Recently, I have been exploring the “safe” options inside various 529 plans. This would be a good choice for those who want to feel like they are making continuous gradual progress and avoid the swings of the stock market, similar to what is offered in pre-paid tuition plans in certain states like Florida. The problems with those plans are that they are usually limited to residents only, and your kid often has to go to one of the in-state schools to get the guaranteed tuition benefit. One unique pre-paid type of plan is the Independent 529 plan, but it is also restricted to certain schools (mostly private liberal arts colleges).

Next, there are plans with guaranteed-return funds backed by insurance companies, or certificates of deposit from banks. However, these types of investments are still subject to inflation risk. If a period of high inflation occurs, your returns could be squashed. Even with current deflation concerns, given current government policy I think high inflation in the future is still a potential concern.

So what’s left?

CollegeSure Tuition-Indexed CDs

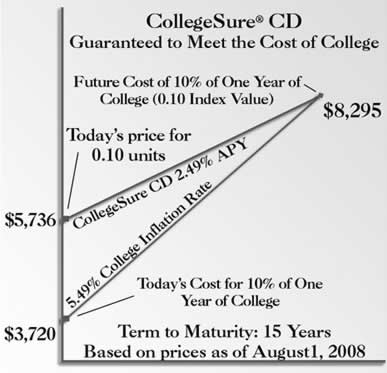

Offered by the College Savings Bank, these are FDIC-insured certificates of deposit which offer an interest rate linked to college tuition levels. The CollegeSure CD earns an annual percentage yield (APY) over the life of the investment that is 3.00% less than the college inflation rate. (For a while, this margin was only 1.5%.) These are only available through either the Montana or Arizona 529 plans, but you can use the proceeds towards a school in any state.

The CDs are available in maturities ranging from 1 to 22 years, so you are basically pre-paying tuition at a fixed premium. Here’s an illustration from their site:

Changes in costs are tracked by the Independent College 500 Index (IC500), which is derived from the average tuition plus housing costs of 500 private colleges. Over the last 10 years, the college inflation rate has been 5.4% annualized, Over the last 20 years, it was 5.7% annualized. Of course, this is just an average and it both excludes public universities and ignores the average aid packages given out, but it seems to be a reasonable index.

Treasury Inflation-Protected Bonds

Treasury Inflation-Protected Securities (TIPS) are bonds that promise you a total return that adjusts with the CPI index for inflation. Very generally, it works like this: if the stated real yield is 2% and inflation ends up at 4%, your return would be 6%. TIPS are issued and backed by full faith of the U.S. government. Right now, they are only available in 529 plans in the form of mutual funds like the Vanguard Inflation Indexed Bond Fund. Some plans offer them as part of their age-based investment mixes, but a few offer them as standalone investment options. The Ohio 529 plan ($25 bonus) looks to offer the cheapest option, with an annual expense ratio of 0.32%.

The actual real yield you get varies, but here is some historical market data for a maturity of 10-years, which is close to the average mutual of the Vanguard fund:

To make a rough estimate, I’d say you average about 2% real before fees. After about 0.3% in fees, you’d end up with 1.7% + inflation.

Inflation is tracked here by the CPI-U (Consumer Price Index for All Urban Consumers), a number tracking the price of a wide basket of goods and services. From January 1999 to January 2009, the annualized inflation rate was about 2.5%. Over the last 20 years, it has been about 3.0%.

It does not focus on college tuition, or even include it explicitly as far as I know. However, there should be some correlation to college tuition.

So which is better?

Would you rather have:

If we use the average numbers from the last 10 years, the CollegeSure CD would have earned roughly 2.4% annually and the TIPS fund would have earned roughly 4.2% annually. This would seem to tilt in favor of TIPS, but there are two problems:

- Unlike with the CollegeSure CD, you can’t match the maturity of the TIPS fund with your goals. It’s more or less fixed at 10 years forever. For example, if you only have 2 years left until college, you might want to start moving money out because you can still lose principal in the short-term due to interest rate fluctations.

- If the rate of college tuition rises significantly higher than overall inflation by greater than 4.7% a year, then the TIPS fund would fall short.

One could always split money between the two as well, but for not I’m just investing in the TIPS. College inflation may continue to outpace overall inflation (or it may not), but I doubt it will do so by more than 4.7% a year for an extended period. Also, I believe that investment options in 529s will only improve with time. One day, I expect to be able to buy individual TIPS to more closely match maturities with our time horizon.

