I recently received a review copy of Jean Chatzky’s The Difference: How Anyone Can Prosper in Even The Toughest Times, where she attempts to understand why some people easily move from barely getting by into a life of comfort and/or wealth, while others get stuck or even fall backwards. What are the attributes that set them apart?

I recently received a review copy of Jean Chatzky’s The Difference: How Anyone Can Prosper in Even The Toughest Times, where she attempts to understand why some people easily move from barely getting by into a life of comfort and/or wealth, while others get stuck or even fall backwards. What are the attributes that set them apart?

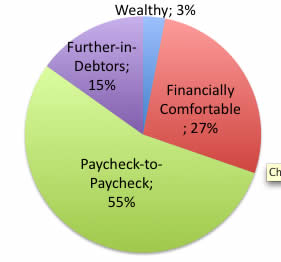

From her research, she divided people into four groups: The wealthy, which have on average assets of $2 million, not including home equity. The financially comfortable, who save regularly and have a financial cushion. The paycheck-to-paycheck, who are getting by but are one unexpected expense away from stumbling into the last group, which are the further-in-debtors. Here’s how the population breaks down:

20 Factors

As you can see, plenty of people are living paycheck-to-paycheck. But what about those who only used to live that way? She found that 75% of the wealthy and nearly 100% of the upper-middle class originally came from middle class backgrounds.

Here are what Chatzky says are the twenty key elements of those people who improved their situations. You don’t need to have them all, but she says that you need, on average, ten factors to make your way to financial comfort.

Financial Attitudes

– feel stocks are worth the risk

– devote money to savings

– save regularly for emergencies

– invest for retirement

– reduced debt

Goals

– want to retire comfortably

– want to be financially comfortable during working years too

– always knew what they wanted to do for a career

– made it a goal to accumulate $1 million

– want to own a home

Personality

– are confident

– happy

– optimistic

– competitive

– leaders

Nonfinancial Behaviors

– have a college degree

– socialize with friends at least once a week

– exercise at least 2-3 times a week

– read newspapers regularly

– are married

Sounds simple enough, eh? I call some of these “duh” factors. The rest of the book tries to explore these factors and ways to actually get yourself to really believe and/or achieve them, since simple doesn’t mean easy. For one, there are many levels of “wanting” – do you have the resolve to make it happen? Or, how is exercise related to wealth?

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

So is it worth reading?

I will respond to the “how is exercise related to wealth?” comment. When you excercise, it makes you feel better about who you are, and a lot more confident. Those that don’t excercise are usually tired most of the time and less motivated. So when you feel good about yourself, you might be more willing to put in the work necessary to reach your goals.

Personally I hate to excercise, but I know the long term benefits for my health and well being. I get more things done than I used to, and feel better about myself too.

I think all of this is true. it is amazing what a difference exercise in particular makes on your general attitude throughout the day.

A friend told me Oprah once said something about exercise 1st thing in the morning being like “Stoking Your Fire”. I am not a fan of hers but I think that analogy is dead on. It works for me!

Also, the married one is important as you can make so much more progress with two incomes and combined expenses. That is, assuming you don’t just waste the extra income of course.

All of these seem pretty easy except for one: “Leaders”

That is a huge personality change, and it is probably the most important item on the list. A leader gets things done and gets promoted. It’s not the only item, but to seek it out is far more difficult than most of us imagine.

Another factor of how excercising increases wealth is less health care expenses.

In my experience, the biggest factor in moving from the pay chk to pay check crowd is to live within your means and abolish all debt. Out of all the four letter words I think DEBT is the worst. Having debt just makes you a slave to the holder of that debt and once you get out from under debt then you can truely start accumulating wealth. I’m doing my best to get out from under my mortgage so instead of giving the bank my money I can give myself my money.

I really think society has gotten harder on people to be savers, it’s not cool to not have a flat screen tv, nice car and fancy clothes and the marketers are spending billions getting you to part with your trillions and they’re able to entice you on many more levels then in the past. In the past, it was acceptable to be frugal now it is frowned upon.

Jean Chatzky gives good financial advice on good morning america. She’s of the most level-headed people that I’ve heard in the field.

However, this book seems like crap. Who cares what the attributes are? If I’m living paycheck to paycheck, should I start reading the newspaper to improve my financial situation?

Nope, I should get out of debt by living below my means.

Quick question – does she assume that a higher income stream will be a bi-product of someone making sure they have at least 10 of these key attribute in play?

This reminds me of the phrase “Correlation does not imply causation”, which is probably true for some of the points. For instance, “exercise” and “reading newspapers” seem to point to the socio-economic background.

I see the major “duh” moments in the goals department. So, it’s less likely to get rich if you don’t want to get rich? Who would have thought.

Personally, I would bet on the personality traits as the key points here. If you are confident and competitive, there is a good chance that this might lead to a higher income.

One thing I wish could be more clear, who exactly is the paycheck-to-paycheck crowd? I have savings (now), and other assets, but if I and my husband were to lose our jobs, in a matter of a year or two,we’d be in big trouble.

We need our jobs to support ourselves, maybe not this particular paycheck, but in general, we couldn’t get by without working. If you really don’t live from your paychecks, then you’d already be rich (or retired), right?

As far as exercise being related to wealth, I would argue that you are more likely to have time to exercise if you are financially stable. It’s the result of being wealthy, not the cause of it. Think about it, if you are a construction worker coming off a tough shift, you’re not going to hit up the stairmaster at the gym. There is a reason that the average triathlete’s salary is 6 figures.

