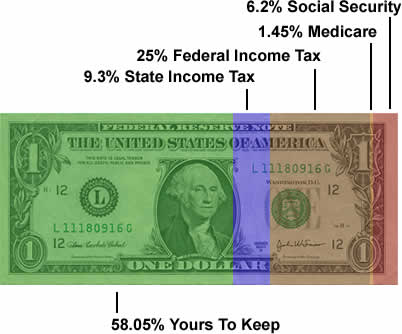

Earn more. Save more. Those are the two ways to get out of debt and build wealth. I’m a big proponent of doing both, but for many people it may be easier to cut back on some luxuries rather than land a higher-paying job, start a side business, or become an investing wizard. It’s also more effective due to marginal tax rates. Let’s say you are single resident of California and your (taxable) gross income is $50,000 a year.

If you were to go out and earn another dollar as an employee, here’s how that additional $1 would get broken down:

You’d only keep 58 cents. On top of that, a lot of extra or freelance work is done as an independent contractor. That means you’re self-employed and get the happy task of paying another 7.65% of payroll taxes (the employer share), which brings your total tax hit to 49.6%! So in order to keep $1 in your pocket, you’d have to get someone to pay you $1.99. In that case, your choice becomes:

This relationship helps me visualize the power of spending less. Now when you save $1, you can feel good knowing that you’d have to have earned $2 of income to equal that. But on the flip side, when I get a check from a side project for $500, I know I’ll only keep $250 of it. 🙁

The Small Print

- This is a specific example, your tax situation may vary. Also note that this isn’t the average tax rate on all your income, but for the next $1 you might earn “at the margin”.

- You might get a portion of your Social Security or Medicare taxes back in the future, even though your taxes aren’t being saved or invested anywhere; it’s being paid out immediately to current retirees.

- Some states don’t have an income tax, but may have higher sales tax or property tax rates to generate that revenue. But remember, a sales tax is basically a tax on income that you spend!

- You’re allowed to deduct half of your self-employment tax from your adjusted gross income, which saves you a bit in taxes.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Your post is right on time. It’s tax time and each year I see (more and more) how much of my second income gets eaten up by taxes.

Vote Republican and you save 2 dollars for every vote…

Wow- this was the perfect article to come across today.

Thanks for explaining the philosophy behind my website so nicely. I’ll have to link to this post.

Assuming you live in an area with a sales tax, that’s an addition 6%-10% so the end result is closer to $0.50 out of that $1.00 that’s yours. So, it really is nearly “$1.00 saved = $2.00 earned”.

Can anyone point me to some more information regarding taxation on freelance work? I’m currently finishing a side project for $8k, and was under the impression that it

would be taxed at my marginal rate. Needless to say, I’m pretty disappointed in hearing that I may only be netting about $4k.

Jonathan, it was so simple argument you explained in easy way. It makes a lot more easier to get richer by not splurging and saving more.

thanks

Just an FYI which will help tweak your numbers a bit, but on Self Employemnt income, the Social Secuirity Tax, the Medicare Tax, the Self Employment tax, and the Federal Income tax percentages only on 92.35% of the extra $1 you earned… (Presumably the state income tax too if they simply carry over the AGI from the federal return) So in actuality the tax load on that $1 is really 45.8%… The math for those interested: 92.35% * (25% + 6.2% + 1.45% + 7.65% + 9.3%)

For those who have the pleasure of filling out schedule SE, the 92.35% number is not a magic number that comes out of thin air… It’s actually the income adjustment to make up for the fact the the employer share of the SS and Medicare tax is not to be considered income. So 100% – the 7.65% SE tax rate gives us the 92.35% number.

And as you pointed out Johnathan, the deduction for 1/2 of the Self employment finished the equation, effectivly reducing your income by the “employer” share of the tax since that is not considered taxable income to the “employee”.

BTW, adjusting for the 92.35%, for a self employed person to actually be able to take home $1 in the scenario you presented, they need to be paid $1.85.

Hi,

I am single and is paying taxes through my nose. I don’t mind paying taxes if I know they are being put to good uses. But they are NOT. I want my dollars to go toward health care and not the war. I want my dollars to building good education systems and not governmental waste.

If our government is using our dollars effectively, I don’t mind spending more to keep the economy going and work more to be a productive member of our society.

Then you have other taxes for your car, property, sales, etc.

Nice and concise description. That’s exactly the correct tax breakdown for me living in CA, yikes!

Saving is extremely powerful and can help a family or an individual a huge amount going forward. Why the savings rate in America is so low is confusing to me, and its

also quite concerning.