This is not to say I’ll necessarily be 100% TIPS – I’ll most likely throw a bit of stocks in there – but I think it’ll be a big component of our plan.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

While it is true that the prepaid tuition guarantee only applies if the student attends an in-state public college, nevertheless, for students who attend out-of-state or private colleges, the pre-paid program permits the transfer of the value of the plan which would otherwise have been paid to the public college in Florida. In other words, a participant in the pre-paid program is still purchasing protection against rising college tuition/inflation, regardless of whether the student attends a covered in-state Florida public college.

According to the program’s FAQ, “if the beneficiary attends a qualified out-of-state college, public or private, the Florida Prepaid College Plan will transfer an amount equaling the current rates paid to a public university in Florida. More than 1,700 colleges and universities have been approved for the out-of-state transfer of Florida Prepaid benefits”.

For the record, I am a Florida resident and participant in the Florida prepaid program.

Hi there, nice summary. Is it possible to buy TIPS in an IRA or other retirement tax-advantaged vehicle? Specifically, NOT a TIPS mutual fund. I believe TreasuryDirect only interfaces with taxable money, right? I just don’t want to deal with the tax accounting basis for a TIPS vehicle…the time spent keeping track of it seems not worth it. I like to value my free time at 2x my salary (i.e. is doing this going to likely net me 2x the rate of my salary? not worth it, unless I think it’s fun)

I do understand 529s don’t qualify for this…is there any benefit a person might have saving within this vehicle if the beneficiary is not known yet? Is the beneficiary transferable?

Adam – Thanks for pointing that out. Too bad the beneficiary or parent has to be a Florida resident.

K – You can buy individual TIPS in several brokerage accounts. You can buy them with no commission besides the bid/ask spread in a Fidelity IRA. I think Vanguard charges $35 or so per TIPS trade.

Hi,

We have two things going right now for my daughter. We have a 529 plan set up through Upromise so we can get cash back savings on our purchases. We started it with some money (not much). The other thing we have is a savings account which we put money in every month. We are taking that money and putting in the mefa plan. My daughter will be able to pick from 80 plus colleges and universities both public and private. In essence, we are prepaying the tuition at these institutions. If she does not want to go there, she can get the money back with some rate of return (not as much as a 529, say invested in equities).

We did this because we felt this way we could get the best of both worlds. We can put the money we save into a vehicle that helps combat tuition inflation and the money the 529 with is based in the market will be for books & such. Our daughter is 1 so she has lots of time & the 529 is invested aggressively in equities.

The Wisconsin EdVest program has 2 CD Portfolios as investment options as well. Definitely worth a look.

http://www.edvest.com

You can also buy individual TIPS directly from treasury via treasurydirect.gov, much like I-bonds. No commissions, no bid- or ask- spread: when you buy them directly from treasury you don’t buy on a secondary market as with brokerages, you buy them when they are actually sold first or re-opened at face value. The drawback is that you can only do it at specific times i.e. during initial offering (when TIPS are sold or when they are re-opened). Including both the times when they are sold and when they are re-opened you get 2 chances a year for 5- and 20- year TIPS and 4 chances a year for 10-year TIPS (this includes both when they are sold and when they are re-opened). You can go to treasurydirect.gov and read everything you ever wanted to know about TIPs.

Incidentally, TIPs don’t add rate of inflation to your fixed rate as the article above says. What TIPs do is a) pay you fix rate b) at the end of the year your principal is adjusted for inflation. The interesting item is what they do in case of deflation: if you buy from the treasury during initial offering, you’ll never lose your principal, but you may lose your interest and adjustments. However, as long as there is cumulative inflation between the date you purchase and the maturity date, you’ll get at least the actual yield-to-maturity cited when you bought it. But if you buy from a broker – i.e. on a secondary market, and if the issue you buy already includes accrued principal in the price, you can lose money in deflation. I suggest you read the explanation at http://www.treasurydirect.gov; also google for TIPS and deflation.

There are also I bonds which use a specific formula to add inflation to a specific fixed rate (set twice a year). But you are only allowed no more than 10K of those a year – 5K via treasurydirect and 5K in paper form from your local bank.

The interesting thing is what happens with both I bonds and TIPs during deflation. Nope, you’ll never lose your original investment even if there is net deflation, but you may lose some of the adjustments you got in-between. You can google for “TIPS and deflation” – there are detailed explanations available.