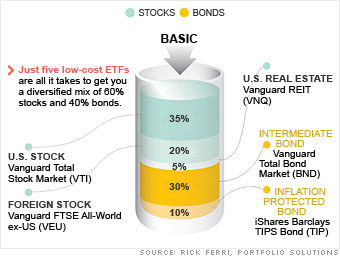

In a recent Money magazine article about ETF Investing, there is a nice illustration of a simple and diversified portfolio made entirely of ETFs by author/money manager Rick Ferri:

Put simply, ETFs are essentially mutual funds that trade like stocks. (Note the ticker symbols included above.) Hence the name Exchange Traded Funds! You tend to get lower annual expense ratios than mutual funds, but you must also pay a stock commission on each and every trade. They also tend be better in taxable accounts because they often don’t shed as many capital gains. Since there are now a million types of ETFs out there, it’s good to remind everyone about the great portfolio building blocks out there.

If you trade large amounts at a time or have cheap enough trades, then ETFs can be a good option. Otherwise, even $10 a trade can really add up. If you have $25,000 of total stock value, you can move your account to Zecco Trading for 10 free trades per month, or to WellsTrade (by Wells Fargo) for 100 free trades per year (special PMA checking account required).

Done this way, the total cost of this portfolio would be under $20 a year for every $10,000 invested. Less money in a broker’s or manager’s pocket means more for you.

* Update: Here are 8 more model portfolios that you can replicate with ETFs these days.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I have never had any luck with bond funds,I avoid them like the plague.

“I have never had any luck with bond funds,I avoid them like the plague.” probably because there value changes with interest rates so it looks like you’re losing money when you’re not.

What you forgot about is that the spreads on Wellstrade and Zecco more than make up for the trade being “free”

Charles Schwab has the best NASDAQ spread and Scottrade has the best NYSE spread. When you are trading $25,000 or $50k worth of stock (what is needed to get free trades. The cost per trade is going to be $40-$120 more than with a firm with a narrow spread and $7-$10 trades.

I can’t find the article again though because google search results are increasingly filled with spam links. If you like low fees and basic service scottrade is the best. If you like more service and account features, Charles Schwab has low fees but offers more. I am currently switching over to Schwab from Scottrade because of their 2% cashback (end of every month no minimum redemption amount) and checking account (monthly refund of atm fees, no forex fee, and it is interest bearing.

ETF’s are fairly new to me but my understanding is that positions are automatically traded electronically based on a price. This is similar to putting strict preservative stop loss orders on all your individual stocks in your portfolio of stocks. Agressive market fluctuations with no direct impact on an individual stock position would force the ETF to unload the position. The problem comes with high volume days and volatility in the market which could disturb the long-term allocation of an ETF. I personally would only use leveraged ETFs for short-term swing trading.

Take my analysis with a grain of salt and I could have the wrong impression of ETFs. I do have a position in DVY etf.

Agreed on the ETFs, but why sit there and take the pain in down markets? An excellent book hear by Meb Faber about 1) being well diversified thruogh ETFs (like above) and 2) getting out when a class is trading below the 200-day moving average.

http://www.theivyportfolio.com/

Even Mark Cuban is saying Buy and Hold is dead:

http://blogmaverick.com/2009/06/19/2-quick-hits-on-sports-media-and-the-stock-market/

30% in bonds and 10% in TIPS?

That is pretty conservative.

NY GUY:

I mean this unsarcastically — keep learning. Your understanding of ETFs is not quite right. ETF shares are created and destroyed as stock, so no buying or selling of stock takes place within the ETF. This makes ETFs very efficient. What happens is that a large institutional broker may buy enough stocks to create an ETF “creation unit” (a creation unit is just a specific large number of shares). This buying happens outside the ETF, so it doesn’t matter to you. Then they convert it into ETF shares. They’ll do this if the bid/ask spread is in their favor to do this. They’ll do the opposite if the market is pricing the ETF lower than the individual stocks. This keeps the ETF value fair, and provides liquidity, and keeps management costs of the ETF down.

yeah 40% bond is a little too conservative for me, well it really depends on your age and when you plan to retire.

also if I may add, I would also get some commodities ETFs such as gold, metals, oil etc to get a more balance portfolio. might also want to throw in Asian, South American etc ETF to capture their growth too.

