I’ve been getting my butt kicked by a bout of food poisoning, so posting will be light this week. Fever, chills, sweats, and I haven’t been able to keep down any solid food in over 48 hours. Blech.

What Does 200 Calories Cost? A Visual Guide (Economics of Obesity)

Posted on April 25, 2013 // 75 Comments

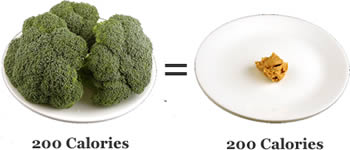

WiseGeek has an interesting article on What Does 200 Calories Look Like?, where it photographs the portions of several foods that equal 200 calories and sorts them by weight. Here’s broccoli next to peanut butter on the same plate:

I thought it would be neat to extend this idea and see what 200 calories costs. So I extended my usual grocery trip by finding out the price per weight for each of the food items they selected. The results are below, grouped by price per 200 calories. Image credits go to WiseGeek.com. Please go there for the full versions, these are just thumbnails for reference.

| Cost of 200 Calories: Less than 50 cents | |||

Canola Oil $0.07 |

Wheat flour $0.07 |

Brown Sugar $0.10 |

Peanut Butter $0.17 |

Cornmeal $0.20 |

Uncooked Pasta $0.21 |

Glazed Donut $0.23 |

Butter $0.24 |

Salted Pretzels $0.24 |

Wheat Dinner Rolls $0.23 |

French Sandwich Roll $0.24 |

Smarties Candy $0.24 |

Why You Should Make a New Year’s Resolution

Posted on December 28, 2012 // 2 Comments

If you’re like me, you may wonder if a New Year’s resolution is even worth the bother. By chance, I was listening to an NPR interview today with a Dr. John Norcross, a psychology professor who decided to study this phenomenon. Listen, download the mp3, or read the transcript at NPR.org. Here are the highlights:

If you’re like me, you may wonder if a New Year’s resolution is even worth the bother. By chance, I was listening to an NPR interview today with a Dr. John Norcross, a psychology professor who decided to study this phenomenon. Listen, download the mp3, or read the transcript at NPR.org. Here are the highlights:

According to Norcross, 40-50% of people make New Year’s resolutions each year. How did they do when studied over time?

Dr. NORCROSS: In two of our longitudinal studies, 40 to 46 percent of New Year’s resolvers will be successful at six months. So, the half empty is it’s true, most people fail. But 40 to 46 percent is pretty impressive. […]

You know, I was tired of people saying resolutions never succeed, we shouldn’t even try them. And I said, well, wait a minute, these are life-sustaining behaviors. What’s the alternative? So, the alternative was to track people starting before January 1st with the same behavioral goals, with the same motivation to stop or to take the resolutions but who just weren’t going to do anything then. And that’s – and only four percent of them were successful at six months. So you go from four percent, all the way up to 44, 46 percent by taking a New Year’s resolution seriously and trying to do something about it.

10 times the success rate! So people who made resolutions had a 40% success rate as compared to 4% from those who had the same motivations but didn’t set resolutions. Definitely encouragement for would-be resolvers. More goods news is that the studies found that slips or short lapses in the resolution did not always lead to failure. Many people used the lapses to strengthen their determination.

How to set a good resolution. Norcross recommends setting attainable, realistic, and measurable goals. So lose 10 pounds instead of 50 pounds or “a lot of weight”. Save $100 more from each paycheck vs. saving an extra $15,000 somehow during the year. Grandiose goals set you up for failure, as you need to have inner confidence that the specific goal you set is achievable. This agrees with the popular SMART mnemonic that says that goals should be Specific, Measurable, Attainable, Relevant and Time-sensitive.

So, resolutions are good, especially if you do them right. However, you may want to keep number of resolutions to a minimum:

FLATOW: So you do one thing at a time, you know? Don’t say, I’m going to diet and quit smoking at the same time, because you’ll never get them both done.