I wholeheartedly agree with this post. For the majority of us controlling costs, not revenue, is the biggest problem. Only the impoverished have the comfort of always blaming their incomes.

I definitely agree with you about saving v. earning. Something else that’s important is that you only have so much time and energy. That extra dollar doesn’t only cost all that in taxes but it also costs you time and energy that you could have spent doing something else. It’s generally easier to prevent money from going out the door than to get more money in.

I hate income taxes with a passion.

wow, great visual, explain very clear. great job. keep it up. thanks.

You have some good points with this post. The key is finding ways to keep more money in your pocket over the long haul… so many people what their money now instead of planning for ways to have money now but even more later.

Although I don’t disagree with the analogy in the post, I find its logic is somewhat over-simplified. There’s nothing wrong to advocate “live with in means” and “save as much as possible” principles. However, if you suggest trying to make more money (maximize one’s earning potential) is somehow less effective/efficient than just try to save as much as you can on your current earnings, then this assumption is flawed. There are too many variables that will make the situation a lot harder to judge. Judging by the comments follows, I sense that many people are saying “it’s simply not worth it to work harder and smarter because you make less than what it appeared on paper.”

That may be true when a 20-something-single-guy is making $50k a year and is trying to do some side works by making another $10k per year. But what if his side works took off and he eventually has to quite his $50k day job and try to make that small business a much bigger success story? What if that small business is going to earn him $200-$300k/year or even millions in just few more years? Then the whole equation will change. Whether this young man ever limited his expense and maximized all his IRA/401k became completely irrelevant to his “American dream” equation. Don’t tell me this is a dream and it’s unreal. I see it happens everyday and frankly, Republican or Democrat aside, this is what makes America great in the first place.

Even if you just want to concentrate on your “savings”, you would still need to invest tremendous amount of time and efforts to refine your investment skills. The earning of “deposit and forget” strategy generally give you a slightly-above-inflation which will almost certainly not to get you ahead, but merely keeps you from fallen behind.

So the advice above may seem wise but it could be a penny wise (or two penny wise?) statement after all.

yeah i’m sure you would all be richer if your neighborhoods privatized everything , and hired everyone yourselves, that’s why govt work pays so much LOL give me a break, you all cry about taxes and need to realize how convenient everything is.. and top of all that some of you even get tax returns.. i’m sure you all would be so shocked to see the prices of everything if taxes did not exist.. i’m sure no one would raise prices dramatically on everything in existence to match the money in people pockets..look at rich areas.. every thing cost way way more in those areas

You forgot to add another 2% property tax on avg price of home being in the 600-800M range to the cost of TAX in CA. 🙁

Jonathon –

I’m really disappointed in your graphic. You have stooped to the level of the sound byte.

The graphic is COMPLETELY misleading and a GROSS exaggeration. Yes, you explain better in the footnote that the tax is on the “next dollar”. Even with note, the graphic is STILL wrong because SSI stops at some point.

The federal tax income for that individual making 50k taking the standard deduction is only 15.2%.

The same goes for state income tax, depending on your state.

You should come up with an accurate graphic. People on this blog look up to you. No need to mislead them.

-Wes

Ouch. That blue chunk (blue state premium) hurts.

If you save and put your money in a stardard CD, the bank will give you 5%, you then pay 1- 2% of that to taxes, bringing your interest rate to 3%. Inflation is probably closer to 6-7% in this country, so you lose 3-4% each year. Yes savings is good, debt is bad, but unfortunately we are in a weird situation in this country where no one saves, so the minority that do save actually lose value each and every day on their savings. Its really not that simple, if you saved and saved to pay cash for your home you will probably save till you die. Prices are rising faster than anyone can save. Taxes on employed individuals is extremely high. Fica should be illegal.

It always surprises me when you really see how much we pay in taxes. I wonder how long the IRS would last if we had to write a check to them each month instead of having it taken out of our payroll. Taxes are by far our largest expense.

Wes, without thinking of accuracy, I was going to say I loved how easy to understand the graphic was. Hmmmm…can we simply update the figures on the graphic but leave the graphic as is. I think it’s great! Loved this post because of the graphic!

_N

Guilty as charged in trying keeping it simple. So instead of gross income, replace that with *taxable* gross income. Or *adjusted* gross income (AGI). Or just change the person’s income to $60,000. I think the idea remains the same.

Check it out. For 2007, the 25% marginal rate apples to taxable income from $31,851-$77,100. The low range is a lot less than $50,000. I just chose $50k to be in the middle.