If you treat this as long term investment and not trade frequenty, the cost impact is pretty low.

Dear Chuck and NY Guy,

If possible, would you continue the discussion about the mechanics of ETFs? Not the investing rationale but actual ownership issues, asset protection, and liquidation issues. The issues which are the inherent risk factors in the type of structure the ETF uses, not the market risks, except as they cause the systemic type of risk issues to develop.

Just cannot get my brain around the structure and the worst-case scenario possibilities

Tommy: I’ve had quite the opposite experience with them (not that 2 anecdotes have any value) — I’ve owned some shared of BND for a couple years now, and they’ve been the most stable shares I’ve owned. Pays dividends monthly like clockwork. BWX (an international bond fund) was similar, but recently they ditched the monthly dividends as far as I can tell. Both have actually posted gains against when I bought them; none of my other stock can say that at the moment 😉

I agree with cs — 40%’s a bit conservative. real estate seems a bit under represented (I usually see 10-15%).

I personally think it makes a lot of sense to create a properly asset allocated portfolio using ETF’s. My own portfolio is based primarily on index’s although I have a more aggresive asset allocation as a larger portion in small caps (VB) and a commodity index (DJP) to enhance the portfolio and create more diversification using another asset class. I have created a portfolio as such and put it up to some fairly aggressive active managed funds and so far the properly asset allocated fund is outpacing the active funds and that is strictly on a performance basis not including expense ratio’s and fees.

I do not hold any bonds or bond funds in my portfolio simply due to age and risk tolerance although I have heard of some people setting up a 50/50 portfolio and doing nicely.

So what is the best way to implement this in my life? Probably not my work’s retirement plan (lack of control over commission per trade?), maybe a 529 plan (can that be done through Zecco for free trades?), or I guess I give up on trying to buy individual stocks and buy ETFs instead.

I have a pension plan, a 457 retirement plan, and some individual stocks. I need to start a 529 plan for my kids. I am unclear as to where I could fit in investing in ETFs.

Also, the article contained this line: “You pay a commission on each trade, so ETFs aren’t an ideal place to sock away small amounts of money each month. But they’re perfect if you’re investing a lump sum, such as an inheritance or a 401(k) rollover.” So it is feasible to sock away small amounts with Zecco free trades, but how long before they stop offering free trades (or raise the minimum account amount), and what do you do then?

But you are losing on bond funds – especially if you have to sell them. This buy and hold strategy simply does not work anymore. Why do you think that Fast Money show is so popular?

ETF Mechanics

Liquidity depends on the ETF and index it is tracking. The QQQQ’s or VTI have a lot of liquidity. There are so many ways to slice and dice and create an index say the Pallisides Water Index (PHO), there will be less liquidity with the more obscure ETF’s then the larger overall market ETF’s but still are pretty liquid unless you are an institutional investor. Some of these ETF’s get so specific that it is more risk because you are betting on a specific industry such as CUT,SEA etc.

Also be careful for 3X ETF’s such as FAZ or FAS (Financial firms)which are supposed to offer 3X the returns either shorting or long.

I mentioned earlier DJP which is actually an ETN (Exhange traded note) there is a credit risk associted with ETN’s as they are backed by the firm offering so if you bought an ETN backed by a bank you felt could go under then you would be in line with all the other creditors. DJP is currently backed by Barclays bank & would imagine still will be even though Blackrock has purchased the iShares business from Barclays.

MS the only other issue I would say the big difference between buying the ETF as opposed to the Index fund at say Vanguard is you cannot automatically reinvest dividends, it would be a trade then.

I personally like the flebility the ETF’s offer with trading during the day I can be more precise for which price I pay for an index rather then thru a fund purchase which if it is a big percentage moving day it could cost. Hope this helps.

Can anyone else verify what Michael said about Wells Fargo and Scottrade really being the cheapest brockers when dealing with large orders because of market spread advantage. I never heard this before, but if true, I can see how it would make sense.

Rick, WellsTrade is one of the bad one’s. You mean Scottrade and Charles Schwab.

This is from 2006 so it is a bit out dated (I don’t think this is the same article that I originally saw, but it has the same result so w/e):

http://www.businessweek.com/magazine/content/06_31/b3995118.htm?chan=investing_spr_tools

@Christopher Wright: I also had a bit of BND and I saw the dividents coming at approx. 4% rate. It beats many savings accounts in this economy.