Dr. NORCROSS: Well, there’s some interesting research on that. And that is, it depends how much time and commitment you have. If the two resolutions are related, then it may make sense to do it together. For example, losing weight and increasing exercise – most people see those things as going together. But if there are two very different resolutions, you may just be overwhelmed with the amount of time and energy that they call for. So, we ask people never more than two. If they’re related, two is great. Otherwise, just do one at a time.

Link Digest: Mixing Work & Passion, Invest in Memories, Stable Value Fund Warning, and More

Posted on April 27, 2012 // 4 Comments

Here are some more links worthy of sharing:

The Overjustification Effect

A smorgasbord of behavioral psychology that questions the idea that there is nothing better in the world than getting paid to do what you love. This is a very complicated topic but the article makes some good observations.

Memory as a Consumer Durable (Atlantic)

Another twist on the whole “buy experiences, not things” theory. What if you treated a memory as “consumer durable” good much like refrigerators, furniture, or a car? In similar ways, they provide constant satisfaction and/or pleasure, and they last a very long time. In that case, should we acquire them while we’re young so we can enjoy them the rest of our lives?

Stable value 2.0, fewer investor guarantees (Reuters)

If you own a stable value fund in your retirement plan, you should check to see if changes were made to any of its principal guarantees.

The 401(k): Americans ‘just not prepared’ to manage their own retirement funds (WaPo)

401k were designed to be a supplemental account to pensions, but now they are a replacement. If you know what you’re doing, it’s good, and it’s nice because you can take the money with you across jobs. But the total account balances are nowhere near what people need to retire as a whole. Maybe we need something else.

“If the 401(k) is supposed to be the primary retirement vehicle for the average American worker, then it needs to be consistent with the information and financial ability of the average American worker, who is just not prepared to manage funds like that over the course of a lifetime.”

GMO 2012 1st Quarter Letter

The most recent letter from Grantham talks some sense about why most managers can’t afford to have the proper long-term mentality for market-beating returns.

…ignoring the volatile up-and-down market moves and attempting to focus on the slower burning long-term reality is simply too dangerous in career terms. Missing a big move, however unjustified it may be by fundamentals, is to take a very high risk of being fired. Career risk and the resulting herding it creates are likely to always dominate investing.

CarrierCompare: The iPhone app your carrier doesn’t want you to see (CNN)

An iPhone app that takes data (signal strength, response time and speed) from users and analyzes it together to find which carriers have the best service and coverage for any given area. (Update: Apple has since removed it from the App Store.)

Link Digest: Paying For Status, Nutella Class Action, Social Security Planning, Being Your Own Bank, and More

Posted on April 18, 2012 // 11 Comments

The Perils of Paying for Status

An article in Scientific American magazine about our desire to feel powerful and achieve social status affects our decision-making. If you’re feeling insecure, you’re more likely to overpay for products and/or buy more stuff than you need. Simply knowing this common weakness may help you spend more wisely in the future.

Nutella Class Action Lawsuit

Nutella calls itself healthy, when in fact the first two ingredients are sugar and vegetable oil (fat). Class action lawsuit ensues. Lawyers get rich. Regular folks who bought the stuff can get $20 with a claim, with no proof of purchase required. If you’ve ever bought Nutella spread since 2008, you should check if you’re eligible.

Social Security and Medicare: Proper Planning Pays Off Big

I’m not an expert on this stuff, but this Morningstar article seems to do a pretty good job of summarizing the ways to maximize your Social Security and Medicare benefits and minimizing any penalties.

I Quit My Passion and Took a Boring Job

A guest poster at GetRichSlowly shares his story of quitting a job he loved (teaching high school math) and taking on a job that pays the bills (accountant).

Bestselling book’s financial promises don’t add up

Allan Roth at CBS Moneywatch does a great job debunking a “bestseller” book that is one of many misleading scams that pushes whole life insurance as “infinite banking” or “make your own bank” as a good way to build wealth. It’s a great way to build wealth, but only when you’re the one selling the whole life insurance!

What Does the Prudent Investor Do Now?

WSJ article by author Burton Malkiel about his outlook on stocks and bonds. If you can’t read it directly, try here and click on the first result.

