A financial topic that nearly everyone has an opinion on is car ownership. Do you buy new and drive it into the ground? Do you buy slightly used after the early depreciation hit? Do you buy a cheaper 10-year-old car, drive it for a while, sell it for not much less, and repeat?

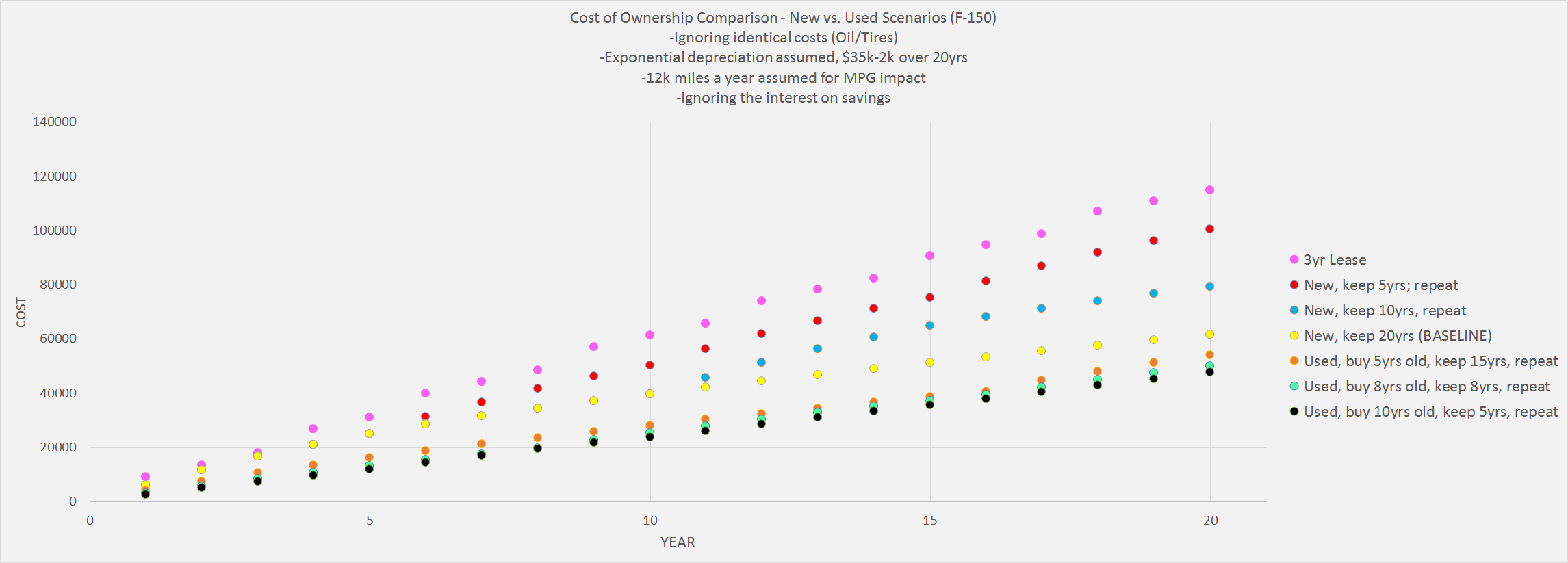

Reddit user nmtxinsc2 put together an interesting car cost comparison of the total cost of ownership for these options and more. Here is the final graphic, which you should click to enlarge:

Assumptions. These are not based on average or historical car values, but from a theoretical cost model for a single car. A quick overview:

- Car Value. New price $32,000. Value depreciates exponentially down to $2,000 after 20 year lifespan. The historical depreciation behavior of a Ford F-150 is a general benchmark.

- Maintenance. From $0 to $800 over lifespan.

- Insurance. From $742 to $300 over lifespan.

- Fuel efficiency. MPG goes from 25 to 16 over lifespan. 12,000 miles a year at $2.50 a gallon.

Don’t agree? You can download the source spreadsheet and adjust any of the assumptions yourself.

Observations. It’s not surprising that leasing a brand-new car every 3 years is the most expensive, or that buying a 10-year used car and keeping it for a while is the least expensive. However, it may interest you that the calculations show that, for example:

- You would save ~$68,000 over 20 years if you Buy 10-year-old Used Car/Keep 5 years instead of always doing 3-year New Leases.

