Update February 2024: Save now provides a link to their actual returns for their 1-year Market Savings across all portfolios. But be careful, as much of what is shown at first glance is for products that haven’t actually completed their entire terms. You need to scroll all the way left to find numbers for products that have reached maturity and actually paid out any returns. For example, starting December 2022 and ending December 2023, or January 2023 through January 2024. Screenshot taken 2/29/24.

Update January 2024: I have updated this review with my final return numbers, along with additional details from my bank and brokerage statements. I really wish it were different, but unfortunately my experience was not unique. I have gotten a lot of messages from people who are unhappy that they received a 0% actual return on their Market Savings investments. I hope it can help prospective users make a more educated decision.

Detailed, full review:

The Save app advertises a Market Savings Account that “combines the security of FDIC-insured bank deposits with the upside potential of market returns”. I took a glance at the advertised yields (see below) and quickly filed it under “probably too good to be true”, but still came back and took a shot due to the “free” 6X leverage offered where I could invest $1,000 and get the returns of $6,000 worth of investments.

Here is a screenshot of their advertised rates, taken 2/29/24:

A short theoretical story. Let’s say you have $1,000 and put it into a 1-year CD at an FDIC-insured bank that pays 5% APY. At the end of the year, you’d have $1,050 guaranteed. Now, imagine you went to Vegas and instead bet that $50 interest on red at the roulette table. Worst-case, you’d lose the $50 and still have $1,000. Best-case, you’d double the $50 and end up with $1,100. A 10% annual return! Now, you might charge a fee to others for this “service”. Nothing if they lose, but a little cut if they win. So $1,000 worst-case, and $1,096 if they win ($4 fee for the service).

This gives you a basic idea of what I imagined was going on here, except replace Vegas with some fancy derivatives to give you market exposure to a portfolio of stocks and bonds.

The longer Save version. Here it is, straight from Save:

Every Save® account is connected with a FDIC-insured bank account. Your deposits are never at risk. We only invest the interest on your deposits, so no matter what happens with the ups and downs of the markets, your initial deposit is never at risk for investment loss.

This app is a combination of an FDIC-insured bank account, an SIPC-insured brokerage account, and an SEC-registered investment advisor. Your money is placed into an FDIC-insured account at Webster Bank that doesn’t earn any interest. Instead of paying you interest, they will buy a portfolio of securities that offer exposure to market products like stocks and bonds. These securities are held in a brokerage account with Apex Clearing, the same firm used by brokers like Robinhood, WeBull, etc. As your financial advisor, they will charge you a fee of 0.35% annually for this service. Ex. 0.35% of $1,000 is $3.50 a year. 0.35% of $10,000 is $35 a year.

This is all taken from Save’s official documents: press release, terms and conditions, SEC Form ADV, deposit agreement, and Form CRS.

Upon opening Market Savings and initiating a deposit to the Deposit Account, Save will, on behalf of you:

– deposit your funds in full into the Deposit Account provided by Webster, member FDIC and,

– purchase a strategy–linked security selected based on your risk tolerances within a Client Account

The Market Savings Product is comprised of a Deposit Account with Webster Bank, N.A. and a Client Account with Apex Clearing Corporation.

SAVE Advisers is an investment adviser registered with the SEC. SAVE Advisers provides its clients with combined banking products and wealth management services through a web-based algorithmically driven wrap-fee investment advisory program (the “SAVE Market Savings Wrap Program”).

The SAVE Market Savings Wrap Program is designed for investors with a cash savings investment profile. The investment objective of the SAVE Market Savings Wrap Program is to enhance our clients’ cash savings investment profile by providing attractive returns on capital using Save’s core investment philosophy while preserving their initial investment.

On the Market Savings Wrap Program, Clients will pay a wrap fee at a rate of 35 basis points (0.35%) per annum (one basis point is 1/100 of 1%) on either 1.) the total notional amount of each strategy–linked security or 2.) the total notional value of the Client Deposit Account (whichever is greater).

Save products are intended for conservative investors who are mostly concerned about the protection of their principal investments.

This reminds me of the No Risk Portfolio with 100% Money Back Guarantee. Your market-linked investment may go up 10%, 100%, or whatever, but the worst thing that can happen is it goes to zero (and you still get back your initial investment). According to this WSJ article (paywall), the CEO says the chance of a zero return in any given year is about 15%. This suggests that they are using some sort of leverage. (They also say the returns will count as long-term capital gains, unlike ordinary bank interest.)

The investments in Save portfolios are held for over a year so they are taxed as long-term capital gains.

This reminds me of the structured investments and “equity-linked returns with no downside” offered by many insurance companies. The insurance companies have much more onerous early withdrawal penalties where you can lose more than your initial principal, so this seems like a much lower cost option (even if still not what I want for my primary portfolio).

Where do they get those high advertised returns? Those are back-tested numbers:

Average annual returns are based on hypothetical back-tested performance by Save of the Save Moderate Portfolio from 2006 to present.

