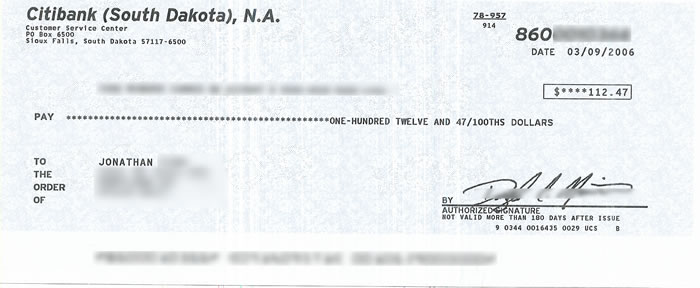

I guess Citibank doesn’t hate me as much as I thought they did. I just received my cashback check for $112.47, right on time:

You gotta love getting over $100 in free money just for pumping gas and buying groceries!

I guess Citibank doesn’t hate me as much as I thought they did. I just received my cashback check for $112.47, right on time:

You gotta love getting over $100 in free money just for pumping gas and buying groceries!

My ‘How Do You Budget?‘ post was a nice success, and the giveaway winner has been notified. Here is a breakdown of the replies:

Apparently this is the big news today. Check out Google Finance for yourself. More evolutionary than revolutionary, but as always competition is good, and will lead to more improvements for all finance sites. Yay AJAX.

Ah, mutual fund companies love your money, and fully realize many people are lazy, busy, or just don’t want to deal with money. So they created the All-in-One fund. The one I like the best for our purposes is the Vanguard Target Retirement 2045 Fund (VTIVX). I don’t really care about the dates on the funds, as each company does things a bit differently. Let’s look under the hood. Currently, VTIVX has the following underlying funds:

Vanguard Total Stock Market Index Fund (VTSMX) – 70.4%

Vanguard Total Bond Market Index Fund (VBFMX) – 12.1%

Vanguard European Stock Index Fund (VEURX) – 11.8%

Vanguard Pacific Stock Index Fund (VPACX) – 5.7%

[Read more…]

When I talk about maximizing your return (reward) for a given amount of risk, that is called being on the Efficient Frontier. For a very neat illustration of this, check out this Interactive Risk/Reward Chart from IFA, which lists 15 index portfolios as well as 20 of their suggested portfolios.

The individual index portfolios illustrate that individual asset classes like 1-Yr Bonds, Emerging Markets, or Micro Cap each have their own risk/reward characteristics. But, if you combine a bit of each, you can make a nice happy combination to optimize your risk/reward ratio. Why take any extra risk without more reward? That nice sloping line is the Efficient Frontier. My portfolio options are somewhat similar to the #80 dot, but with some tweaks to minimize expenses and complexity.

[Read more…]

Now, let’s see if we can take the slice and dice portfolio option and make it a bit simpler, and hopefully avoid all extra fees.

Theoretical Allocation

20% S&P 500 (VFINX or VTGIX)

20% Large Cap Value Index (VIVAX)

20% Small Cap Value Index (VISVX)

10% REIT (VGSIX)

20% Total International Index (VGTSX)

10% Intermediate-Term Bond (VFICX)

[Read more…]

Man, figuring out a good set of funds to work into your asset allocation plan is hard! There are so many different funds to choose from. So I’ve decided to break it down into three possible scenarios that I can then choose from, varying from complex to super-simple. The first scenario is to pick a variety of funds that each focus on a specific asset category. This will result in more complexity and possibly higher fees, but in theory may result in better long-term returns.

First, I’ll list the funds that I would use in theory, and then I’ll list how they would actually fit in reality into our two Roth IRAs, one Traditional IRA, and taxable accounts. The goal is to put the most tax-inefficient funds into the most tax-deferred accounts.

[Read more…]

As mentioned before, our goal when investing is to maximize the potential return for the amount of risk we decide to take. But how do you find that out? It seems the traditional way to decide this is through what financial planners call a Risk Questionnaire. You answer a series of multiple choice questions, and in the end it suggests an approximate asset allocation, usually telling you how much to put into stocks and how much in bonds.

