Updated with my own experience and new referral bonus. Bask Bank is a FDIC-insured savings account that pays you American Airlines (AA) miles instead of cash interest. Every $1 earns 1 mile a year. For example, $1,000 kept for a year would earn 1,000 AA miles at the end of the year. If you kept $50,000 there for a year, you would earn 50,000 AA miles at the end of a year. There is no minimum balance and no monthly fees. I’ve updated this review after opening an account.

Bask Bank is part of Texas Capital Bank (FDIC Certificate #34383), which also runs BankDirect. BankDirect has been giving out American Airlines miles for many years on their checking account, but with different requirements and a steep monthly fee. Note that they are all the same bank in regards to the $250,000 FDIC insurance limits per depositor type. Bask Bank routing number is 111026177.

Account opening process. Opening an account was done all online with no issues, with no physical paperwork to send in. They state there is no hard credit check upon opening, and there was none upon my own opening. I received all my promised points (past bonus and monthly interest) on time and without issue. Note: They do not currently offer joint accounts.

Value calculations. If you valued American Airlines miles at 1 cent per mile, then this account would earn you the equivalent of 1% APY. ($10,000 a year = 10,000 AA miles = $100 value.) Given that other online savings accounts also earn about 1% APY nowadays, this has become a closer call after you consider the tax consequences…

1099-INT details. If you get miles instead of cash, what happens at tax time? Bask Bank and BankDirect has stated that they plan to issue 1099-INT for 2020 interest earned based on a valuation of 0.42 cents per mile. This can be found deep in their disclosures:

Since you are Awarded Miles based on the average collected balance in your Account each month instead of interest, Bask Bank calculates an interest equivalent based on a good faith estimate of the value of the miles. Your interest rate and annual percentage yield may change based on a change in either the Miles Award Rate or the estimated value. Miles are currently valued at 0.42 cents per mile, the equivalent of 0.42% annual percentage yield.

So if you held $10,000 for all of 2020 and earned $10,000 miles, current your 1099-INT will show $42 in interest paid. However, this is subject to change and I don’t really like that sort of uncertainty. It is unlikely but still possible that they could change this number and it would be a hassle to dispute such a valuation.

Useful for keeping your AA miles active. Airline miles are useful, but also subject to rampant inflation. Since AA miles are worth less every year, I do not plan on using this as my main savings account. However, the ability to keep about $15 in there and earn at least 1 mile per month to prevent my existing American miles from expiring, that could be useful. If I need a certain amount of American Airlines to reach an award, this may be a backup option as well. I have a large amount of AA miles, so this account gives me peace of mind that they won’t suddenly expire when I’m not paying attention.

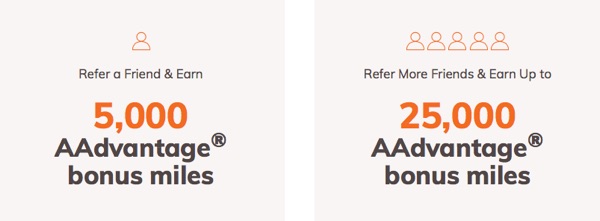

New account referral bonus. Bask Bank now runs a refer-a-friend program where if the person referred opens an account by 9/30/2020, deposits at least $10,000, and keeps it there for 90 days, they will earn 5,000 AAdvantage® bonus miles on top of the usual interest. The referrer will also then receive 5,000 miles. Here is my Bask Bank referral link, thanks if you use it. After you open the account, you can also refer up to 5 friends yourself:

If you again value an AA mile at 1 cent a mile, then the bonus is worth $50. Earning $50 for keeping $10,000 there for 90 days is the equivalent of a bonus APY of 2% for those 90 days. So in total, you might get the cash equivalent of 3% APY over those initial 90 days with the referral bonus if you use that 1 cent per mile valuation.

Bottom line. Bask Bank is an online savings account that pays you American Airlines (AA) miles instead of cash interest. It won’t be a great fit for everyone, but may be interesting to those that can maximize the value of an American Airlines mile. You may also like the ability to keep all your AA miles from expiring by keeping a small amount of cash at the bank.

I started looking into financial independence because I simply couldn’t imagine doing what I was doing every weekday at that time for another 30 or 40 years. Some people know exactly what they want to spend their life doing, and it also pays the bills and then some. I was always envious of those folks. Strangely, I never really felt that making more money was the final answer. I saved diligently in order to quit my job and go back to school and explore alternate paths.

I started looking into financial independence because I simply couldn’t imagine doing what I was doing every weekday at that time for another 30 or 40 years. Some people know exactly what they want to spend their life doing, and it also pays the bills and then some. I was always envious of those folks. Strangely, I never really felt that making more money was the final answer. I saved diligently in order to quit my job and go back to school and explore alternate paths.

The Best Credit Card Bonus Offers – 2026

The Best Credit Card Bonus Offers – 2026 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2026

Best Interest Rates on Cash - 2026 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)