What happens if I try to withdraw my investment before the end of my term? There is a early withdrawal fee (a slightly complicated formula), but you’ll always at least get back your initial principal.

I understand that if I terminate my account prior to the completion of an investment term I may forgo all gains and receive back only my initial deposit.

Update: My final results from December 2022 to December 2023. I deposited $1,000 in December 2022, and ended up with… $1,000 in December 2023. I got back my initial $1,000 and that was it. All of the other investments apparently matured at a value of zero. This is despite having been told that I had positive returns in the middle of my term.

After my initial sign-up and $1,000 investment of my own money in December 2022, I did later participate in Save’s referral program and that did later result in additional earnings (my earnings were the same as the referred earnings). If you count this money, then I received a positive return. However, I don’t feel that this is representative of what you (the reader) could necessarily achieve on your own, so I chose to focus only on what I would have gotten without the ability to refer other users. I simply count the $1,000 of my own money and the $5,000 equivalent balance invested due to using someone else’s referral. On that money, my return was the same as everyone else who invested in my portfolio from December 2022 to December 2023: zero.

Save’s referral program is structured in that I earn the same bonus as the reader that signed up. Thus, you can see the returns of every single reader that used me as their referral (thanks again if you did!). I have gone ahead and attached the screenshot of every single referral that I have made with a matured investment, as of the end of March 2024. These are real-world results from real readers. The return percentages are usually based on a $5,000 equivalent investment (i.e. 1% return on $5,000 is $50.)

People with different start times and end times have different returns. Some have had zero returns. Some have had positive returns. The more recent returns are higher, and I hope that they continue to rise. However, I don’t count my chickens until they have hatched (fully matured and paid back any principal and interest).

That was a lot, but now you have all my returns and all the matured returns from all referred readers, down to the penny.

Save did put my initial $1,000 in an FDIC-insured bank account and just kept it there – nice and safe – doing absolutely nothing. No interest was earned. Each month, I got a bank statement and a brokerage statement. Here is a screenshot of my final bank statement showing $1,000 being sent back to me at the end of December 2023, after 12 months.

Below is a screenshot from my Save Brokerage statement, which was indeed held at Apex Clearing (a popular clearing firm for many fintechs, used by Robinhood, etc). Inside, they bought some sort of non-transparent, thinly-traded securities that were classified as corporate bonds. Perhaps someone with more advanced market knowledge can tell me more about these things. Example CUSIPs were 05600HTU9 and 05600H2F1.

Here is a tiny of bit info from FINRA:

The value of this security varied wildly through the year, from zero to $1 and all the way back to apparently zero?

How much of this security did they buy? In my case, it was about $15 worth per $1,000 invested. In comparison, earning 4% APY from a 1-year $1,000 traditional bank CD would equal $40.

I did sign up using a referral link and deposited $1,000 to qualify for the bonus $5,000 (at the time, lower now) for a total equivalent balance of $6,000. I thought this would be a good value bet, effectively leveraging any returns. Unfortunately, zero times anything is still… zero. I just got back my $1,000. Again, this excludes any referral bonus income.