In today’s environment, the minimization of investment fees is more important than ever. A 1% investment management fee may appear to be very low when measured against assets. But when measured against a 7% equity return, that fee represents more than 14% of the return. Against a 2% dividend yield, the fee absorbs one half of the dividend income.

GMO Quarterly Letter Q4 2011 (pdf)

Another letter to investors that I have come to enjoy reading each quarter. Jeremy Grantham gives some good investment advice, and also some market opinions that may or may not be right. I don’t necessarily agree myself, but I like his style. Right now he only likes “high quality” US equities, and he hates going long on bond duration to reach for yield.

Reading List: Low-Risk Investing, Free Accounting Software, Limited Willpower, Flexible Withdrawal Rates

Posted on February 29, 2012 // 9 Comments

I run across a lot of articles that may not merit an entire blog post but are worthy of sharing. Let me know if you like this format with short summaries or if you’d rather me just tweet links.

Playing It Safe as a Long-Term Strategy

For a while, Professor Zvi Bodie has written books and articles about low-risk investing and encouraging the purchase of Treasury Inflation-Protected Securities (TIPS) and I-bonds. If you bought them when he was first saying that, you’d have TIPS paying 3%+ real yield and doing quite well. But now you’re looking at 0% or negative real yield unless you go decades out to eek out 1%.

He still says that stocks are too risky regardless of time held and should not be bought unless you already have enough assets to cover the bare necessities. You won’t like the alternative options: spend less, save more; plan on retiring later; work a second job. He and Taqqu have a new book called Risk Less and Prosper.

Berkshire Hathaway Letter to Shareholders

Warren Buffett sent out his annual letter to shareholders over the weekend. As usual, the letter contains some of his insights and opinions on issues like the housing market recovery, investing in gold, and the current dangers of bonds. He also lays out his argument for why owning equities (at least BRK) is actually low-risk over a long time horizon.

There has never been a better time to be an individual investor

From the Abnormal Returns blog. I agree that there are better tools out there now at a lower cost, but with the death of pensions there will also be a lot more responsibility and pressure placed on individual investors. If they mess it up, it’s not going to be pretty. That makes it a stressful time to be an individual investor!

Wave Accounting: Free online accounting software for small businesses

The price is right at free, as they intend for it to be ad-supported. Includes free import of transactions from your bank account. I signed up but haven’t taken it for a test run yet. I currently use Intuit Quickbooks and haven’t had to upgrade for 5 years.

Your Mistaken Belief in Financial Willpower

I have come around to support the idea that willpower is more of a finite resource, or at least it has to be built up like a muscle. Don’t use it up when you don’t have to. Carl Richards of the NY Times points out ways that we can conserve our willpower for other things using automation for paying bills and savings.

Should Your Retirement-Portfolio Withdrawals Fluctuate With the Market?

What is the best way to withdraw from your portfolio in retirement in order to make sure it lasts? This Morningstar article looks at the research on ways to implement flexible withdrawal rates. I agree that numbers like 4% withdrawal rates should be a guideline and not a rigid rule.

Labor Day Weekend Links: Insurance for Freelancers, Google Looks For Money Advice, Vanguard Canada, and More

Posted on September 6, 2011 // 3 Comments

I hope that everyone managed to have a relaxing and refreshing long weekend. I managed to catch up on some Instapaper reading, and here are some links worth sharing:

Freelancer’s Union

Independent workers make up 30% of the nation’s workforce, and the FreeLancer’s Union is trying to help organize them into a stronger community. The primary reason I found this interesting is in limited geographical areas, they offer ways to get affordable health, dental, and disability insurance to freelance workers. Finding non-employer-linked insurance is a big concern of mine in the future, and perhaps more localized freelancer groups can help.

The best investment advice you’ll never get (San Francisco Magazine)

In 2004, when Google’s IPO occurred and made hundreds of young multimillionaires that quite possibly had no idea how to handle that money, their management team did something very clever. Instead of just shunting them to Goldman Sachs or Morgan Stanley “predators” :), they brought in a series of speakers to talk about investing. This included names like Bill Sharpe, Burton Malkiel, and Jack Bogle. Read this (long) article to see what they were shown.