Federal Income Tax – Marginal Rates 2007

SS does stop at over $100,000, but I would say that is a far ways off from $50 or $60k. Also, as you get that high your other marginal rates will got up. Do I want to re-calculate again? No, still trying to keep it simple.

Main idea remains these same: It takes significantly more than $1 earned (more than double for some, less than double for others) to replace $1 saved. 🙂

Nicolas needs to read up on some basic economics. So what he is saying that paying all that tax is good because if we did not then prices would go up?

I paid $8k to the Feds in income tax, SS, and medicare last year. How is that good? I can’t believe people are this dumb, but Jay Leno’s Jaywalking and Nicolas says otherwise.

I can only imagine how much cheaper everything would be if we abolished as many taxes as possible. Income taxes, employment taxes, property taxes.

There is only one candidate in presidential race that has the record on income taxes (hint: he is a congressman from Texas and believes in following the US Constitution and wants to abolish the IRS). Naturally, a candidate of this caliber recieves poor main stream media coverage.

Draw your own conclusion.

Abolish the IRS? What point would that serve? The government still needs to be financed which means there still needs to be a tax collector.

Overall, don’t we have one of the lowest effective tax rates for the average Joe for a non-OPEC country? So quit your whining!

(some references:

http://en.wikipedia.org/wiki/Image:Income_Taxes_By_Country.svg

http://www.worldwide-tax.com/index.asp#partthree)

Do you really want LESS in social services, defense, environmental, energy, education spending than we have NOW???? Aren’t we ALREADY out of the top 10 globally in education, mortality, infant mortality, envriroment, energy, and overall “happiness”.

Let’s see if we can get to 3rd world levels in EVERYTHING except for defense!

-Wes

This is a GREAT post! This is why I am a HUGE advocate of spending your money on paper BEFORE you ever receive it. It allows you to choose the best places to spend your money and provides options to reduce your expenses!

When I started using a cash envelope for groceries, I saved $200 PER MONTH! That was like a $325 – $400/month pay raise!!!

Well explained. A picture says a thousand words.

Thanks

“Do you really want LESS in social services, defense, environmental, energy, education spending than we have NOW???? Aren’t we ALREADY out of the top 10 globally in education, mortality, infant mortality, envriroment, energy, and overall “happiness”.”

Yes, I truly believe in NO government social services. Definitely NONE at the Federal Level. I see no basis for Dept of Education or Dept of Housing that give free houses to former drug users or subsidizes housing when I’m told I make too much money to receive the same treatment.

States have more than adequate environmental oversite and paymore than enough for education. Why pay twice for the alleged “service”? Why must I pay for others education and taxed at the local, state, and federal level for this alleged “service”. This country spends the most per child for “education”. And the kids are still stupid!!!!

If we cut the Feds down to CONSTITUTIONAL functions, the Feds loot plenty from gasoline taxes, tariffs, and other fees. Remember, this is the same government that does not know what happened to $400 billion for TSA, the billions in Iraq, loses track of multimillion dollar equipment every day. This is government that has abusive IRS that runs over 4th Amendment rights if I make even an honest mistake on taxes but does not hold itself to same principles.

That $8k does not include my other taxes my check like property taxes, sales tax, gasoline tax, tax on phone. That is at least another $3k per year. Never mind the burdens of minimum wage and other nonsensical government licenses and regulation that with taxes probably consume 50% of everyone’s gross pay each year.

I would never volunteer my time or my left over income to any social charities since government already does all that via taxes.

As for defense, this is a legitamate fed function, but one that has also failed us. I’m not sure how 700 plus military bases is good “defense” along with 12 aircraft carrier fleets.

Jonathan,

I just stumbled across your blog and I’ve really enjoyed reading through it. I started a similar project last month with the idea of tracking my own progress to financial freedom. It’s nice to see someone who has been doing it for a little while and making great progress.

I plan on spending a little time reading some of the older posts from when you just got started. I think that the thought processes succesfsful people have at the beginning of your journey can be very insightful and helpful to those starting out.

Congratulations on how far you’ve come!

Jonathan, this post rocks. I’ve understood this concept for a while now, but haven’t been able to convey it as well as you did here. Great work.

To K man: Hmm, vote Republican, earn $2, and hate myself ’cause I don’t agree with any of their views. No thanks.

Great article, it really breaks everything down simply. I think most people understand it’s illustrative and not completely indicative of their situation–but does represent the spirit of it.