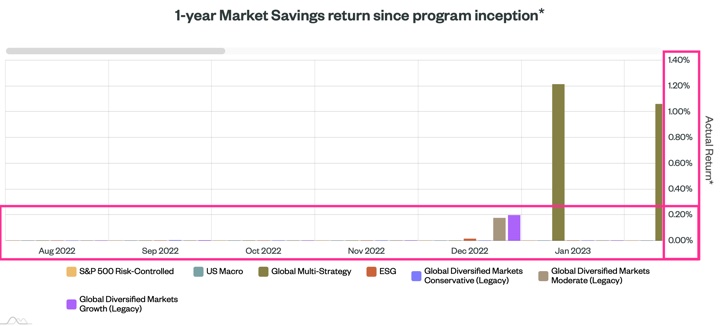

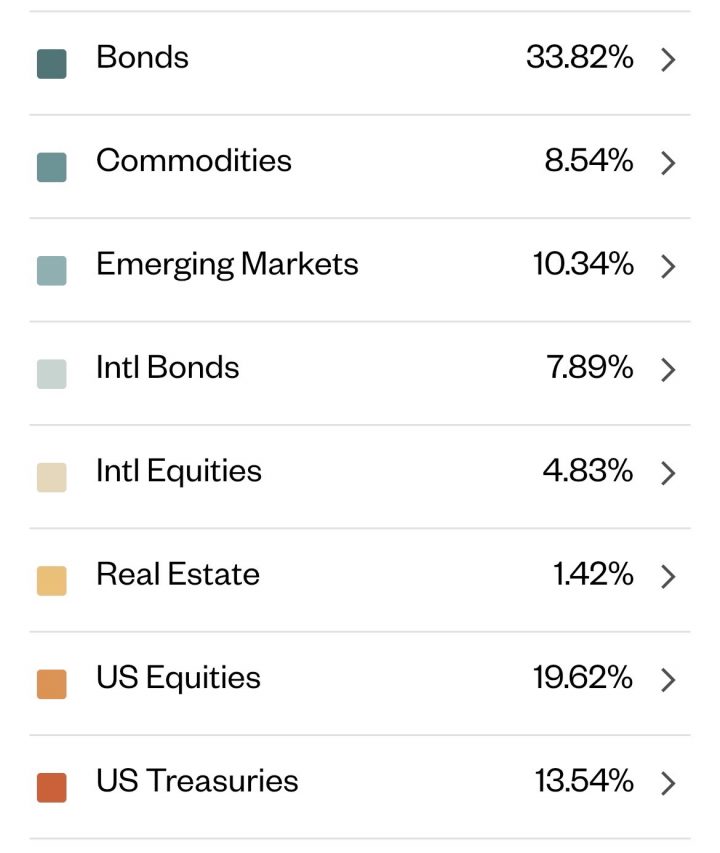

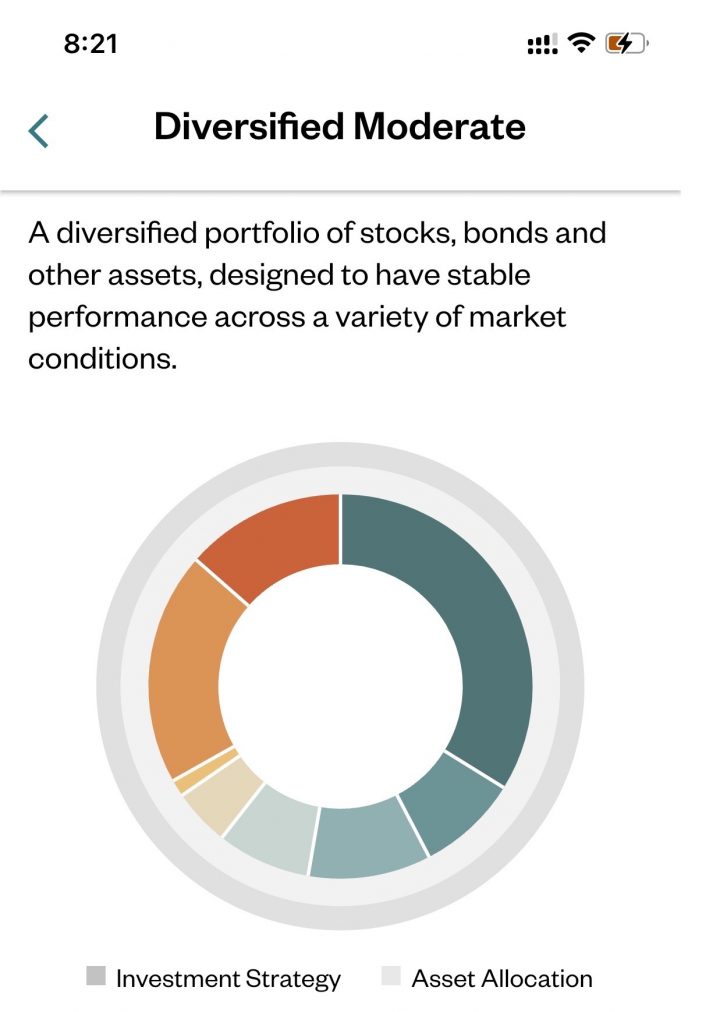

Now, I knew that a zero return was possible. A screenshot of the portfolio strategy that I picked initially is shown below. However, nearly every major asset class had solid positive returns for 2023. Yet, according to Save’s own historical returns page (see top of post), the highest return for any of their multiple portfolios that were held from both (December 2022 to December 2023) or (January 2023 to January 2024) was 1.20%, with the median return being zero. I’m afraid that I simply don’t understand what is inside the securities that they chose to buy, so I will not be investing anything further.

Honestly, I had high hopes for this product. It had potential and it didn’t even have to be that complicated. Again, look at this simple DIY principal-guaranteed investment linked to market returns.

Bottom line. The Save app advertises to folks “higher returns on their savings without the risks of the stock market.” They do appear to keep your principal safe in an FDIC-insured account, so indeed you can’t technically lose money. But it is unclear to me how they invest the rest. Despite their advertised 1-year return numbers, my personal experience was zero return (0.00%) on my 1-year term Market Savings investment that ran from December 2022 to December 2023. This matches their published actual returns for all investors during this time frame. This numbers excludes subsequent income from referral bonuses, which if you did include, would have resulted in a positive return. Other maturities may have experienced different returns, as shown in the screenshots above. I did receive my initial principal back as promised.

Note: Save Advisers pays a Referral Bonus up to $5000/$10,000 [product specific] as more specifically described in the current Referral Program as outlined by the Advisor here: https://joinsave.com/referrals, for each successful client referral. This amount is subject to change at any time.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

So the bank must be loaning them the money to invest? Otherwise, where would SAVE get the funds to invest? So what happens if the investment tanks and the bank calls on the margin? It seems SAVE recognizes you might not earn anything after a year but what happens to the SAVE account if it goes underwater?

