Updated for crazy 2020. The big news yesterday was that one measure of crude oil prices actually went negative, because futures were coming due and nobody had any place to store the oil upon delivery.

Why did this happen? Part of the reason is that too many people had the following plan:

- Crude oil has dropped to $18 a barrel. These prices are multi-decade lows.

- Oil prices must go up again… eventually… right? Look at that historical chart!

- The futures market is kinda complicated… I know! I’ll buy an ETF like USO.

- Profit!?!?

Here are a few things you should know first about the United States Oil Fund (USO) and similar oil ETPs.

You aren’t the only one who’s thought of this. Billion of dollars have come and gone into oil ETFs in the past few years. Here are articles from 2014 and 2015 when oil dropped to below $50 a gallon after being over $100:

- Cash-Burning Bets on Oil Rebound Surge in U.S. ETF Market (Nov 2014)

- The Perils of Bargain-Hunting With Oil ETFs (Jan 2015)

- Oil Prices: The Perils of Bottom Feeding (Jan 2015)

In April 2020, USO ended up having to actually change how the ETF operated in order to avoid some the market distortions that the speculation caused.

The usual market timing questions apply. Sure, the price will go up, but how long is “eventually”? It might be 1,3,5, or 10 years. If you have a specific time-frame in mind, then you can go out on the futures market and then buy a specific contract. But if oil hasn’t risen enough at that time – maybe it peaked earlier and dropped, or it peaks further in the future – you’ll have lost money.

If you buy the ETF, when is a good time to sell? $40 a barrel? $80? $100? What if you sell and then it rises another 50%?

What if it takes a while? The longer you have to hold these ETFs, the less likely they will track the price of oil (see below). Meanwhile, the ETF provider is happily collecting their annual expense ratios of 0.50% to 1%. At the current asset level of $4 billion times the 0.45% management fee, that’s $18 million a year in fees.

Your commodities futures ETF may not track the price of oil very well at all. To properly track the price of oil, you’d need to buy some oil and store it somewhere (and pay storage and security costs). These ETFs don’t do that, instead they buy oil futures contracts and keep rolling them over into new ones when they expire. That’s not the same thing. USO is designed to track daily price movements in the price of oil, not long-term movements!

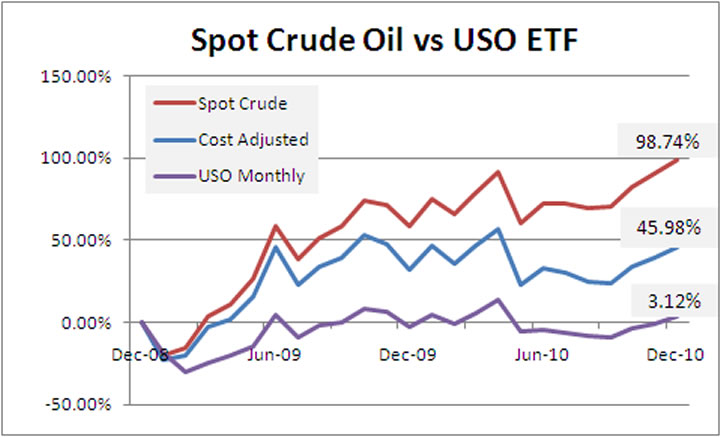

Oil prices doubled from in 2009-2010. USO went nowhere. Visually, here’s a chart from Attain Capital that compares the change in USO share price (purple) as compared to the spot price of crude oil (red) when oil prices doubled between the start of 2009 and the end of 2010 (blue line adjusts USO underperformance for roll costs):

From the Bloomberg article above:

Since USO launched in April 2006, it has returned -71 percent, while the spot price of oil returned -26 percent. The last time oil roared back from a bottom was in 2009, when it returned 78 percent on the year. USO returned just 14 percent.

If you don’t understand the terms “backwardation”, “contango”, and “roll costs” then you don’t understand commodities futures. If you don’t understand something, you probably shouldn’t buy it. The more people crowd into this trade, the weirder the futures markets get. Who would think that you could get paid to take oil from someone? Take it straight from a USO executive:

John Hyland, chief investment officer of USO, says the fund is a “tactical trading vehicle predominately used by professional traders,” and not meant to be a buy-and-hold investment.