I think you’re making it more complicated than it is. Let’s say you need surgery tomorrow and it costs $500. You can either (1) spend your existing money, (2) create $500 by cutting $500 in existing costs or (3) go out and make an additional $1,000. You can’t convert one back to another, but the result is the same.

“I could save the equivalent of 2 PTDs, but when I spend I only get to spend 1 SD.” Exactly.

I’m not so sure about this concept. I’ve been trying to come up with a way to explain my misgivings, and this is the best I could come up with:

Let’s start with the idea that everybody has to pay taxes — even on a 401k, they’re just deferred. If you have a dollar that hasn’t been taxed, you’ll owe taxes on it. If you have a dollar that’s already been taxed (two pre-tax dollars, as you say), you don’t.

So, let’s consider these as two different currencies, or types of dollars. You have pre-tax dollars (PTD) and super dollars (SD). An SD has a note attached from the IRS that says “I’ve already been taxed”.

You can have a bank account for SDs and one from PTDs (retirement accounts), but they’re kept separate. If you try to transfer from PTDs to SDs, you’ll pay a tax. You can’t spend PTDs anywhere — nobody accepts them. And, importantly, you can’t go backwards — from SDs to PTDs — as you’ve already paid the tax (see next para). The exchange rate is about 2 PTDs to 1 SD.

So, let’s look at the platitude again, “A super dollar saved is two pre-tax dollars earned.” Sure, that makes perfect sense. However, it’s completely irrelevant. I could save the equivalent of 2 PTDs, but when I spend I only get to spend 1 SD. Theoretically, I could not spend the SD and put it into an IRA. The statement they send me says I’ve deposited 2 PTDs. However, when I withdraw (at 30 years old or 70 years old), I have to pay taxes and convert to Super Dollars.

Another analogy, though probably more complicated for some to grasp, is food. Consider the fact that just the act of chewing and digesting uses up 15% of the calories in food (I’ve heard). And consider someone who desires as many calories as possible. You’ve just hunted and killed 1000 calories worth of rabbit. Short of biomechanically injecting those calories into your system, you’re not going to get them. So, you eat 1000 calories and you only “get to use” 850. I could say that 850 calories saved is 1000 calories hunted. But that’s irrelevant because I’ll have to eat the 1000 calories at some point, and I’ll only get 850.

Or, as the age-old saying goes, “A bird in hand is worth two in the bush.”

Great post, thanks for the graphic too!

The inflation rate is misleading. It’s based on the assumption that you would replace every single thing you own every year. How many of you actually do that? Not me. It’d be idiotic and wasteful on so many levels. And if you think about it, a lot of things that were supposed to go up in price have actually gone down. Technological devices are the best example of this; we’re all on computers here, and we’ve all watched their prices drop. The laptop I’m using right now was bought new for less than five hundred dollars; five years ago it would have cost at least three times that much.

Housing prices also rise and fall depending on the market and the area of the country. A house that would have cost you $100,000 three years ago may go for $80,000 this year.

So it’s foolish to say that you can’t save money because you don’t make enough to keep up with inflation. That’s just an excuse for irresponsibility. It never ceases to amaze me how many people would rather play the stock market or gamble in some other way when if they just stuck the money in a bank account or a CD they would be guaranteed to hold on to it, and they would have it for a rainy day. Appreciate what you have.

As for the tax discussion… that’s a whole ‘nother ball of wax. I LIKE living in a first-world nation, with all the amenities thereof. I’m willing to pay for it, when my income’s high enough that the government wants any of it. For those of you who don’t think you’re seeing any of your tax money back, remember that the next time you take a road trip or drink water or breathe air. We all benefit, believe it or not.

I was trying to explain this the other day – you do it so much better, thanks!

While your example uses the American tax system, the principle that it is easier to save a dollar than to make a dollar would seem to be universal. I’m an Australian gov. public servant. I don’t get overtime, so the only way I can make extra money is to work a second job. That probably means extra transport costs, or home office costs. The high cost of child care services means that if I had kids I’d think twice before agreeing that me and the wife should both work (at the same time). There are more practical ways to save. Do you buy coffee every day? Do you buy lunch? I figure I spend $14 minimum on those two things every day. All I have to do to save is take my own lunch.

Great article with some fantastic food for thought believe me I need some really good ideas and fast (like yesterday!) Now I have a starting block Thanks for all your help

An oldie but goodie, refreshed!

Just move out of California to Washington or Nevada and save a heck of a lot more!

not sure how I missed this one the first time around…. Still makes me wish Ron Paul got the nod. =(

Yes, this is most compelling when you look at it this way. Great post.