My assumption is that Webster Bank is directly paying Save for these deposits in some way, in lieu of paying interest on the client accounts.

Jonathan with the 5k referral bonus I will give it a try. What term are you using 1yr 2yr or 5yr?

I’m doing the $1k for 1 year.

Any update on how your portfolio is doing? I recently signed up with your referral link for $1,000 for one year. Since the money is secured, I will give it a shot. They are also now advertising 8.6% apy.

8.26% *

Thanks for your patience. I have written a new post outlining my experiences and return numbers so far. I hope you find it useful.

https://www.mymoneyblog.com/save-app-experiment-actual-performance-numbers.html

I am very seriously considering using your referral and giving this a shot, but before I decide how much money to fund, I am interested in your experience after having been invested for a few months. Thanks for your insight.

Thanks for your comment, I have written a new post outlining my experiences and return numbers so far. I hope you find it useful.

https://www.mymoneyblog.com/save-app-experiment-actual-performance-numbers.html

Hi Jonathan, I tried opening the Market Savings Account with Save using your referral link but not sure why it still asks me for you First & Last name and Email/Mobile Number. Could you please provide that?

Sure, I can provide that, but please contact me via link below. My full name is Jonathan Ping. I’d rather not post my email online, thank you.

https://www.mymoneyblog.com/contact-me/

I don’t think your analysis is right. Save invests an amount equivalent to the principal, not the interest. The question remains, where does Save get the money to invest? And if my investment suffers a loss, how do i get the original principal out of Webster Bank? Ditto if Save goes bankrupt?

Maybe you are right. I looked through Save’s web site. I can’t find an answer to the question “If you deposit $1000 with Save, how much goes into the investment account?” How did you come to the conclusion that they only put a small percentage (equivalent to interest) of your deposit into the investment account? If this is true, then their claims of ~8% return are highly misleading if not downright false.

I don’t know Save’s secret sauce, but if you deposit $1,000 with them upfront and they only have to guarantee that you get back $1,000 in 1, 3, or 5 years, then I am saying that they definitely have the wiggle room to put some money aside and invest it. Webster Bank will pay Save some amount of money for those locked-up funds, especially with current 5% interest rates. They don’t invest your principal, but they do put some money aside (including the money from Webster Bank, plus could be some of their own money, I have no idea) and invest it *instead* of paying you some guaranteed interest like a bank. The 8% is not guaranteed, just like 8% based on past performance, just like 8% in the stock market is not guaranteed. But unless they are outright lying (which I don’t believe to be the case), then if you give them $1,000 then $1,000 does go into Webster Bank.

so you saying the one year term with 8.26% apy is a catch & webster bank dont calculated as other bank calculate interest rate so really it should be all straight clear simple calculations & nothig a catch for me senior 67 yrs old i am too old to understand there catch but bank should be at front honest with simple laungauge

When I made my investment a month ago, the advertised interest rate average was 8.96%. I see someone said 8.26% so can I surmise that they have averaged .7% more over a period of time. I left money in a CapitalOne high interest savings account at 4.1% to try out Save but at this writing it is saying 3.96%. It has fluxuated from 4.55 down to the present 3.96%. Good to know at the end of a year I’ll at lease get my initial deposit back with no service charge just in case it keeps on going down. Percentage going down usually happens when more military mode/sales increases.

They do in fact charge you heavy service fees for early withdrawal. They make you pay these fees before they refund your money. My return over the past 4 months has only been 0.77% . Currently I am going to lose 1-1.5% in fees for taking an early withdrawal. It’s not risk free.

It’s clearly a term product, meaning you bought it for a 1-year to 5-year term that you chose yourself initially. You broke the term early, so there is an early withdrawal fee. Sounds fair enough to me.

I’m assuming there’s no way to change the allocation you are invested in? I didn’t know about this until your $6500 post the other day, so I guess you need to keep it going another year to take advantage of the new referral investment earnings. 😀

The one that they put me in is different based on how I answered the questions. I want to say it had an expected return of 26% which most likely will not happen.

I had $1000 principal and $6000 in their reward money. Few days before term completion, a service charge took all the return off. No explanation on how that was calculated. So, in a week or so my term will mature with just principal returned. I hope. This when all the indices hit their peak this week. It was totally a scam. I fell for it just because of this blog. I am going to complain to the ftc and CFPB shine a light on these thieves.

That’s terrible of them! Good for you for filing a complaint.

Sounds like you gave them an interest free loan, which means you only lost at the rate of inflation for the term. This is why I didn’t fall for it. TGTBT offer seemed sketchy to me.

I’d like to hear what OP has to say about this, so I’ll bookmark the thread.