In the end, such a play is a speculative bet and it may just pay off, who knows. But it certainly isn’t a wise investment, especially if the tool you’re using doesn’t even do what you want it to do.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Thanks for the post Jonathan, I had a similar thought, but decided against USO and OIL. If you want to make a move on the idea that oil prices will go up, I am wondering if less risky ETF to consider would be XLE, the Energy Select Sector SPDR Fund. It’s an ETF to aims to track the performance of the Energy Select Sector Index. The index includes companies from the industries including oil, gas & consumable fuels; and energy equipment & services. It appears to have a low expense ratio (0.17%) and a 10 year return of 9.85%.

In my opinion, it probably won’t track oil prices very closely either, but XLE at least invests in companies that should create long-term value and profit.

I definitely have zero clue about commodity futures and I think that’s a blessing. Thanks for sharing this post.

thanks! you read my mind, was just thinking of investing in an oil ETF

Also, USO is run as a partnership which means a k-1 come tax season, adding to complexity. It’s not as simple as a 1099 and you’d have to wait until you got your k-1 to file your taxes. Plus commodities may not be taxed the same as equities.

Good points.

Don’t buy what you don’t know. OK, but are really sure you know what you are buying though?

I actually did this very same analysis and came to a different conclusion entirely. My first problem with this analysis is: why are they using data that’s over 4 years old? Its extremely easy to get spot price oil and uso’s price from yahoo from 2011 forward and plug it into an excel just like Attain did for ’10 backward. So why didn’t they? I expect some discontinuity between the two series as some of the money in the ETF is leaked through expenses the fund has, and I do see some. From 2011 forward oil fell 40% while USO fell 42%. I can live with this discrepancy and decided to invest in USO.

I wish I could post a chart from 2011 forward, it shows a very different picture. Anyone trying to argue USO doesn’t follow Oil prices should look at it.

From 2012 onward oil prices have been pretty stable, there has been little reason for it not to track properly. Only recently has there been a huge drop in oil prices. 2009 to 2011 represents a 2-year period when oil prices doubled, which is exactly what people think will happen again over the next few years. From $50 back to $100 oil.

The article states “rolling them over” as the reasons they don’t track. Not rising prices. Is rolling over harder to do when prices rise (I don’t have any reason to believe it is)? Or did USO just get more efficient at rolling over?

I’ll admit the article makes me think a bit, but some additional information would be needed to draw a conclusion.

Check out this article (also by Attain Capital), especially the section “Roll Yields, Contango, and Backwardation”.

http://www.nasdaq.com/article/3-big-reasons-commodity-etfs-arent-getting-the-job-done-cm252347

Thanks, these articles (and your feedback in the comments) are why I keep coming back to your site. In light of this new information I will hold off on buying more shares of USO. I am still optimistic about USO though for a couple of reasons though.

1: I read in bloomberg that contango isnt as big this time as in ’08–future contracts are only 6$ above spot instead of 11$ above

2:Probably more important, it seems the ETF’s have indeed learned from their mistakes. From your NASDAQ article:

“But some of these commodity ETF folks aren’t as dumb as they look, taking steps over the last year or so to address the problem – we covered some of their efforts in a recent blog post . These new ETFs are getting their commodity exposure by investing in a blend of futures contracts for varying maturity dates. For example, the Teucrium Corn ETF tries to minimize the problem by not just plowing into the front month contract for the market they track. Instead, they use the following futures contracts: (1) the second-to-expire Futures Contract for corn traded on the Chicago Board of Trade (“CBOT”), weighted 35%, (2) the third-to-expire CBOT corn Futures Contract, weighted 30%, and (3) the CBOT corn Futures Contract expiring in the December following the expiration month of the third-to-expire contract, weighted 35%. This dynamic, multi-month roll process is their attempt to reduce the impact of Contango markets eating into profits (or compounding losses).”

These commodity ETF’s have massive decay built in to them. Given that, why not take the opposite side of the trade — Short DNO (DNO is the inverse of UNO), so when oil goes up, DNO goes down and you make money. And all of the contango issues work in your favor. Paying 5% interest seems like a good trade to have these decay factors work in your favor.