Having more stocks give you higher overall returns, but higher volatility. Having more bonds does the opposite – it gives you lower returns, but decrease the up and down swings of your overall portfolio. Let’s try out some online risk surveys and see what comes out…

[Read more…]

If you love getting a good deal and have a partner that shares your passion, then you probably already know that you can double your pleasure by both using the same coupon (one per person, right?) or signing up for bonuses separately, and then getting double the money!

Alas, I, who truly loves wringing money out of companies, has a wife who hates this stuff. She works hard and controls her spending well, but is the type of person who chooses which credit card to carry based on how cute it looks. The words ‘S&P 500’ mean nothing to her. There could be a $1,000 bank bonus and she wouldn’t care. I can’t even sign her up for offers myself anymore, since she really hates having to deal with customer service reps if something goes wrong. The last thing she signed up for was the $100 gift card from Citi, and only after I did it first (and convinced her she could spend it on cute stuff). But I still love her =) So – does your better half care about money as much as you?

This video has been floating around for a while now, but since it’s great Friday material, check out it if you haven’t already – Saturday Night Live – Don’t Buy Stuff You Can’t Afford. “It’s funny ’cause it’s true.”

The Intelligent Asset Allocator (IAA) by William Bernstein does exactly what it says on the cover, it teaches you ‘how to build your portfolio to maximize returns and minimize risk’. However, I would recommend that 95% of readers not buy it. Come again? Instead, I would recommend the later book by the same author, The Four Pillars of Investing (review). Even though Bernstein himself refers to it as for the ‘liberal arts’ audience, I have an engineering background and I still like Four Pillars much, much more. It just feels more refined and easier to follow.

The Intelligent Asset Allocator (IAA) by William Bernstein does exactly what it says on the cover, it teaches you ‘how to build your portfolio to maximize returns and minimize risk’. However, I would recommend that 95% of readers not buy it. Come again? Instead, I would recommend the later book by the same author, The Four Pillars of Investing (review). Even though Bernstein himself refers to it as for the ‘liberal arts’ audience, I have an engineering background and I still like Four Pillars much, much more. It just feels more refined and easier to follow.

Both books seem to cover the same general topics, with IAA giving you a clearer mathematical basis for his conclusions. To me, here are the main ideas within the book:

1) There is very little evidence that, on the whole, actively managed funds outperform the market. In fact, if you just buy what’s been hot the last 5 years, history has shown that you would consistently underperform the S&P 500 afterwards. In other words, don’t chase past performance.

2) As risk increases, so does the return. But that doesn’t mean you should just go out and buy the one riskiest thing you can stomach. Your goal is to get the maximum return out of your acceptable amount of risk.

3) To achieve the goal in #2, you must construct your diversified portfolio out of multiple asset classes which will work in combination to reduce risk. The vast majority of your returns come from your asset allocation mix.

4) You can’t guarantee your future returns, or expect them to follow historical returns exactly. What you can do, is to optimize your portfolio using that data to give you the best chance at achieving the highest returns.

5) Minimize expenses and taxes by choosing no-load index funds with low expense ratios, and by carefully placing each asset where it will be most tax-efficient (taxable vs. tax-deferred accounts).

Finally, in the end, the book gives you some advice on how to choose your specific asset allocation and then implement it using Vanguard or DFA funds. Again, I found the same section in Four Pillars to be easier to follow, and I’ve found myself referring back to it instead of IAA to plan my portfolio.

Summary

Read Four Pillars of Investing first. If you like things like standard deviations and statistics, then pick up The Intelligent Asset Allocator. They are both excellent books, with different approaches to teaching the same material.

Overall Rating:  (ratings explained)

(ratings explained)

Don’t you love how they still claim to have America’s Highest Rate*? My Online Bank Comparison Chart would disagree. Of course, the fine print says “*Highest Nationally Advertised Annual Percentage Yield for unrestricted day of deposit to day of withdrawal savings accounts.” What the #$*% does that even mean?

New accounts can get a $10-$20 Emigrant Direct referral bonus, and my Rate-Chaser Calculator may be useful as well.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)