I’m 7 months thru a 1 year investment originally advertised for 8.96% max but knowing it could be lower. It’s been between 2-3% all along even with a $1000 birthday allowance. Watching and judging by what this blo shows.

hey Ant..so did you get the $6k bonus? I just deposited $6k…feels like too late to the game and is now a little concern.

Hi. I have mine maturing soon in different batches and see that the possible gains are way too low as compared to the 8-9% I thought I signed up for. I also fell for it ignorant about the language.

Please include complaining to BBB. I plan to complain as well, as I have CDs picked in 5 year terms. Very disappointed, I feel scammed in a way.

I would certainly like to hear anyone else with experiences at withdrawl

I filed a complaint against them with CFPB (declined), FTC(no response) and SEC (investigating).

hey why does CFPB decline?? do they give a reason?

I opened my account in October, it shows growth in November and December statements….despite being in a similar security to what yours was invested in, of which I have no idea what it actually is. I guess I’ll see if it all goes to $0.00 next October.

After a year, I only got my original investment of $1000 back. This App is a total scam.

hey Ryan – did you get your bonus??? i just deposited $6k…now a little concerns seeing the comments here.

Thanks for sharing. This is incredibly deceitful.

I have started a withdraw of my $5000 investment after 8 months and my “projected” fee to get my money back is $104. However, It is stated that I earned $61, so to get out of this “investment” should be $43

why didn’t you wait till 1 year to get the bonus Bill? wouldn’t it be better even though there is no interest?

Because I read this blog and was concerned that this may be a pyramid scheme.

The amount invested is backed by FDIC so I’m not worried about the principal but back in June they touted 8.96% and it’s no where that at any point. I’ll just be glad to get 6-8% but don’t figure that’s going to happen. I’ll ride it out till June

They should return your full principal even with early withdrawal, according to the terms when I looked them up above.

They will charge you a fee for an early withdrawal.

hi Jonathan – i just used your referral link to apply for joinsave. This seems like too good to be true, hopefully they aren’t going under in 1 year. Big fan of yours 🙂

Joinsave is terrible! They make you lock your money up with 7-9% promises. The SPY is up 28% yet my save account was up 1.75% LOL – i could do the same thing in my TD bank or my chase account without any lockups.

False advertising

I read all the info before investing and looks like I didn’t read between the lines or something is amiss! I’m gonna stay until June, at least they gave me a Birthday bonus that with that and the tinsy tiny interest, it’ll just about even out to 4% interest so I won’t loose terribly but certainly not 8.96% like was advertised. I’ll not invest with them again. I’ve had bad experiences with Reits before even though they advertise 12%, I’m not doing that again and there is some annuities that advertise paying 14% so I might even look into that, 14% is really too good to be true and you know the saying……

I deposited $1000 with them in Jan 23. It was invested in a low risk portfolio.

It just matured. Guess how much I am getting back? $1000.01 — that’s right, I earned 1 penny on $1000 in a year.

How would any depositor know if they borrowed your money to make large gains without disclosing their profits?

Is there a prospectus to prove there were zero profits? If not, depositors just gave them a free loan for capital to invest. Not sure the mechanism to measure actual performance if it’s not disclosed, or is it? If it is, what is the profit or loss on the fund?

i keep asking them to show the return on my investment thru the year but they just respond with marketing verbiage about how investment performance is variable and not guaranteed.

Shameful way to scam people/investors! Makes me wonder just how many they’ve got doing this investment strategy. Yeah, I’ve ask for info along the way and they just refer back to their info page.

TOTAL SCAM.

Tried them since they promised 7% (*results may vary), and just got back my $1000 investment after a year….wait for it…you’ve heard how good the S&P did over 2023…wait for it…

$1000.01

I had the exact same experience. I understand the returns will vary with market conditions. Some of the portfolios are invested in a variety of asset classes so the SP500 is not a good reference for all portfolios. But _every_ asset class increased in 2023 (except commodoties which are not contained in any of their porfolios) so I can’t understand how I had zero return. I asked this of their customer service several times but just got boilerplate language about variable returns. They email monthly about the return in each portfolio but I didn’t save them all —– strangely, there is no record of this on their web site that I could find. My monthly statements list trades of bonds that complete nonsense to me.

Well I invested more than that but the results may also be the same. I’ll moniter the results of others and project my results also. My offer was 8.96% I think remembering from memory and on my birthday they gave me $1000 but I’ll not include that in the final annalysis as it shouldn’t have anything to do with the earnings. Thanks for your contribution of information. It helps, sadly!

“Results may vary” – hilarious! My experience with JoinSave.com is SO similar with yours ?. I got the fantastic return of $ 0.01 after one year of blocking $ 10K with them … Total scam. Best wishes, A.

Save is worthless. After one year on $225k investment, I got $106 and a $1000 birthday investment bonus. I could have invested in a 5% no risk cd and made close to $9k this past year. Never again. They did return my principal, but what a waste. Stay clear of this non-action.

