There are plenty of “FAKE-O” credit scores out there, but the only place to get your real FICO score is myFICO.com. Problem is, usually these cost money and even if they are free due to some promotion, it’s during some random time of the year. If you want a free FICO Score on demand, you’ll have to agree to a free 10-day trial at MyFICO.com:

IMPORTANT INFORMATION: When you order your free FICO Score here, you will begin your 10-day trial membership in Score Watch®. If you don’t cancel your membership within the 10-day trial period, you will be billed $12.95 for each month that you continue your membership. You may cancel your trial membership anytime within the trial period without charge.

Pain in the rear, right? Well, not really. Two things make this a 5-minute operation:

- If you do not want the monitoring that ScoreWatch provides, then you can cancel immediately after you get your free credit score. Don’t wait a day. Don’t even wait an hour. This way you won’t give yourself a chance to forget.

- You can cancel with just a few clicks. 100% online, no phone calls, with no hassle. You don’t have be subject to a hard sell or argue with anyone.

Here’s how I did last week. First, when you go through the process to buy your free score with trial, you will have to provide your credit card information but nothing should be charged.

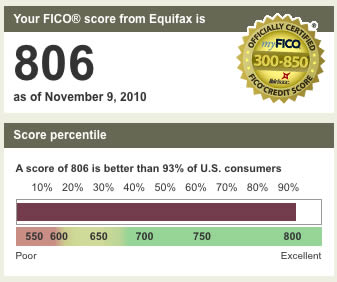

After that, you should receive your credit score and the related Equifax credit report. Print it out. You’re going to cancel right afterward so you won’t have access to the information anymore. Print – or at least print/save to PDF – anything you want to keep. This was the first time I’ve ever seen a score above 800!

Now, don’t go anywhere. To cancel, click on Support on the top right of the page, then Contact Us by email. Choose “I would like to cancel my product subscription” and for the product mark “Score Watch® – Free Trial”. Here is a screenshot of what it should look like. Finally, type in your personal information and submit. There is a blank for the order number, but it is not required. I didn’t bother to fill in anything optional, and my cancellation still worked fine.

myFICO should e-mail you back in about 24 hours. It took 25 hours for me. Here is the response you should get. The title of the e-mail was “Score Watch(R) Cancellation”:

Your order for Score Watch® (monthly payment option) has been cancelled. You will not be charged in the future for this product.

If you have any questions, please call myFICO Customer Support at 1-800-319-4433, Monday – Friday 6:00 AM – 6:00PM (Pacific Time) or Saturday 7:00AM – 4:00PM (Pacific Time).

Thank you,

myFICO Customer Support

That’s it, a free credit report and score with minimal hassle direct from MyFICO.com. Remember, when you request your own report, it doesn’t affect your credit score at all.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work){kind=link}

Thanks! I was considering the free trail, but didn’t want to go through the cancellation process if it can only be done by phone. The online cancellation really helps a lot, so I got mine, but it isn’t 800 yet 🙁

Thanks for the step-by-step. Obtaining your credit report in this way doesn’t ding you for a credit inquiry, does it?

I wonder if it is this easy to obtain scores from the other credit bureaus (Transunion and Experian).

Thanks for the steps! Beat you by 2 pts 🙂

Thank you very much for the steps!

Thanks for the heads up. I was always reluctant bc I hated to have to call in to cancel but now that it’s online, I guess I have no excuses.

796!!!

@Andy – I believe you do get dinged a few points for the inquiry. It doesn’t matter whether the inquiring entity is another financial institution, or you.

@Andy – Inquiries on your own credit report never affect your credit score. (Why would it? You are not seeking credit.) You can check it a hundred times a day if you wanted to. From myFICO:

“Check your own credit reports regularly, before applying for new credit, to be sure they are accurate and up-to-date. As long as you order your credit reports through an organization authorized to provide credit reports to consumers, such as myFICO, your own inquiries will not affect your FICO score.”

@KP – Ha! I was surprised it was over 800.

@Jon – That only applies if you don’t cancel your free trial. As long as you cancel, it’s still free.

Excellent, thanks.

I got an 801. : )

“I agree to be billed 10 days from now at $12.95 per month if I do not cancel my no obligation 10-day free trial. A three month minimum subscription applies”

I wonder if the 3 month thing matters?

Wow, you guys are all-stars. I got 736.

If I do this now, will I be able to do it again in the future or is this for new customers only?

Thanks for the heads-up! My 786 seems so paltry to your 806…

@Justin

Did this last year too, and I just did it again using the same login info. They don’t seem to mind…

I got a 739 by the way. I’m 23 and my short credit history seems to be the only thing hurting me. Still pretty happy with that score though 😉

Just told my little cousin to do this. She’s turning 21 and her score is 752. I guess she has me to thank for the good credit-building advice 😉

I checked my credit report and I noticed that I have duplicate entries (same date) of credit inquiries from AT&T and C Schwab. The inquiry is valid, but does the duplicate have a detrimental affect on my credit score? The credit report mentioned the number of recent inquiries is negatively affecting my score and it seems to count the duplicates too. Should I contact the credit reporting agencies about this?

792

I been using CreditKarma for last year or so and checking my scores without any hassle. May be it is not your good list but it avoids the cancelling and onetime hassle. I also get my credit score from my credit union. Some credit unions nowdays are offering free credit scores too. So these ways helps to be on top of your creditscore but free ones are always good too.

My score was around 802 but recently gone down to 756 because of new credit card and hope to get it back up.

Justin: I did the free score thing two months ago and it wouldn’t let me do it a second time.

