I just experienced my own version of the “Expectation vs. Reality” meme when I looked at my monthly report from my Fidelity Investments securities lending activities, where I lend out my stock shares and get paid interest. I had been getting a lot of transaction notifications where all my shares of Paramount (PARA) were being lend out to somebody (most likely to short it).

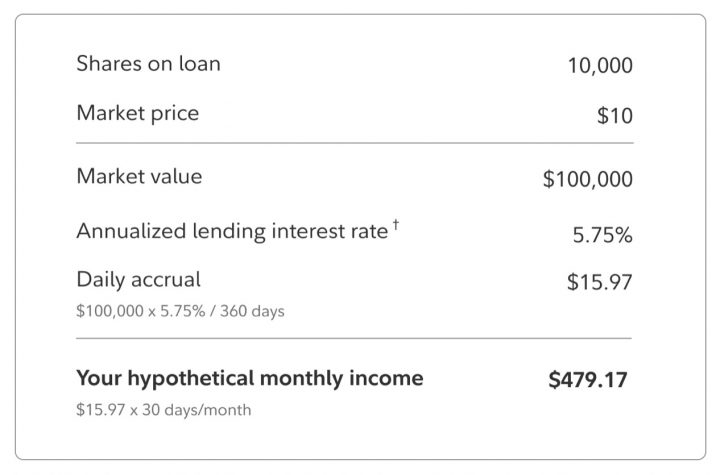

Expectation. I previously wrote about earning some extra income via Fully Paid Lending Programs in general, including that from Fidelity. In December 2021, Fidelity was showing this as an example scenario:

As of March 2023, the example scenario on the official Fidelity page shows a significantly lower income rate:

Still, over $400 a month of extra income from a $100,000 balance? I have a six-figure taxable Fidelity account, so I figured I was leaving money on the table! Let’s go!

Reality. Out of all my stock holdings, the only one to garner any lending interest was Paramount. This mostly makes sense in retrospect, as I tend to buy larger, high-quality companies when they are temporarily out of fashion. You don’t really see a lot of people shorting Berkshire Hathaway. Paramount is more of a value/cheap P/E and/or dividend play. (Although, Berkshire does own 10% or so of Paramount…)

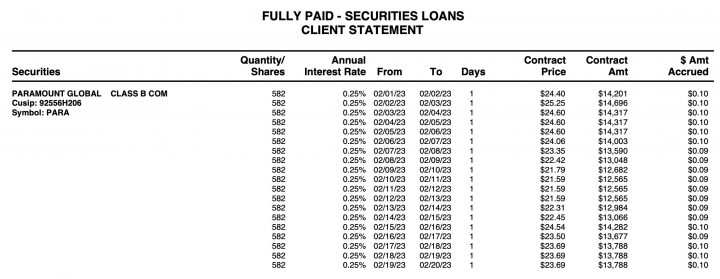

Here are my real-world stats on Paramount:

Shares on loan: 582

Market price: ~$23

Market value: ~$13,386

Annualized lending interest rate: 0.25%

Daily accrual: ~$0.10 a day.

Monthly pro-rated income: $2.79

Actual income: $1.91 (only borrowed for 19 days)

So… basically I was making 10 cents a day lending out my $13,000 of Paramount shares. At that rate, even if I had $100,000 worth of Paramount, I’d be making roughly 77 cents a day, or $23 a month. Nowhere near the $479 a month example.

Add in the fact that PARA is the only security being lent out in my entire portolio, and my securities lending income is currently working out to a pro-rate amount of less than 0.0004%, or 0.04 basis points.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

You should try with Interactive Brokers. They also publish a daily updated list of lending rates for all loanable securities. A few years ago they offered direct access to AQS, and individual investors had the ability to loan out shares in a transparent environment using market-based loan rates. However, the large brokerages put AQS out of business because they make too much lending out shares. Now securities lending is dominated by the big brokerages and inaccessible to most.

Wow, that’s quite a bait and switch! Why on earth are they lending out your shares at 0.25%? I’d like to start borrowing from Fidelity at 0.25%, how do we do that?

If you look at the financial statements of some large funds like S&P 500 for example, you can see securities lending income as a negligible amounts

For example, the Vanguard S&P 500 had $12.462 Billion in dividend income but only $3 Million in securities lending income…

That’s a good point, err observation 🙂 That’s about 2.4 basis points.

2.4 basis points on $100,000 would be $24 a year, which is about what I’m on pace for if I’m lucky!

I don’t like the lending programs because they are used to cover broker’s shady practices and make market manipulations much easier. It’s short sellers who needs the shares ‘loaned’ to them, but if the broker is using regular investors shares, suddenly you are a temporary partner in a covered call options trade that you never signed up for and may not be properly compensated for.

As we saw in 2021 with meme stocks, this lending of shares is a way for market manipulators to pressure the market with less risk to them. It can also end up artificially creating more shares of a company than actually exist due to the settlement rules for stock transactions.

Other issues that Fidelity and other stock brokers downplay:

-Shares on loan are not covered under Securities Investor Protection Corporation (SIPC).

-Cash distributions paid on securities borrowed over the dividend record date are credited as a “cash-in-lieu” payment, which may have a different tax treatment than the actual dividend from the issuer.

-You lose voting rights unless you recall the shares.

You should be aware of payment in lieu of dividends (PILs). M1Finance cost me over $2000 last year in extra taxes because they lent out my shares without my consent. Meaning my foreign dividend tax credit was replaced by high tax bracket interest income. Be aware.

M1 Finance caught me with that as well. Fortunately, I found out recently that you can email them to opt-out of the securities lending program. However, I wish they were more upfront about it as I wasn’t expecting so many of my dividends to end up as substitute payments.

That is annoying, so M1 makes you opt into securities lending by default? Fidelity at least credits you the dividends plus a credit assuming you are charged the maximum income tax.

Yes, M1 opts you into securities lending by default and doesn’t pay you anything for the shares they lend out:

“You are opted into the Program upon Agreement execution, but can opt-out at any time by sending an email to M1 at help@m1.com with “Securities Lending Opt-Out” in the subject.

Revenue from the Program is collected by Apex Clearing and a portion of that revenue is shared with M1 as the introducing broker. You do not receive any portion of the interest.” – Quoted from their securities lending disclosure document.

I only found out about this because they recently sent me an email with an update to my securities lending agreement. Prior to that I didn’t even realize that I was involved in a securities lending agreement. It’s a really shady practice by M1. I wish Fidelity or Vanguard had something similar to M1’s automated investing pies. If so, I would switch from M1 in a heartbeat.

Jonathan, could you please share with us the metrics you use to evaluate potential candidates include in your portfolio and also to exclude from your portfolio?

What tools do you use?