Totally agreed! My “return” was even worse (read my review here or on TrustPilot …)

Save has a webpage that shows the return performance of all actual 1-year Market Savings programs since the month of program inception. https://joinsave.com/market-savings-actual-returns

Don’t believe it. Stay clear of this investment. You will not lose your money, but you will not make any money either.

I’m in the same boat as everyone that has posted about SAVE. My investments have given me a birthday bonus and everything else hasn’t made much money. My entrance into SAVE, expecting to be 8.96% is barely 3% sometimes but 2% most of the time. Even counting the $1000 birthday bonus, which shouldn’t apply, it only brings my total investment to just shy of 5%, still a far cry from what they were promising. At least in another 4-6 months I’ll have my totals back whatever they are and I’ll not use SAVE again. Total sham investment program but getting into it reads as though those high yields are what’s possible but not probable. Now I see they feed us with false advertising hoping many will fall for it, which we all did, me included!

My returns are 8.04%, (total of 6k deposited) would be good to hear from those who got some good returns. I never thought this was guaranteed returns, but zero is a real risk of course.

If your returns are 8.04%, you better count yourself lucky! I’ve got about 4X that invested and my returns are 2.64% plus a birthday bonus which I’m not counting. Another 3-4 months I’ll be getting out and finding something much better to invest in. Been reading the mail on this investment strategy and it’s been the pits ever since I’ve been in but will stay to get what measly amount they give me. You are right, you don’t lose money, you just don’t get much like they say! TRULY A BOGUS CLAIM THEY GIVE UPWARDS OF 8-9%. Steer clear is my recomendation as what I’m going to do.

You will not get that birthday bonus, only any earnings they make for you on it, which will probably be $0.01 (one penny). I just learned this last week, I did not get my “birthday bonus” after the one year.

Yes, I’m not reinvesting in SAVE…after 1 year though I did get 2.39% back on my investment. I’m waiting on my birthday bonus. They just sent me a message of where to put it just like they did my investment and I’should know somthing in a week or two. I’ll make note of it on here then.

Mike

You did better than me. They want to know where to put your one penny in earnings, not the $1000. They asked me the same thin then, when the day came the $1000 just disappeared and I got one penny. Scam.

Thanks for sharing the actual returns link, will update the post.

It looks like the all the options we were put in are no longer even available (“Legacy”)

I had the same experience — invest for one year Jan 2023 – Jan 2024. Earned 0% interest, but at least got my investment back. I understand that returns are dependent on market conditions. Save is not transparent about what they invest your money in. But, like you, I cannot understand how I got zero return when every asset class (except commodities, which Save says they don’t not invest in) went up. Seems like a scam. But at least you lose your investment.

I’ve Googled ‘Save’ reviews and there isn’t any bad reviews. They must be so new that nothing bad is being said about them to dissuade investors.

I don’t know, WHERE you “googled” Save.com or JoinSave.com. Please read reviews here (including mine) plus check TrustPilot for example. As others also wrote here: you won’t loose your money, but you will end up with zero interest. Just your money will be blocked for one year, which you could put into 5.92% CDs with Merchants Bank of Indiana or get $ 150 bonus for every $10K deposited into a Savings Account with PenFed.org (promo until March 31). Best, A.

I can only warn anyone who falls for JoinSave.com’s bait tactics. One year ago they advertised 8.26% interest APY (not “up to” 8.26%), I opened an account and put $10K in. My one year experience just ended with them, they wired exactly $ 10,000.01 back into my funding account. Absolutely ridiculous. If you really want to give good advice to readers of your website, I would rather recommend 5.92% interest with Merchant Bank of Indiana or $ 150 bonus for every $ 10K deposited (max. $ 750 for $ 50K) with PenFed.org’s current extended promo (until March 31). JoinSave.com is simply waste of time. Regards, A.

Same experience here–0% return from April 2023 to April 2024 on a small sum I ventured to try out with Save. That in itself is not surprising given that the portfolio I invested in is top-heavy with bonds and–based on my research and estimations–averaged about negative 2% during that period. However, I have other problems with Save. The investments on my deposit and on the start-up bonus were made the same day in the same ETFs in the same proportions, but were showing significantly different rates of return. Despite their profession of transparency, when I asked why (twice), they gave me some rote, runaround answer about how the values of the investments differed, but didn’t explain why. I asked my investment advisor and he immediately guessed why–they’re not going long on the shares in the ETFs but are buying options. It’s in the fine print: “Save buys strategy-linked securities whose value is equal to the notional value of the purchased strategy-linked security. The notional value accounts for the total value of the position, vs. market value which is the price at which that position can be bought or sold in the market.” The account statements showing investment in corporate bonds through BNP Paribas is for the collateral investments backing up the options trading. But they don’t bother to tell you any of this when you ask.

During the whole period of my account, I don’t recall the website dashboard ever showing a negative return–just a very poor positive return–until the date of maturity, when it was suddenly zero. Could be coincidence, but maybe the dashboard was not accurately representing actual return prior to that date. So that just turned a bad taste to worse.