Not a bad idea. I see DNO hit an all time high today. But shorting DNO and paying 5% interest seems too much. Better do it with options. Buy in the money put. Say $95 Sep2015. To cover the slight premium, sell $45 Sep2015 put. Not a bad bet to make 30% in 9 months. If oil goes up, you will make money. If oil trades sideways around $45 (most likely), you will still make money as these ETFs loose between 1% and 3% per month. I may actually try this trade if oil goes crosses the $40 line.

I get what you mean with everyone following a trend of buying complicated oil investments just to profit from lower prices. Isn’t that the name of the game, buy low and sell high. If you predict oil will go down from here, then by all means do not buy. But if you see it going to $80 a barrel again, why wouldn’t you buy a mutual fund or an index fund tied to oil companies? Once you hold it for a few years and the price goes up, you can do a fee free exchange for another mutual fund that tracks the total market. I don’t see anything too drastic with a plan like that. Thanks for the article.

Are futures’ profits/losses taxed at both short/long term capital gains as a percentage, like 40/60, or something like that? Where would you buy speculative futures or e-mini futures? Any ideas for good brokers without miscellaneous fees and #trade requirements?

You are totally right. Investing in commodities such as oil, gas, gold etc… is speculating.

I have first hand experience with USO. During the last drop ( 2009-2010ish ) where oil price were below $40/barrel, I wanted to invest in oil since I was sure that oil price would go up. I found USO and without knowing too much about it, I bought a few hundred shares. Like what was mentioned by some, the tax filing for the type of partnership is a real pain. After a few years, I was tired of the extra tax work, I sold the shares. Oil price was more than double from the time I bought the fund; however, the fund went up only about 30%. I was a bit puzzled, but now after reading more into it, I understand why. I guess I was lucky that I made some money despite investing in something I didn’t understand very well. Won’t do that again though.

Thanks for sharing the info on this subject.

So will USO ever go up? If contango and roll costs and management fees are a constant and never ending drag on USO performance then isn’t the ETF just slowly going to go to zero?

There must be some scenario where USO goes up in a way that somewhat mirrors the price of oil.

On a daily basis, sure, USO can and will go up. USO is designed for traders, not long-term investors.

Well that answer seems to imply that the ETF is condemned to eventually go to zero. Saying it can go up on a given day (what I think you are saying) implys that the long term prospect is that it will relentlessly and steadily go down because of contango, roll costs and fees. If the vehicle is always going down, except on the odd good day, then it really doesn’t matter how people trade it. People will loose money. And the price can’t shrink forever without eventually hitting zero. Am I missing something?

It’s possible for a basket of futures to go to zero, if the commodity futures are permanently in contango. But they aren’t. Historically, there is on average a positive roll return due to normal backwardation. Also, commodity futures are usually collateralized with TIPS which also provide a positive return (again, usually). This is my limited understanding, I am not a commodities expert.

My limited research indicates that contango is more of a normal state for USO than backwardation. In fact we see that USO looks to be in contango state right now. The price of West Tezas Cruse is up about 12% today and USO is only up 4%. Classic Contago underperformance relative to the commodity being tracked.

So if an investor was in USO apparently it would be wise to sell it before they roll their next contracts?

So i don’t understand contango, or backwardation or most of this post.

I did buy USO as i saw it was once at 20 dollars and was sitting around 9-10 dollars, at this point i own 156 shares (i know i’m small time) and i’m up around 600 dollars, should i bail before it crashes, or hold on. perhaps i should have gotten smart before investing. I was actually just looking for some indication of its nearterm predictions when istumbled across some fairly negative ideas about USO as a whole.

time to revive this thread

Okay, let’s take a look!

Thanks. I think this article helped some people, including myself.

Excellent article. I loved the line “If you don’t understand something, you probably shouldn’t buy it”.

I’ll sit back and enjoy the gyrations of WTI crude prices.

Thank you for this. I’m glad I read it before I bought any. And the 8:1 reverse split and K-1 tax consequences solidified for me that I should avoid it.