| Retirement Portfolio | Actual | Target |

| Asset Class / Fund | % | % |

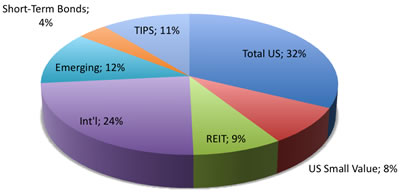

| Broad US Stock Market | 32.2% | 34% |

| VTSMX – Vanguard Total Stock Market Index Fund | ||

| DISFX – Diversified Stock Index Institutional Fund* | ||

| FSEMX – Fidelity Spartan Extended Market Index Fund* | ||

| US Small-Cap Value | 8.7% | 8.9% |

| VISVX – Vanguard Small Cap Value Index Fund | ||

| Real Estate (REITs) | 8.7% | 8.5% |

| VGSIX – Vanguard REIT Index Fund | ||

| Broad International Developed | 23.8% | 25.5% |

| FSIIX – Fidelity Spartan International Index Fund* | ||

| International Emerging Markets | 12.1% | 8.5% |

| VEIEX – Vanguard Emerging Markets Stock Index Fund | ||

| Bonds – Short-Term | 3.7% | 3.8% |

| VFISX – Vanguard Short-Term Treasury Fund | ||

| Bonds – Inflation-Indexed | 10.8% | 11.3% |

| VIPSX – Vanguard Inflation-Protected Securities Fund | ||

| Total Portfolio Value | $120,016 | |

| * denotes 401(k) holding given limited investment options. |

2009 is already over one-fourth over, so I think it’s a good time to check on the ole’ battered portfolio.

Contribution Details

In early 2009, we each made a $5,000 contribution towards our non-deductible IRAs for the 2008 tax year, for a total of $10,000. We have also contributed $12,969 so far into our 401ks through regular salary deferrals and the company match. We haven’t made any after-tax investments in our portfolio yet.

YTD Performance

According to my spreadsheet, the 2009 year-to-date time-weighted performance of our personal portfolio is -15.5% YTD.

For reference, the Vanguard S&P 500 Fund has returned -6% YTD, their FTSE All World Ex-US fund has returned –6.36% YTD, and their Total Bond Index fund is -0.13% YTD as of 12/8/08. The Vanguard Target 2045 Fund has returned -4.70% YTD. Part of the poor relative performance is probably due to the timing of my large lump-sum investments.

Investment Changes

We have used our new contributions to bring us closer to our asset allocation target, with a 85% stocks/15% bonds split.

You can view all my previous portfolio snapshots here.

The Best Credit Card Bonus Offers – May 2024

The Best Credit Card Bonus Offers – May 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - May 2024

Best Interest Rates on Cash - May 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Any thoughts on adding the new Vanguard International Small-Cap fund? I’ve been looking for a way to add one more piece to the pie, and developed international small-cap might be a good choice. I’m guessing your exposure to this asset class is next to nothing in FSIIX…

http://ca.news.finance.yahoo.com/s/06042009/34/biz-f-business-wire-new-vanguard-international-small-cap-etf-begins-trading.html

I like the portfolio in general, but why the fractional percent precision for your target allocations? It seems like there wouldn’t be much difference of 8.9% vs 9 (even 10) percent, but you chose it anyway.

I’m just wondering what the reasoning was. Does another $120 in US Small Value make that big a difference in your portfolio long term?

Why not just “34 + 9 + 9 + 25 + 8 + 4 + 11” or even something like “35 + 10 + 5 + 25 + 5 + 10”?

@Robert: I think he’s using the two % system, a whole number % of total is in stocks and others in bonds, and a whole % of those in stocks is in this asset class, for example.

With a little calculation here’s Jonathan’s allocation

15% bond – of which 75% TIPS, 25% short term

85% stocks – of which 40% Broad US, 30% int Developed, 10.5% US small cap, 10% REIT 10% emerging

I know there’s extra .5% in US small cap, but if you add up Jonathan’s portfolio %, you will get 100.5%

Why are you investing in bonds when you still have a mortgage? It doesn’t make sense to borrow money on your house at 5% only to invest it in 2% bonds. Paying off the mortgage will provide a better return and reduces your financial risk even more than government bonds.

I’m all for a blanced portfolio of stocks and bonds, but only after debt is paid off. Until then it should be 100% stocks + aggressive mortgage paydown. Am I wrong?