That said, I am now doing three months of ScoreWatch as I’m working through paying off credit cards/refinancing a mortgage and in my situation, I’m finding it worth the money. They also have a pretty clever “score simulator” feature.

Discount code: FICO25 for 25% off any of their products, so the ScoreWatch is about $10/month with that.

The link doesn’t seem to be working.

763 for me. Got my first credit card just before I graduated high school, but I guess 7 years of history isn’t long enough yet, but I’ll still take 750+… not bad. Plus that AA visa card I just opened to get 75k miles isn’t helping either… I can take a little credit hit for 3 free domestic rt flights

The link seems to be working again, my FICO was 786, my Credit Karma has been at 769 for a long time for a difference of 17 points.

I would like to get above 800:

I have had credit since I was 7 years old (got on to the parent’s credit card and inherited their credit history), but I could still have a longer credit history.

I opened a new account 15 months ago, FICO says I need to wait 27 months for the best credit score.

I have pretty high utilization on my company Amex, I just asked my other credit card companies to increase limits so that I can offset that.

I guess I just need to continue to pay on time and just wait, I don’t think there is anything I can actively do to improve me score.

-Jared

Thanks Jonathan. I’ve got score of 753. Is that good?

776 on Fico, Credit Karma shows 780.

764. I only have about 4years of credit history. It took years after being in the country before capital one offered me a credit card. I also just cancelled an amex account macy’s opened in my name. apparently, they’re done with visa and switching their customers to amex. either way i’m satisfied.

I took an indepth look and it says my length of credit history is “not good”. I guess that’s what’s hurting me. I’m still young.

Is 776 really the median credit score of the readership of this blog? I suppose those that had lower scores were less likely to post them, but still, wow!

People comparing CreditKarma to the FICO score from this should realize that the sources are different. CreditKarma uses TransUnion; FICO is giving you a score from Equifax.

Check CreditSesame for Experian-based score.

Thanks Jamie,

FICO 786

Credit Karma 769

Credit Sesame 784

-Jared

Is there any limit to the number of times you may sign up for and then cancel the service?

It appears that you can only enjoy the free trial once every 24 months. I just tried signing up using my previous login information and was informed of that limit. I did not try to create another login though, since I think they can place the same limit per SSN.

Unfortunately, I know all these messages were done in 2011 but as of 5/8/12 they have taken the “I would like to cancel my subscription” button off. So this no longer works and you have to call….for anyone who is looking to try, please know you must call now!

Thanks for the update Lane! Makes it less convenient that’s for sure.

You can still just send them an email using the online form– there’s a pull-down for “I want to cancel my free trial”. I just did it, it was painless.

I just did this, and while there are buttons just like described in the original post, after two clicks it takes me to a screen telling me to call the myFICO customer service number to continue. I called, and it was fast and easy to cancel by phone.

FYI The cancellation process required a phone call and the very first question was what is my SSN.

They said the website was having an issue but considering that on the website and during the phone call I was offered the “discount” of $10 / month I suspect it’s a “hard sell” business model.

Not entirely comfortable having this kind of company monitoring my info.

My boyfriend and I each just went through the process (7/30/12), got our FICO scores and history information, immediately went to the “support” and “email” and the “I would like to cancel my product subscription” option WAS there, and it was simple and fast, following the instructions above. We both received cancellation emails, and seems like it worked well and we didn’t have to pay for it at all. Thanks for the info!

TRICKS NOW!!!

YOU HAVE TO CALL TO CANCEL!!! No longer can you do it by email!!!

I HATE THEM!!!

You will be on hold forever…..forever…..FOREVER!!!!!!!!!!!!!!!!!!! And then they will try to sell it for cheaper over and over and over!!!!!!!!!!

Report them to the FTC!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

Mark is right… I’ve been on hold for 40 minutes now and they claim a 5-10 minute wait at the beginning of the call. This is TERRIBLE. I wish they would bring back the e-mail option. I guess this is their way of nailing you into a contract that you’re stuck with.

Could the author please add an update to the top of the article mentioning the info is no longer correct, and that you have to call to cancel now. I didn’t read all the comments first, and now I’m very annoyed.

You can still cancel online. The website even tells you how to do it on your account. It cancels immediately. I was able to cancel mine just now online without giving any personal information.

I just did this and could not cancel online, however I called and my call was answered right away. I just insisted I knew what they were offering and did not want to pay for anything else. She cancelled my subscription and the call took about 5 minutes.

Just cancelled my online subscription via telephone and it took a total of 7 min and 11 seconds. I was on hold for 6 of those minutes. I think the key is to call as soon as they open. I called at 8:05am central time. The lady assisting my cancellation offered a $9.95 monthly discounted rate, but I respectfully declined. It was a quick and simple cancellation process, although the site should be upfront about having to actually call to cancel. The website leads you to believe that it is as simple as making a few clicks on their site.

Extremely hard to cancel. Customer service is subpar.. had to wait almost 30 minutes and then supervisor kept mentioned the 3 month subscription in a rude manner. I missed cancellation of trial by a few days due to personal reasons, asked them to keep 1 month, but cancel the other 2 and was rudely declined.

Overall horrible business practice. They just try to force you on a 3 month sub and this is why cancelling through webpage or email was removed. I will NEVER try this site again nor recommend it to anyone (will talk bad about it anytime someone asks me..).

You can no longer cancel on-line – I did the 10 day trial and have spent over 10 minutes waiting on hold for someone to answer. I only signed up because this article said it was easy to cancel – it should really be changed to reflect the current reality. If only I’d read the comments.

The option to cancel subscription is still there. What’s everyone talking about it not being there? I haven’t cancelled yet but I see the cancel subscription there.