- You would save ~$20,000 over 20 years if you Buy New/Keep 10 years instead of Buy new/Keep 5 years.

- You would save ~$8,000 over 20 years if you Buy 5-year-old Used Car/Keep 15 years instead of Buy New/Keep 20 years.

My own thoughts on managing car costs. I like reading about models and statistics like this. However, my rule of thumb on affordability is more simple and behaviorally-based. If you want to achieve early retirement, you should only pay cash for cars. In my opinion, car debt and credit card debt are equally harmful to your financial health. In fact, auto loans may be worse – many can garnish your wages even after the car is repossessed. Financing obscures the real cost. When you’re faced with writing a huge check for $20,000 or whatever, your decision-making clarity is greatly improved.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

While I agree with the majority of your information the one exception to your “always pay cash for your vehicle” would be to take advantage of one of the fairly popular at the moment 0% for x months provided you DO have the cash to pay it off. Setup an auto payment and put the money where it can earn some interest.

Anything that lets YOU hold onto your money for a longer period “at no cost” is a plus in my opinion.

Sure, although I would add that you can often negotiate a lower price or additional rebate in lieu of 0% financing. (Sometimes the only option is 0% APR due to some form of direct promotion from manufacturer.)

That’s a great point – as long as you make those payments it lets you build!

*You don’t look cool in an old car…hard to find a spouse..

there is another option. Buy a slightly used car (current generation) and keep it for 5 years. You can enjoy all the latest and greatest without having to pay the premium for new car ownership.

You save even more money by not having a spouse or kids 🙂

The kind of spouse who would be attracted to a new car would not be the kind of spouse you would keep forever. Maybe “hard to find a girlfriend,” yeah, but not a spouse.

>> You would save ~$20,000 over 20 years if you Buy New/Keep 10 years instead of Buy new/Keep 5 years.

Or, stated differently, it only saves you $1,000 a year by keeping a car that is over 5 years old.

I don’t know if this takes into account tax/registration. I just bought a new car for my wife last year and got the registration bill, which was like $600 for 2 years In AZ.

Additionally I’m suprised they say that matance is 800 over 20 years, every car I have owned the transmission always goes out, and the last 2 cars the Ac has gone out both can cost over a grand to fix! And that’s just 1 thing going wrong

That’s a good point about the transmissions. I think $800 over 20 years is a bit low as well. Getting breaks replaced with new rotors at a shop cost upwards of 500, and even doing them yourself can get you up to $200.

I checked the spreadsheet and the 20 year calculation is 800 per year. the formula is $40 * vehicle age (so $0 for new and $400 for 10 years old.)

this is enough to cover a transmission at $7,600 total after $20 years.

If it’s happening with every car you sure that’s not just your driving? 😉

Buy a slightly used Toyota, Honda, Mazda or Subaru and keep 10-20 years. I have saved a wheel barrow full of money by doing this. Almost nothing goes wrong with these cars.

Our Toyotas have also performed this way. Even the 17year old one.

The graphic really puts in perspective the want vs need with cars. I’m personally fine with buying a newer used car to increase safety, the technology, and overall experience with it. From the chart this might cost me a grand or two, like the orange vs light blue dots.

This is personal preference though – I drove a 2004 until it couldn’t drive anymore, then upgraded to a 2012. It was awesome to finally have blue tooth and modern dashboard with touch screen. This experience I chose to enjoy since I sacrificed by driving the 2004 for so long.

What are your thoughts on balancing between money and experience, especially with safety?

Enjoy reading your post , but herez my take on this subject when there is a cheap loan take it. E.g. Honda from time to time have 0.9% APR for well qualified buyers , i dont see why should i offer cash down rather than take loan.

Another thing i noticed about Reddit chart -, it might not be good idea to generalize F-150 for all cars. We recently leased Chevy volt which after CA rebate and gas savings seems to be a good deal. Given battery tech is still evolving dont want to buy used one or dont want to own a car for next 8 or 10 years.