Vanguard Is Coming To Canada (Marketwatch)

I did not know this, but according this article Canadian investors are not able to buy Vanguard mutual funds offered in the US. They can, however, buy the same Vanguard ETFs. Well, Vanguard has recently announced that it plans to open 6 low-cost index ETFs for the Canadian market, including an MSCI Canada ETF, a Canada Aggregate Bond Index ETF, a CAD-hedged US Total Market ETF, and a CAD-hedged EAFA Index Fund. It may also open corresponding open-ended mutual funds. This development should put significant pressure to lower costs across the industry.

Intuitive Probabilities – Blackjack and Loss Rebates (Kid Dynamite)

There was some buzz recently about a guy playing high-stakes blackjack that walked away with another $1 million winning session. It was revealed that to entice his play, the casino actually rebated 20% of his losses. Basically, he got to keep whatever he won, but if he lost $1 million, he would only have to pay $800k. This may sound like a sweet deal, but this article shows that with as little as 100 hands played in a session, the casino is still theoretically ahead. The house still wins. Kind of like a lot of hedge funds. You give them your money to invest/gamble, and if they win, they keep 20% of the winnings. If they lose, hey, it was your money. 🙂

Create Time to Change Your Life (Zen Habits)

Making clear priorities allows to you see what you need to do, but you also need to cut out some existing things as well. You may think you can just cram it all in, but you really can’t without burning out eventually.

Chase British Airways Card: $50 off two meals at Michelin-starred restaurants

If you got this card from the previous 100k mile bonus offer, they are offering two $50 off $50 purchases at fancy-schmancy restaurants with Michelin stars. A nice perk, although a meal at these places can easily run a lot more than fifty bucks. I’m sad to say I have never eaten at any of these fine establishments. Le Bernardin would be top on my list.

Refinancing While Underwater (NYT)

Includes different options on how to refinance your mortgage if your home’s value has dropped such that you owe more than your house is worth.

If your loan is owned by Fannie or Freddie, you may qualify for the Home Affordable Refinance Program, or HARP. Some 2.5 million to 3 million homeowners may be eligible to use HARP, according to government estimates — provided, among other things, that they have not been late on their payments more than once in the last 12 months.

Savings Growing at a Glacial Pace?

Posted on August 2, 2011 // 8 Comments

Hello from Alaska! I’ll be back to regular posting shortly.

Reading: Calorie Labels Fail, Family Income Growth is Deceiving, Law School Economics

Posted on July 20, 2011 // 1 Comment

Here’s some articles that caught my eye this week:

Calorie counts don’t change most people’s dining-out habits – Washington Post

Apparently, telling people the amount of calories on menu items doesn’t change their eating habits, cheap or not. Now, I know that I personally do find it helpful, because many times I’m eating out primarily to hang out with friends and the food is not the goal. But in general, we must fight our human nature:

Experts say that for most diners, the issue is not about having information but about lacking self-control. Behavioral economists have for years zeroed in on a logical hiccup: We are unable to balance short-term gains with long-term costs. Many humans are simply really, really impatient. With eating out, the gains are immediate (yummy giant burrito!) and the costs are delayed (staggering bills for heart disease!).

Overtime, Not Wage Increases, Drive Income Growth – WSJ

Working families’ incomes have grown in recent decades. But the gains came mostly because they worked longer hours than because of wage increases, according to new research by the Brookings Institution‘s Hamilton Project. […] Among two-parent families, median earnings did rise by an inflation-adjusted 23% from 1975 to 2009. But the parents’ combined hours worked increased by 26% during the same period–accounting for most of the income gains.

The median income for two-parent families rose to $70,000 in 2009, for working 3,500 hours a year on average, compared with working about 2,800 hours in 1975 to earn $56,600 (in 2009 dollars). Hmm.

Law School Economics: Ka-Ching! and Reactions – NYT

Law schools have the power to raise prices and increase enrollments without any decrease in demand… even as the job market worsens for lawyers. Result: Law school tuition rises 4x faster than even overall college tuition costs, which are already skyrocketing. Are law schools abusing this pricing power?

