Updated April 2018 with custom ETF allocations. Betterment is an independent hybrid digital/human advisor that will manage a diversified mix of low-cost index funds and help you decide how much you’ll need to save for retirement. (By independent, I mean that they are not tied to a specific brand of funds like Vanguard or Schwab). Betterment is also an RIA, which means they have a legal fiduciary duty to keep client interests first. They frequently announce new features and improvements, so I will work to keep this feature list updated.

Updated April 2018 with custom ETF allocations. Betterment is an independent hybrid digital/human advisor that will manage a diversified mix of low-cost index funds and help you decide how much you’ll need to save for retirement. (By independent, I mean that they are not tied to a specific brand of funds like Vanguard or Schwab). Betterment is also an RIA, which means they have a legal fiduciary duty to keep client interests first. They frequently announce new features and improvements, so I will work to keep this feature list updated.

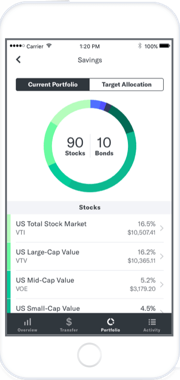

Diversified portfolio of high-quality, low-cost ETFs. Their portfolios are a diversified mix of several asset classes including: US Total, US Large Value, US Mid Value, US Small Value, International Developed, Emerging Markets, US Corporate Bonds, US Total Bond, Inflation-Protected Treasuries, Muni Bonds, International Bonds, and Emerging Market Bonds. For the most part, Vanguard and iShares ETFs are used.

The traditional Betterment portfolio has a more pronounced tilt towards the size premium and value premium than the cap-weighted indexes. You could argue the finer points of whether this will really create higher risk-adjusted returns, but overall it is backed by academic research. Betterment has also added a Socially Responsible Investing (SRI) portfolio option.

In April 2018, Betterment added Flexible Portfolios which lets you manually adjust the percentages of each asset class. As a DIY investor with assets spread across multiple accounts, this customization has been something I’ve been waiting for. This option is currently available only to clients with $100,000+ in assets.

Both the SRI and Flexible Portfolio options will work with Tax Loss Harvesting and Tax Coordination features (see below).

Free access to human advice for everyone. In July 2017, Betterment announced that all of their customers can message a licensed financial experts. Digital members (0.25% annual fee) can ask questions any time via their mobile app. Digital members should expect an answer in approximately one business day. Betterment Premium members (0.40% annual fee) have unlimited e-mail and direct phone access to “Certified Financial Planner professionals”. From their press release:

Our experts can assist with deciding which funds to move to Betterment, setting goals (like saving for college, a house, or retirement), and identifying which Betterment tax features may be right. They can also help you make important investment decisions, like choosing risk levels, amounts to invest, and types of accounts.

Reading between the lines, Digital members get “licensed financial experts” while Premium members get “Certified Financial Planner professionals”. This suggests that while Digital members will still get fiduciary (client-first) advice, Premium members will get priority access to the more-experienced advisors in exchange for paying their higher fee.

Retirement planning software with external account balances. RetireGuide is Betterment’s retirement planning software, first launched in April 2015. This service links your external accounts from other banks, brokerages, and 401k plans (similar to Mint and Personal Capital) in order to see your balances without having to manually input them. According to their methodology guide [pdf], they don’t analyze your transactions to estimate savings rate, they are just pulling in balances.

Example questions: How much do I have invested elsewhere? Am I saving enough money? How much estimated income will I have in retirement? Your future Social Security income is estimated for your based on your chosen retirement age and birthdate. You can change many of the variables as you like.

Account types. Betterment now supports taxable joint accounts, trust accounts, 401k rollovers, Traditional IRAs, Roth IRAs, SEP IRAs, and Inherited IRAs.

Tax-efficent asset location. Tax-Coordinated Portfolio will place different asset classes in your taxable accounts vs. tax-deferred accounts (IRAs, 401ks) for a higher after-tax return. In addition, if you have multiple types of accounts at Betterment (i.e. both IRA and taxable), it will manage multiple accounts as a single portfolio, placing assets that are taxed more into more favorably taxed accounts (like IRAs). Note that this only works across accounts that are held at Betterment. It does not adjust for non-Betterment accounts. This is called their Tax-Coordinated Portfolio (TCP).

Use dividends and new contributions to rebalance. They will use your dividends and new contributions to rebalance your asset classes in order to minimize sells and thus minimize capital gains.

Daily tax-loss harvesting. Betterment’s Tax-loss Harvesting+ (TLH+) software monitors your holdings daily and attempts to find opportunities to harvest tax losses by switching between “similar but not substantially identical” ETFs. If you can delay paying taxes and reinvest them, this can result in a greater after-tax return. The exact “tax alpha” of this practice depends on multiple factors like portfolio size and tax brackets. You can read the Betterment side of things in their whitepaper. Here is an outside viewpoint arguing for more conservative estimates.

My opinion is that there is long-term value in tax-loss harvesting and especially daily monitoring to capture more losses. However, I also think it’s wise to use a conservative assumption as to the size of that value. (DIY investors can perform their own tax-loss harvesting as well on a less-frequent basis. I do it myself, but it’s rather tedious and I’m definitely not doing it more often than once a year. I would gladly leave it to the bots if it was cheap enough.)

Invest your excess cash automatically. Automatic contributions are good, but perhaps you don’t want to commit to a set amount each month. (Ideally, you do commit to a set amount, and this service invests more money on top of that.) Called SmartDeposit, you link your checking account and choose your Checking Account Ceiling and Max Deposit amount. If your checking account balance goes above the ceiling, Betterment will automatically sweep over money and invest it for you. Betterment will account for future scheduled deposits so you don’t over-contribute.

Fee schedule. Betterment has a fee structure with two tiers.

- Betterment Digital. No minimum balance. Digital portfolio management and guidance. Unlimited access to “licensed financial experts” via mobile app with ~1 business day turnaround time. Flat fee of 0.25% of assets annually. The management fee on any assets over $2 million is waived.

- Betterment Premium. $100,000 minimum balance. Digital portfolio management and guidance. Unlimited access to “CFP professionals” financial experts” via e-mail or phone. Includes more in-depth advice on investments outside of Betterment. Flat fee of 0.40% of assets annually. The management fee on any assets over $2 million is waived.

In my opinion, the main concern of any outside advisor is the same: you are handing over control to someone else. Betterment could change their investment philosophy, their pricing structure, and feature set in the future. Digital advisors are constantly changing, and some of their new features could be great or it could just be a fad.

Bottom line. Betterment is an independent digital advisory firm with nearly $10 billion in assets, which means they aren’t tied to any specific brand of funds like Vanguard, Fidelity, or Schwab. Their main differentiators from the other independent firms (see my Wealthfront review) are (1) access to human advice available to all customers and now (2) the ability to customize your target asset allocation ($100k+ in assets). Other notable features include: Retirement planning software that syncs with external accounts, tax-loss harvesting, tax-coordinated portfolios (when you have both IRA/401k and taxable at Betterment), and SmartDeposit which automatically invests excess cash from your checking account.

The Best Credit Card Bonus Offers – May 2024

The Best Credit Card Bonus Offers – May 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - May 2024

Best Interest Rates on Cash - May 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Great article. I am a big fan of betterment. They keep innovating at a fast pace.

Isn’t their premium service .40% not .025% as mentioned in your article.

Thanks, fixed.

What makes you think that the “licensed financial professional” is required to be a fiduciary?

Betterment is an RIA, so they are legally required to act as a fiduciary.

Is there an offer code to get one year free?