I’m 70 and have never made a car payment in my life. I can now afford to buy new and pay cash, but still won’t, and not just because I’m frugal (OK, cheap). I would dread parking a new car at the supermarket parking lot. Will my car get nicked by an opening door or drifting cart? Who needs it. A used car is already nicked. One more is nothing to care about.

Interesting chart, but it left out my favorite strategy: buying a 5-year-old car (so that its technology is reasonably current) and then selling it 5 to 7 years later.

When I buy that 5-year-old car, I then change all its fluids unless Carfax shows me they’re not needed. I also create a maintenance log showing every action I take on the car. Down the road, makes selling the car a LOT easier.

Frankly, don’t know why everybody doesn’t do this.

I agree with not financing cars if you can avoid it – they make a lot of money on the fees even if you get a decent rate.

I’ve written this before but want to raise it again – safety features on cars should really factor into your purchase. If you have the money and care at all about safety, I cannot imagine why you’d want to drive the same car for 20 years. Car safety technology is thankfully advancing every year, but that means committing to a new car in 1996, 2006, or 2016 for twenty years guarantees you will be driving a compartively unsafe car during the last 10-20 years you own it. Humans can be poor judges of threats – like how many people worry about airplane crashes but not car crashes – when you a far more likely to be maimed or killed in a car accident per mile traveled. But car fatalities are still a huge source of deaths, and you should buy your car accordingly.

I agree that cars today should be turned over more often than 20 years, but have a somewhat different basis: computerization and the decay of plastics.

First, if you test drive a ten year old “high tech” car of the day (e.g., 2007 Infiniti) you’ll be shocked at the dashboard and its limitations. Anyone with computer experience should worry greatly about circuit rot and sensor breakdown. Cars are getting more and more dependent on computers with each generation — have to wait and see if any technology can last 20 years.

Second, automotive plastics have about a 15 year lifespan when exposed to the elements. Everything from the seats and bumpers to to major engine parts start to crack and fail. The reliability and risk of catastrophic failure grows (e.g., on that summer trip out in the desert…).

Note that the collector and custom car market remains fixated on 1960s or earlier technology. These are analog machines (except for ignitions and fuel injection). They remain in this era because of simplicity, repairability, and the limited use of plastic.

One of the assumptions is :

“Fuel efficiency. MPG goes from 25 to 16 over lifespan. 12,000 miles a year at $2.50 a gallon”

Does that mean that they expect the MPG seen by the car to decline from 25 MPG at new to just 16 MPG at 20 years old? Is this typical? that seems like a very drastic reduction in efficiency. I was getting 25 MPG combined out of a 13 year old Toyota rated at 23city/32hwy new.

Yeah, I wondered about that part too. I’ve never owned a cart less than 10 years old, and the mileage is always around what the manufacturer says it should be. Sometimes I get more, and so I wonder how much has to do with driving habits.

Do a new graph with new Honda or Toyota.

Lease on cars as a tax deduction can throw a wrench into calculaion as well…

In about 5 years, once the last of the kids are out of the house & my older relatives stop driving, I’ll be switching to leasing the rest of my life.

I love our local mechanic, but with the half-dozen vehicles for which I’m responsible it seems I’m at his shop every other week.

BTW, maintenance of $800/year for vehicles over 5 years old is WAY too low.

Great topic and discussion points. Tough to generalize given: 1. miles driven/yr is a huge variable impacting costs [hard & soft i.e. depreciation]; 2. area driven – salt exposure deterioration from either road or ocean influence kills vehicles; 3. PM practices vary widely [most ignored are brake fluid and coolant changes – brake lines+calipers & heater cores = big$$$]; 4 HOW driven drives costs! Teen? Towing? Severe traffic? ZoomZoom? 5. The single largest cost is depreciation – residual value after 3 years is often < 50% depending on model. So skipping the initial 3-5 year depreciation seems key no matter how long the vehicle is owned after that! CRASH PERFORMANCE is PRICELESS!! Buy the safest you can prudently afford.

Comparing different length of car ownership doesn’t add up. If you buy new every 10 and buy 3 year used every 7, you need to compare over 40 years. Comparing a purchase every 10 years to every 20…of course it’s cheaper to keep a car longer.