If you are a construction worker coming off a tough shift, you probably get quite a bit of exercise just from doing your job.

If you sit in an office staring at a computer screen all day, it is more important to get to the gym.

@baughman –

you are missing the point. it isnt about reading the paper. that is just something you do. its about what makes you the type of person that does, or what that does for you.

likely, you are trying to stay on top of political and financial news, which may be related to your investments, your business, or other decisions in your life.

it may also be partially the

sounds fairly stupid. you will have more money by not buying this moronic book.

Think about it,you see more thin/in shape wealthy people and more overweight,obese poor people. Exercise is a must for everybody no matter their financial state.

Another backup statement for excercise and wealth, is that excercising takes discipline and motivation. Theese traits have a high coarelation to the traits you’d most likely find in self-made wealthly people.

With that perky sub-title, I think this book is more motivational than truly analytical.

I doubt Chatzky was brave enough to look at the gender and racial breakdowns of her categories. If she had, that non-financial behaviors list would include “be male” and “be white or Asian.”

Include some serious sociology in your book, and then let’s talk about the causation/correlation of personal habits and social mobility.

@Mimi,

I take paycheck-to-paycheck to be the people who don’t have any money left over after they’ve paid their bills for the month, and don’t have anything saved.

Maybe they make $800/month, but their bills/food/everything total $799, so one bad thing happening financially (car breaks down, somebody gets sick, etc) tends to REALLY mess them up.

Now, whether they’re like this because they just don’t make enough money, or whether they’re not disciplined in their spending, who knows.

A couple other good books on this subject are “The millionaire next door” and “The millionaire mind”. Thomas Stanley has done very in-depth research on how differently the wealthy think.

To NY Guy, nail on the head.

To Randy. Some chains are on the body, but most are on the mind. As long as women and people of color think like that they will be oppressed, not by white men, but by their own minds.

I live in an area where a sudden influx of poorly educated Latin Americans has moved in. With no capital and no language skills a surprising number of them have achieved high incomes in a very short period of time.

FWIW there are more wealthy women than men in this country. This is still very much a meritocracy. Just ask Obama.

I only need a wife to complete the set… half joke half serious… any takers? 🙂

It’s a lot harder to be motivated (and in most cases motivation = discipline) when your life is crappy. For someone who lives from paycheck-to-paycheck, they don’t have the ability to spend money on the things they enjoy and make them happy, and probably just end up watching TV/surfing the internet/playing games/cheap socializing in their free time. It’s easier to be motivated consistently when things are going well.

Marriage may be a positive contributing factor but given the failure rate and the financial carnage it often leaves behind the value it brings to this equation may be overstated.

@Ryan… how old are you? 😛

@Sarah: yes, I knew it’s a corny joke which I made because I think the article is a bit corny as well. And I’m old enough to vote and drink in US 🙂

Back to the topic, you see, being wealthy, financially independent or getting by I think is a matter of individual perspective and circumstances. The framework the author sets for dividing classes is somehow BS and too US centric. You can be wealthy with $300k (besides residence value) or getting by with the same amount. It all depends on what you do with the money. It’s also a state of mind. For some people marriage comes early and for others pretty late and I don’t think that’s a factor of how motivated an individual is to feel secure about his finances.

@ DCnTN

That’s a great anecdote–and a spectacularly insulting aphorism–but neither addresses my point.

This book is motivational, not analytical. If you want me to buy your research on the “characteristics” of the upwardly-mobile, then your analysis has to address the systemic disparities in our society. If you don’t, you’re taking such simplistic view of the subject that your results aren’t worth my money.

Women DO earn $0.78 for every dollar earned by men. The median income for a black household IS 60% of that for a white household. These are huge disparities and they’re based on data for the entire nation.

That list of characteristics certainly makes me feel good about myself, but I recognize that it’s just stroking my ego without telling me anything of real value. I want to spend my money on books that teach me something, that expand my understanding, not that reinforce my own self-righteousness.

I’m much more interested in the Buffet bio; at least he has the honesty to admit that random chance played a central role in his success.

Randy I didn’t intend to insult you or anyone else. I apologise if I was insensitive.

Wow, I think I’m already at 16 or 17 (and gunning for 20). Which explains why I’m reading the review in the first place eh? Guess I can skip this one.

Also, I would suggest the ‘papers’ part can be safely detached from the ‘news’ nowadays.

Mimi- I think it’s pretty obvious that you wouldn’t be considered paycheck-to-paycheck. You’re saying you’d be fine for 1-2 yrs if you lost your jobs…that is FAR from being paycheck-to-paycheck.

I think paycheck to paycheck is when missing 2 or 3 paychecks would put you in a deep hole, one you might take several years (or never) to get out of. Even one would put a strain on your finances.

I find it agreeable how she broke down the population into groups; the wealthy, the financially comfortable, the paycheck-to-paycheck, and the further-in-debtors. I also agree that the paycheck-to-paycheck group has the highest number of all, and that those factors mentioned can help someone make his way to financial comfort.

I think what really prevents some of us from getting a comfortable life through our paychecks is the way we live our lives; our lifestyle. We cannot deny that others spend more than what they earn. Spending unwisely and impulsively can lead someone to further-in-debtors group. Who could want that?

Thinking ahead of your future by saving some of your money for your retirement and emergencies and living a simple life are more likely to draw you nearer to financially comfortable group or even to the wealthy group.