I’d agree with James that this post contains a bit of a fallacy. Unfortunately I’m not sure I can explain it any better than James did.

You state that saving 1 post-tax dollar equals earning 2 pre-tax dollars (and so saving is more “effective”).

But, you could restate this as “saving 1 post-tax dollar equals earning 1 post-tax dollar” or “saving 2 pre-tax dollars equals earning 2 pre-tax dollars.”

Forgive me if you intended this simply as some sort of motivation tool to “trick” yourself into saving more.

I’m not sure I follow. How do you save a pre-tax dollar? If I want a dollar bill, I have to earn two dollars of income. Two dollars has to transfer from one entity to another, due to the friction of taxes. Or I could just keep a dollar bill from leaving my pocket.

While it is admittedly an oversimplification, the point is exactly right.

You need to earn way more than $1 to make the same financial impact as saving $1.

For example, if I could convince someone to carpool with me, that would save me 175 miles a week and thousands of dollars a year.

The amount of money I would have to earn produce the same positive financial result is vastly greater than that once you figure in all the taxes.

And how did you get that dollar bill in your pocket in the first place? It was also two dollars that had to transfer from one entity to another.

I think perhaps your argument is that getting the next dollar is harder than it was to get the one you already have. The question then is whether getting that next dollar is easier/harder than cutting expenses by (i.e. saving) a dollar–which is something that simply depends on one’s circumstances.

Calling that calculation $2 vs. $1 is simply false–otherwise anyone with a brain would have stopped after making their first dollar =)

Yes, the whole idea is that we’re talking about marginal dollars here.

Stated another way: I think perhaps your argument is that getting the next dollar is harder than it was to get the one you already have. But surely getting the next dollar is rarely TWICE as hard as it was to get the one you just earned.

I think what we’re both saying seems obvious to the other person. You’re saying in every dollar in my pocket was taxed as well to get there. I’m saying that to get the *next* $1 in my pocket, I have to earn $2 from you or someone else. Same thing, really, with the added wrinkle of progressive tax rates. But, I have the option of not earning an additional dollar, which will never get taxed. I don’t call it pre-tax or post-tax, because that’s just a matter of perpective.

Let’s assume the marginal tax rate is 50%. Let’s say you have a dollar and I have a dollar. If I pay you the dollar to cut my lawn, then you have 50 cents. I’m out a dollar, you’re up 50 cents, 50 cents went to taxes. What’s pre-tax and what’s post-tax depends on which person you are, but in the end there was a loss due to friction. What if I cut my own lawn. No friction. Let’s avoid the friction.

What if the friction (tax rate) was 99% on every dollar you earned over $50k? Then there would be a lot of friction to avoid. Wouldn’t you focus on living within that $50k as opposed to earning more, if you already earned 50k?

STFU DS. Earning the next dollar is more than TWICE as hard. Otherwise you would have been making more money and rent some brain.

DS – I don’t think John is saying anything about how hard it is to save or earn a dollar, just that you shouldn’t consider that dollar as being worth the same in both cases. The point is that saving money is equivalent to earning the same amount post-taxes, but often when we think of earnings we focus on the pre-tax amount. So if you really want an extra $1, you either don’t spend $1 elsewhere, or you spend your $1 then earn $2 pre-tax which will be $1 when it gets to your pocket. There’s no judgement about which one a person SHOULD do (as John wrote, “I’m a big proponent of doing both…”).

In some cases, it will be easier to earn the next $2 than to save another $1, for example if you’ve already completely cut your spending down to essentials, or if offered a promotion that comes with little extra work but a nice raise.

I did not read the whole comments string – just read the lately posted arguments.

I noted the dollar bill did not show the DSI imposed on wages earned in California. Does it mean that many other states do not have DSI (to me, DSI is a tax, not an option)? If there is a mandatory DSI, the post-tax dollar bill should shrink further to a smaller size.

Also, when we take into account the “California Sales and Use Tax”, Oh, my dollar bill shrinks further. In summer 2010, I revisited the state of Maine and did some shopping near Portland, Maine. I was asked the sales tax rate in my living area. The return comment was similar to this, “How could The State of California have budget problems when it imposes 10% sales tax?” In Maine, sales tax rate was 5% in Summer 2010 (I did not recall the sales tax rate in Maine around Summer 2007). In Summer 2010, sales tax rate was 9.75% in the greater Los Angeles area, whereas it was 10.75% in the cities of El Monte and Pico Rivera.

As David says, we could move out of California and live in Washington where impose no income tax. I would say that we could then go shopping in Oregon or Montana where impose no sales tax.