millions of return-hungry investors. It’s almost like the old saw: if something’s too good to be true, it probably is. I have money invested in Fundrise that I can afford to lose. And that’s it.

I think it’s rather that they’re lending for projects that wouldn’t qualify for, say, a bank loan because of the nature of the project (not because the borrower has bad credit). And it’s not all about lending; some of Fundrise’s investments are equity investments. An apartment building that hasn’t been built yet isn’t worth nearly as much as one that has tenants; increasing the non-existent building’s value after expenses by 40% in 5 years would, of course, translate into the ability to pay out 8% per year.

If the projects were larger, then they would be of interest to the big REITs.

I have also invested with Emerging Trends RE Corp, which is currently specializing in deals with Thailand-based New Nordic. Essentially, that’s a play on the expansion of Chinese tourism to Thailand. I first learned about Emerging Trends RE Corp because I already owned a New Nordic apartment.

Hi mdduff,

Just curious to see how your $25K has fared since Oct? Thanks for posting.

I ended up putting in another $50k in January after I ensured that the quarterly dividend paid out. To date, I have had 2.3% total return as dividend. Not bad for 9 months. This does not include any increase in the actual “stock” value. I don’t know how often that gets adjusted. I have also enrolled in the automatic reinvestment program, so the dividends roll into my principal quarterly. So if it stays on track through the end of the year, I’ll make about 4% in dividends. Not terrible, but not a get rich quick scheme. I have found their customer service to be excellent – they have gotten back to me quickly to answer questions.

The only reason you made only 4 percent is you put the money in to late.

That is what happened to me when I first put it in

Now I am getting about 8 percent

One fund is all return of capital which I dont like

A reply to Ralphpal from above: OK, to be completely accurate, I invested $25k in late October, and then $50k more in January. The total return on all that has been 2.3% over the past approx 9 months. If you count in that there were 3 months with only $25k, the return is maybe 3-4% from October to October. I’d love to see 8%, but it’s not on target for that for this investment year unless they up the dividend.

Good reply. Can i please get the same type of update from you with all the informstion you included updated to todays date?

Hey guys, as requested here is an update….with my initial investment of $23k now in my 3rd year i have so far generated $4,846.83 over the life of the investment.

Dividends fluctuated a little…..here are all my dividends to date.

4/12/16 $48.33

7/13/17 – $561.67

10/9/17 – $596.73

1/9/18 – $570.40

4/11/18 – $405.34

7/11/18 – $449.71

There was certainly a dip starting after the first of the year, but I will see where it goes from here I am in it for the long haul.

(Edited to remove referral links. Thanks.)

I put In 1000 dollars in 6 different instances

This was actually before everything became an REIT

You actually was able to just invest in one building

So after 4 years on 6000 dollars I am receiving

114 dollars every quarter

now, just to put this in perspective, you could spend 6700 dollars on 100 shares of ABBVIE and get roughly that, each quarter, but the problem of course is that when I bought in, ABBVIE was around 90 a share. So let’s not imagine that equities and stable dividend payers can’t give you the same rough ride that real estate can!

Great article Johnathon

Hello to all you fundrise veterans out there, did anyone run the numbers to determine how much tax benefits you would get by using a self directed IRA? I noticed on the site they are promoting a partnership with Millennium

https://fundrise.com/mtc

http://www.mtrustcompany.com/individuals

here’s their fee schedule

http://www.mtrustcompany.com/sites/default/files/forms/static/Self_Directed_IRA_Fee_Schedule.pdf?access=1517621854

the way I understand it, if I invest in their balanced portfolio, I would charged $200 for all the eREITs

so fee breakdown using Millennium would be something like

$350 first year (incl $50 account setup)

2nd year and onward would be $300 annually if they don’t increase their fees

when investing outside of an IRA I understand that all dividend from fundrise are taxed at your income tax bracket, that that also hold true for redemption?

thanks

Well I have in the growth and income

4 thousand in one of them

2 thousand in the other

the dividends went down 20 percent in the last quarter , I guess that was because the interest rates increase

Also one of the funds the dividends was non qualified dividends which you will expect from a REIT like fundrive

the other one either growth or income fund

the dividends was return of capital

I am not sure if that is good or not

I know you don’t have to pay taxes on ROC

but am I just getting my money back or was this a fancy accounting that let me get dividends but not pay taxes on them

Update: Just got my quarterly dividend for the Fundrise Long-Term Growth plan. Approx 1.1% for the quarter. If it keeps that rate, it’ll be about 4.5% for the year. Not bad. It is supposed to be more oriented to the long haul. Automatic reinvestment is activated. And remember there is a 1% annual fee. So return will be more like 3.5%.

Thinking of opening an income account to see how that fares.

Hey Mdduff, I would also look at the appreciation of your initial investment I saw that I also received 1.1% dividend but my appreciation was up about 1.5% which would equate to about 10.4% return (I also DRIP because why not?)

Hi mdduff, would you mind giving another update on how things are going for you? I actually signed up in July 2018 so right around the time of your last update. I also went for the Long-Term Growth plan and haven’t seen a lot of growth yet (though it is a little hard to calculate the exact return to date since I have made several recurring investments rather than one lump sum).

Thanks!

Conor,

Sounds as if you are having some of the same questions I have. on 1/1/18, I had $25,189 in the fund. I added $25k Jan 19 and $25k on Mar 7. On Mar 7, I had $75,389 in. It makes the math a bit tough, because of the staggered additions, but overall, I ended 2018 with $80,730. That gives me a return of $5341 over the last 75% of the year. Or about 6.6% return for that 9 month period. If the current % holds, it would be about 8.3% for 2019. (I do the DRIP, btw).

What I can’t figure out is how they are going to revalue the actual shares to reflect the increasing value that Fundrise says I’ll be able to capitalize on far down the road (the equivalent of the share price). I haven’t seen a revaluation anywhere on the website. 8.3% isn’t bad at all (again, minus the 1% fee, it still isn’t bad at 7.3% – certainly better than my 2.3% savings account), but I’d like to know if I can get another couple of percent per year out of this. Then it would be a truly great investment.

Of course, all of this is dependent on my being able to actually get the money back from them someday. Because I’m in it for the long haul, I haven’t tried to withdraw funds.

mdduff

One more quick note: I just noticed that the Fundrise website now breaks down my earnings into Dividends and Appreciation. It shows 2019 YTD and “all time” columns. According to that, the gains I have made are approximately 60% dividends and 40% appreciation. That puts my projected dividend gain for 2019 at about 5%, and the appreciation at 3.3%. IF, IF, IF it continues at the same rate. I’d be excited to get an 8.3% return!