When your account is nearing maturity and it’s obviously doing poorly, they will advertise that you should invest in one of their high-roller portfolios of derivatives, etc., seeming a bit like a bait & switch. They now offer “Save +” where you’re guaranteed a minimum 3% APY, but I’m just not interested. I’d have done much better putting that bit of cash into some HYSA, MMDA, CD or T-Bill, which is what I’d recommend to anyone else for short-term cash savings. I’m not impressed with Save.

just sharing my experience which pretty much mirrors everyone else’s.

used Jonathan’s referral link, i put down $1000. the $5000 bonus was placed in the Diversified Moderate portfolio.

now a year later, my money has been returned. my $1000 deposit turned into $1001.06, and the referral bonus earned $1.67. so my total return is $2.73. yay (i guess)

I signed up for Save thinking they were a high-yield savings through Webster Bank. Save bragged of 5-7% rate. At the very end I realized they had disguised themselves and I tried to get out of it. When I called they threatened me with huge fees and insisted I ride out the year and that I would be pleased. The year ended a month ago, I invested $10k and received $10,078.30 back. Less than 1% which is worse than the local bank savings account. TOTAL SCAM!

Save is a scam so to speak. Back in June of last year, I invested due to a 8.96% offer and right now 2 months away, it looks like about 1.5% so far. I’ll not invest any further with SAVE and will advertise for them, haha!!!

Total scam!!! They advertise huge returns, but deliver NOTHING! They had my money for 1 year. I periodically checked by balance and the return was nil. I finally closed out after 1 year. They returned my principle, but ZERO interest! I should have left my money in a basic savings account at my bank. SAVE cost me hundreds of dollars!!! Total liars! Stay away!

I don’t know how SAVE can get away with what they do. I invested $25K for 12 months and received nothing in return. So they basically held/used my money for a year at my expense. I could have easily made at least $1K+ by investing in a money market fund. The worst part is that they actually tried to “incentivize” me to keep my money for longer. Luckily I saw them for what they were and pulled my money. Lesson learned.

Absolute and total scam. Finally have all my money back, so here you go. Principal is safe, but you’re giving them an almost interest-free loan of your money to invest. Here’s my experience:

Date invested Rate “promised” Rate returned

1/18/23 7% 0%

(I got back $1000.01 on $1000 invested)

2/15/23 7.5% 0%

3/15/23 8.26% 3.06%

5/17/23 8.96% 2.41%

Sorry I didn’t record all the decimal places on my first 2 investments… They post historical returns on their site that don’t match this at all. They’re scammers.

Save Adviser is a scam company. I gave them $150000 for 1 year into three investment accounts.

The first $50000 was into the conservative portfolio. after 12 months of maturity, I have to wait another 3 weeks for the transfer back to my account. I got back after almost 13 months $50,000.01

The other two with $50000 each were the same story. The return was $50,000.00 and $50,332.00.

The total of $150,000.00 for almost 13 months I got $332.01.

The bank statement balances they published on my accounts were around $4200 for a year.

No matter what portfolio I chose a conservative promised by them around 7% interest or a high-yield risky one, they sold lost penny stocks to give me my money back after maturity.

I would not be surprised if the company will be investigated and shut down.

My advice is to stay away from them as far as possible. If you already gave them your money try to get it back because they have access and full control of the bank accounts they opened behalf of you. Good luck

You can submit a complaint at https://www.consumerfinance.gov/complaint/. I did. see below.

Stay as far away from SAVE as you can. Last week I learned that the $1000 “Birthday Bonus” is not actually $1000, it is really that they put $1000 into an account for you and give you the earnings. You never get the $1000. So my earnings on the $1000 for one year in the SAVE account was….drumroll please… $0.01, yes one penny. They must have a bunch of shmucks investing over there, they could have invested in T-Bills and got me at least $5 for the year. They have huge issues. They word it to make you think you are getting an actual $1000 plus earnings for your birthday or more for a referral, but that is not true. I will be filing a complaint with the SEC for their deceptive practices. I can’t believe they are still in business. I think I made a grand total of under $5 for $250k invested over a year period. Somehow, they are investing other peoples money and keeping it, because no one can’t be that stupid.

It is secure in terms of you’ll get back your initial investment but the chance of you making hardly any profit is quite the case. I invested in 08/23 and my account just came to maturity, I put 10K in total, the first 5K just reached maturity, and after their fees I received $44.16 that’s less than 1% return 0.88% to be exact. I would have put my money in a HYS for 4.75% instead. They will lure you in with high returns of 9% or more then say the market blah blah blah… I still have another 5K maturing in one month and those returns look to be less than $200 as of today. The percentage of returns changes on a daily basis very volatile and dependent on the stock market so why not just invest directly in the stock market and leave it long term, the fees will be a lot less and you’d be getting more. This was a waste of time, I regret tying up my funds for a whole year for nothing, but it was a lesson learned… I do not recommend.