Maury – I think the new International Small Cap fund is a nice addition, but I don’t know if the added complexity will be worth it. Sometimes I think I’m making it too complicated as it is.

Robert – As Jim noted, it’s just a result pulled off from my Excel spreadsheet. I don’t really aim to hit it square, it would be too difficult with all our different account types anyhow.

Matt – Interesting question. I’ll explore more later, but paying down a mortgage to me is like a 30-year Treasury note. There are issues of matching desired maturities, risk, liquidity, tax-deferral, etc. You may be right, if that’s what you want.

Jonathan,

I agree with Maury, you ought to consider adding Small-Cap Int’l to your mix. As an asset class it has historically been less correlated with the overall U.S markets and, as with U.S Small-Caps vs. Large U.S, is likely to have a higher return over time than the developed markets. Moreover, the new Vanguard Small-cap Int’l fund also includes emerging markets exposure too.

The rest of the portfolio looks good. You could add Int’l REITS or a Commodity fund at some point to round out the full diversification.

One reason to not pay down a mortgage is liquidity… Any money you put into your house you can’t get to until you sell it.

If Jonathan were to lose his job, (Don’t worry Jonathan, just hypothetical…) he would likely not be able to get a home equity loan, and he would only have what liquid cash he has on hand to make house payments/meet needs.

Any extra money he had put in his house is stuck there. (Ironically, a lot of people put extra payments towards their house and end up losing it because of a cash crunch and not being able to make future payments if they lose their job.)

That said, if those bonds are in retirement accounts (which they probably are because TIPS are horrible to own outside of retirement accounts…) than what you said makes a bit more sense as the time frame for selling the house is likely sooner than that of retiring.

What your opinion on balancing your portfolio across different accounts? Example, I have about half my investments in a my 401K and the other half in Roth IRA and other.

When you look at asset allocation do you look at the whole thing as a group or each ‘account’ separately. Its hard to keep both ‘accounts’ balanced without using lots of funds in each.

Jonathan,

In your brokerage account, why are you using mutual funds and not their ETF equivalents? Even though Vanguard Funds are no load, my broker (Schwab) still takes 5% sales commission which is huge compare to the $12.90 they charge for ETF transaction.

@Tyler, I look at the whole thing a group, so my 401k might be all international funds, while my wife’s might be all US index funds. However, we do make sacrifices to keep simplicity and costs down.

@Motti – You are getting charged a 5% commision for Vanguard funds? Why, are you in a managed account? I just hold mine at Vanguard.com, and have never paid a transaction fee… ever.

I think you have way too much TIPS. I think so partly because I believe inflation will stay low despite what the hyperinflation Armageddon “analysts” are saying. And even if inflation does pick up, TIPS don’t give you much of a hedge. Instead I’d go for a world basic materials fund (an ETF or index fund). The dividend yield on funds like DBN is over 5%, and plus, you have much better capital appreciation potential (and much more downside risk yes). You can also consider emerging market debt (EMB for example) if basic materials equity is too risky since emerging economies’ credit ratings (and hence bond prices) will rise with higher commodity prices. Russia, Venezuela, South Africa are top holdings in EMB for example.

Something else I need to mention. The MSCI Emerging Markets index which is benchmarked by most emerging markets funds do not include much of China. Taiwan yes, but mainland no. I would dedicate at least 5% of your portfolio to pure-play China stocks since China will be the big growth story for the next 10 years or so. FXI is OK but it has way too much state-owned megabanks. I’d go for PGJ or HAO.

I’m curious why you’re targeting 8.5% of your portfolio in an REIT since you have so much net worth already tied up in your home (or visa versa).

Are you concerned that fluctuations in the national real-estate market won’t be reflected in your own home’s value? I realize that the fund you’re investing in is more closely tied to corporate real-estate values, but there is still a strong correlation to residential prices.

http://tinyurl.com/y8h9wn6 (Home builders index etf vs your own over the past 2 years)

I suggest moving a large chunk of that 8.5% in to a corporate bond fund. This way you’ll still be in a more conservative asset class, but less tied up in real-estate values (see LQD or even JNK).

where’s the most recent quarter?

hey john,

what brokerage are you using, and which brokerages have the best spiffs right now for new retirement accounts? thanks.

mike

Not a bad allocation, but why so much in TIPS? It would seem more prudent to perhaps hold both BND and VIPSX. (though this would add yet another fund)

I also would be curious to know which holdings are in your Roth vs Taxable accounts.

Keep up the great work!