I am looking for a portfolio mixture (i.e. asset allocation) that is both rock stable and a better than savings accounts rate in this bear market.

Does any one have some more info to share?

I personally have been burned on bond funds.They are not bonds and they don’t in anyway mimic the way a bond behaves.They can’t give you a fixed yield and you can lose a lot of your principal,so I stay away from them.I am sure they work for some people but not for me.I think they are a garbage investment.Buying a bond means something it is a contract to pay you a certain amount of money a bond fund is no better and probably worse then a stock fund.

Bond funds protect you from the credit risk associated with buying single bonds. If you have one bond and it defaults, you just lost all your principal. If you own parts of 1,000 and one defaults, you would barely notice.

Just like single bonds, the market price of your bond fund will fluctuate due to interest rate changes of the market. Matching maturities exactly is more important if you are trying to match cashflows, not as much if you are maintaining a long-term portfolio, where maturities still help in bond funds to determine how volatile your values will be.

If I was going to buy bonds, I would always buy them through a fund unless they are Treasury bonds which have as close to no default risk as possible.

To add to what Jonathan just mentioned: buying individual bonds also means your risk profile (mainly bond duration, also the gamma and vega value of your portfolio, for you finance guys) will alter everyday unless you have a huge person bond portfolio and it is balanced constantly. Your bonds portfolio will be more or less sensitive to interest rate changes, based on its duration (ie, in simplest terms, short-term vs long-term bonds). It’s pretty tough for any individual to track and maintain bond portfolio durations, unless you only have a few bonds (then you are missing out on the only free lunch: diversification). Bond funds’ duration usually stay fairly consistent.

My problem with bond funds is that people think of them as a fixed income investment and they are anything but that.When you buy a bond fund their is no fixed income or any obligation to pay you anything.As for diversfication in a bond fund,How is a person to know what a fund manager is doing with a bond fund?maybe your risk is being raised every day,you can’t know.If you own a bond ,even just one bond, you can know its risk level and their are numerous ways to deal with that risk.I guess my real problem with bond funds are that their name implies something that they are not.

Are ETF’s really better than Vanguard? Just want to make sure before I make the big plunge. 🙂

2 things:

1. Don’t use Zecco if u intend on having a margin account.

2. Wells Fargo short term muni fund. VERY stable share price & pays more than taxable funds!

“Are ETF’s really better than Vanguard? Just want to make sure before I make the big plunge.”

ETFs are better for financial advisors because they can charge 1% management fee instead of simply taking the .2% commission for selling vanguard funds. Brokers like it because it generates more trading fees for them. ETFs are more hype than anything else, a lot of their supposed “benefits” are exactly the same as the benefits of index mutual funds. Publishers/Content providers (CNBC,blogs,etc) promote them because ETF funds are willing to pay to sponsor reports on ETFs and buy ad time to promote them with a portion of the extra fees(If you don’t believe me count the number of ETFs vs Mutual Fund ads you see when you watch TV or go to financial websites and check out the ads). ETFs also make stock exchanges more money too and market makers get another asset to collect spreads on.

The only real advantage for consumers that buy ETFs is that there is more variety and that you can buy and sell them at all times of the day.

Vanguard ETFs vs Mutual Funds Calculator:

https://personal.vanguard.com/us/faces/JSP/Funds/Tools/FundsToolsEtfCostPurchInfoContent.jsp

The difference between the two ranges from negligible to favors mutual funds. .03 spread will be most certainly be higher if you use a $0 trade broker as I pointed out above

Don’t get me wrong I don’t think ETFs are bad. I am not some fringe conspiracy theorist, but at the same time seeing the same inaccurate and shameless pro-ETF BS time and again gets annoying. It is more annoying when people start to buy into it.

I’ve thought about buying a bond ETF before, but only because I already have a brokerage account. If you already have a Vanguard account I would keep it, unless you have an actual complaint such as a lack of diversity.

“Tax Tales

You hear a lot about tax advantages with ETFs. Treat it like barroom gossip: exciting to hear, but probably an exaggeration.”

“#I n general, the structure of ETFs tends to avoid the kind of outright selling that would trigger undistributed capital gains and other IRS nightmares. To understand why, think back to the ETF structure. For every ETF seller, there’s a buyer.