Save’s S&P 500 Risk-Controlled portfolio produced returns for a 1-year Market Savings program of 13.1%, after fees.

This ad just came in my email. My birthday bonus is suppose to transfer today or tomorrow. I invested $24K a year ago last month and this month. In all that $24K brought exactly (drum roll please) according to computer calculator.$385.40 in my banks savings where I told them to put it. That’s 0.0160583333333333% and a long way from the promiised 8.96% when I sighed up. I’m not putting money back in them either. I sure do hope that the SEC can do something about them. I filed paperwork online to them and hope something can be done…like maybe shut them down!!!

Mike

Your math appears off. $385.40/$24,000 equals a 1.606% return. Were you invested in the S&P? Their website shows the S&P investors performing much better.

Yes you’re right, I shouldn’t have put the % sign.

385.40/24000=0.0160583333333333

I sent an email to SAVE asking about my Birthday Bonus and when could I receive it. My original investments I received the principal within 2-3 days and the interest a day or two later. My Birthday Bonus if going by my previous sentence should be here today but their email I just received says 15-20 business days. I’m gonna watch to see if actually comes to pass since I’ve watched what others have said here.

Sent the previous note and then this came in within minutes….so they’re keeping my BD Bonus! Should’ve known! Very misleading…I’d rather them not give it at all! Now I’m waiting for info from SEC! Has anyone gotten any info after filing with them…asking for a friend!!!

Referrals and other rewards must stay invested until they’ve matured and cannot be withdrawn.

Save makes the investments in the Client Account on behalf of our customers and the return, not the investment itself, is yours (minus our fee).

>I sure do hope that the SEC can do something about them. I filed paperwork

>online to them and hope something can be done…like maybe shut them down!!!

Good for you! I’d like to do the same.

Can you pls post the URL for doing so?

Thanks

Gladly…here it is

https://www.sec.gov/submit-tip-or-complaint

This is such a joke. My 12 month matures on 10/28. The gains were stable for the first several months…but as I log in the past few days as they keep sending me emails to tell me to renew….the gains drop daily.

SAVE is a joke. I had them with a moderate investment and it basically paid me peanuts. Not gonna trust them again. Them telling me a little longer than a year ago to invest at 8.96% and it paying me 1.606% not gonna happen again. The birtday bonus, I eagerly waited to see what happened to it and the info they sent me was I don’t get it just the interest earned from the bonus which was less and a penny!!! What a ripoff!!!

STAY FAR AWAY FROM SAVE. They will give you your money back, but you will earn nothing. Put it in a money market if you want security and 4.5% (real) money. SAVE should be investigated by the SEC.

You can submit a complaint at https://www.consumerfinance.gov/complaint/. I did. see below.

On 10/27, it showed I have $18 in gains. On the maturity date of 10/28, no gains. We shall see if the $36 in gains I am showing for the referral will also go down to $0 in the next week.

Looks like i ended up getting about $34 total in addition to my $1k returned.

Absolute and total waste of investment – 2% return if you’re lucky.

Finally got the last of my “birthday bonus” back from them, so I can clear this from my books. Like others have said, the high interest rates they “promise” (see fine print) are empty promises. If you want to give someone an effectively no-interest loan while keeping your principal safe, go for it. If you’re trying to grow your savings, they won’t beat inflation, much less the S&P500. Positively awful experience. Absolutely nothing good to say about this company.

You can submit a complaint at https://www.consumerfinance.gov/complaint/. I did. see below.

Save has a partnership with Webster Bank, which is a legit bank. I just messaged Webster thru the Facebook page

https://www.facebook.com/websterbank and advised them to end their association with Save

because they are damaging their reputation. If you agree, you may wish to message them also.

I filed a compliant about Save with the Consumer Financial protection Bureau, saying they are advertising rates far exceeding what is realized. Today I got a letter from Webster Bank, saying that SAVE is a division of the Bank, which I did not know, and verifying receipt of the complaint and “working on a resolution”. If believe SAVE has treated you unfairly, you can sumbit a complaint at

https://www.consumerfinance.gov/complaint/.

These idiots need to send a corrected 1099.

After one year in Save, I removed my money. Here’s the email they sent me:

Withdraw Finalized

Hi Robert,

We have completed the request to withdraw a deposit from your Market Savings at Save.

Your net returns are $0.00. While neither of us wanted this performance, the great thing about Market Savings is your initial deposit is 100% safe from market risk when held for the entire term length.

Net Returns $0.00

If you have any questions, please contact our customer support team.

I got similar “results.” I submitted a complaint to the Consumer Fraud Protection Bureau. They followed up by notifying Save and Webster Bank about the compliant. I got a response from Save with self-serving legalese and it did not go any further. However, if many other people also complained to the CFPB, there might be more investigation. However, with Trump shutting down the CFPB, unethical companies have the green light to over-promise and under-deliver without accountability. If you disapprove of this, voice you concern to your US representative and senators. If you don’t get satisfaction, vote them out in 2026.