Tinkering With Site Design

Posted on July 12, 2011 // 16 Comments

I changed up some of the design of the website last night, not really sure why, I had some free time and have been meaning to try some things out. I don’t have the motivation to do a complete redesign, but wanted to update things slightly to account for modern screen sizes and resolutions. I’ve made the content a bit wider (this also allows for larger embedded images), widened the sidebars a bit, made the text a bit bigger, and changed the spacing a little. Let me know if you have any suggestions.

Weekend Reading: The American Dream, Dollar Coins, Fidelity Problems, and United/Continental Merger

Posted on July 4, 2011 // 12 Comments

Happy Birthday America! Here’s some of what I’ve been reading over the long weekend:

Happy Birthday America! Here’s some of what I’ve been reading over the long weekend:

The Death of the American Dream I

A good long-ish editorial from the The American Interest magazine about the “American Dream”. The American Dream used to be owning your own family farm. “In 1900, 41 percent of Americans worked on farms. Today fewer than 2 percent do.” The updated Dream became lifetime employment (plus a pension of lifetime income) plus owning a home through a 30-year (half a lifetime) mortgage. There is no longer lifetime employment these days, and perhaps the government-subsidized 30-year mortgage is up next. Also see Part II.

$1 Billion That Nobody Wants

An NPR investigative article about how the US government keeps making billions of dollar coins, even though most people prefer paper bills. I suppose this answers why you can buy coins from the US mint with a credit card, enabling people to rack up credit card rewards, and also a good way to meet minimum spend requirements for the big bonus cards. I think the two options should be to either stop making paper bills, or stop spending so much money pushing dollar coins on us. Until then, since the coins exist already, we are essentially getting paid by the government to distribute them.

Fidelity’s Experience Proves Bigger Doesn’t Mean Better

Morningstar article outlines reasons why Fidelity is having some issues with their actively managed funds. One issue is manager turnover; Their average manager tenure is 3.2 years, ranked 24th out of the 25 largest firms. They also have too many funds and not enough talent for all those positions. For example, Fidelity has 17 large-growth funds geared toward retail investors alone. As they earn a big chunk of profits from retirement plans, they will be much less likely to allow unconventional managers who take risks for big returns. Also see my review of Fidelity’s Portfolio Advisory Service product.

United and Continental Merger Updates

If you haven’t heard, United and Continental are merging, and you can link your accounts and transfer miles between the two frequent flier programs at your convenience. Combine your two balances to make one award flight, for example. I’m a United Elite and I heart my Economy Plus seats. Thanks reader Michael for the tip.

The Continental OnePass Plus credit card is still offering 30,000 miles + $50, and will still work after the merger.

Crunching The Numbers & Looking Into The Crystal Ball

Posted on May 24, 2011 // 9 Comments

While catching up on some reading over the weekend, I found two articles that both dealt with large issues that we’ll have to face over the next few decades. Predicting the future is always difficult, but sometimes the numbers can seem very compelling.

Oil & Commodities

Jeremy Grantham is co-founder of GMO, an investment management firm with $107B in assets. That doesn’t mean he necessarily knows the future. But in his April 2011 quarterly letter titled Time to Wake Up: Days of Abundant Resources and Falling Prices Are Over Forever, he does manage to put together a convincing argument that we are using up our natural resources very quickly, and we can’t continue on at this rate. It’s mathematically impossible.

Will we find other energy sources to replace cheap oil? Will technology allow us to do more with less? Probably, but I doubt the transition will be a smooth one. I think learning to be less dependent on natural resources (read: be frugal, efficient, and less wasteful) will even more important financially than it is now.

Medicare & Taxes

Paul Krugman is a Nobel-winning economist with a popular blog at the NY Times. In a recent Op-Ed titled Seniors, Guns and Money, if you strip out all the political stuff, you’ll find this: In the coming years, there will be either significant cuts in Medicare, or tax increases to pay for the rising heath care costs.

One, our population is aging, with more retired seniors being supported by fewer workers. Two, health care costs keeps rising on their own. As he says, “It’s just a matter of arithmetic.” Either the government will raises taxes to pay for all this, or there will be major cuts in benefits. My guess is both.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)