# On the other hand, if a flood of investors decide to dump a mutual fund, the fund may need to sell the underlying holdings in order to raise the cash to pay out, and that would bring Uncle Sam with hat in hand. ETFs may also have to drop a few schillings into the taxman’s cap, for instance, when the underlying index is changed.

# Keep in mind that the traditional fund industry and the ETF industry disagree on the extent of the ETF’s advantage. Of course, they’re competing for your investment dollar, so you should expect squabbles. Still, according to published reports, the Barclays iShares S&P 500 ETF made capital gains distributions while the Vanguard 500 mutual fund did not..”

–http://www.fool.com/etf/etf02.htm

FWIW, I currently invest primarily with Vanguard mutual funds directly at Vanguard, because they provide all the asset classes I need at a low reasonable price.

However, if my taxable holdings got large, I would consider moving to ETFs for the price advantage. On top of lower expense ratios, I get annoyed at some of the purchase and redemption fees of some Vanguard mutual funds (i.e. Emerging Markets, FTSE All World ex-US.) which don’t apply to their ETF equivalents.

Yeah, it’s crazy but it is more expensive to buy Vanguard ETFs through Vanguard than if you were to buy them through say Schwab…

One problem I’m running into with Vanguard right now is my accounts there are a complete mess and hard to keep track of. If you have an IRA there for example, and you want to trade ETFs, AND buy index funds as well, you have to have TWO different accounts. I have the following accounts at Vanguard: SEP-IRA, traditional IRA, non-deductible IRA (to be rolled over in 2010) a ROTH IRA and a taxable account. Now multiply all these x 2 accounts (One for buying funds, and the other a VBS account for buying stocks) and I have 10 different accounts at Vanguard. It makes asset allocation a nightmare!

I’m honestly considering switching to Schwab as I can buy Vanguard ETFs there anyway.

I have for years told people the only place to go if they wanted to invest was Vanguard. Alas, they are making it difficult for me to still make that recommendation. (Although they do still have the best funds…)

Vanguard needs to have a commodity fund, I know they have the precious metals and the energy fund but it would be nice if they had a fund tracking the Dow Jones Commodity Index.

I don’t think Vanguard has a micro-cap fund either although I do think you would have advantages of an active manager in that universe over using just an index. I know a lot of advisers feel even in the small cap world that active is better then passive, I personally don’t agree.

I use Bank of America’s free trades to invest in ETFs. I chose to go with ETFs over equivalent mutual funds in order to get diversification that is affordable. Most mutual funds have minimum initial investments of $2k+, as a beginning investor I’m not in a position to do that with 10 funds. With ETFs its not a problem.

Maury, I’m curious, if you have an account at Vanguard, why would you want to buy Vanguard ETFs as opposed to their funds? You have to pay commissions on each time you trade the ETF.

Vanguard requires a separate account since you are trading the Vanguard ETFs on the open market. You can buy/sell any other stock with that account as well, so I understand why they would separate it. It’s unfortunate thought that they don’t provide you with a service that shows your combined assets to assist you with asset allocation.

Bill,

A good part of the reason Vanguard doesn’t have a micro-cap fund is that it would just be too large to run effectively. The closest thing to a truly decent micro-cap fund was the DFA small company index which tracked the 9th and 10th deciles of the market. I think the minimum on that was $1 million and even then I believe you could only get it through DFA registered advisors. A lot of institutions used that for their exposure.

The micro-cap ETFs are all garbage. They are hugely overweighted to financials and most of the stocks overlap with the bottom half of the Russell 2000 anyway… I remember reading that something like 70% of the Russell Micro-cap indexes weight overlapped with the Russell 2000 index.

A good micro-cap “index like” fund is Bridgeway. It is something both Jonathan and I own and gives you good exposure to the smallest stocks. Royce has some decent funds as well.

Full disclosure, my job is raising money for institutional micro-cap managers. You can rest assured the institutions run into the same problem you face. It’s nearly impossible to find a good micro-cap manager who isn’t closed, (or who should be!) Many of the institutions don’t bother with the asset class because there is too much effort involved for the quantities of money they can invest. It is one area though where the returns have historically been appealing. Especially coming out of recessions.