(In this post, I’m not going to provide all the background information on savings bonds that I normally do. For that, please read the older posts in my Savings Bonds category.)

(In this post, I’m not going to provide all the background information on savings bonds that I normally do. For that, please read the older posts in my Savings Bonds category.)

When the Treasury announced the $10,000 purchase limit for 2012, a few readers asked if you should buy savings bonds in January, or wait until later in the year. Since then, a few things have happened. For one, the Federal Reserve has basically said that they will keep their target fed funds rates at zero until late 2014, while setting a target inflation rate at 2% annually. Translation: Interest rates on savings accounts and similar products will be remain crap while the things we buy get more expensive.

Also, we have another month’s worth of Consumer Price Index (CPI) data which is how the inflation rate is defined for savings bonds. The next 6-month variable rate update will be based on the CPI-U change between September 2011 and March 2012. We are halfway there:

CPI-U

Sep 2011 226.889

Oct 2011 226.421

Nov 2011 226.230

Dec 2011 225.672

Jan 2012 ?

Feb 2012 ?

Mar 2012 ?

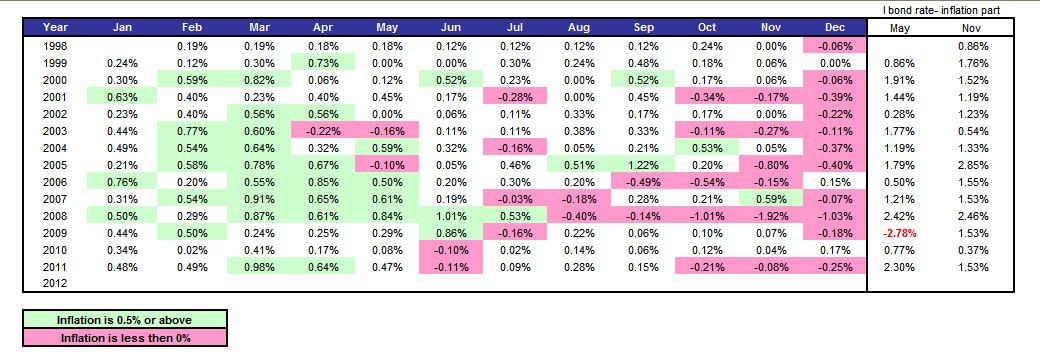

You can see that inflation is actually negative over these three months. However, user MoneyOCD of Bogleheads posted this informational chart showing that in recent years there have been many periods of negative inflation from September to December, only to be followed by periods of higher inflation from December to March.

Basically, making predictions now is premature. If you buy in January through April, you will get a fixed rate of 0%, and a variable rate of 3.06% for six months. Given the interest rate environment, this is pretty much one of the best options for “safe” money. If you wait all the way until May, you’ll get something new based on whatever happens to inflation the next few months along with a fixed rate that will most likely be zero again. The inflation rate resets every 6 months based on your purchase month.

In general, if you have the money and are looking to put it in shorter-term, low risk investments that are guaranteed not to lose money (in terms of face value), I would be maxing out my limit on savings bonds for 2012. Keep in mind that savings bonds can’t be cashed in for an entire year after purchase. My personal opinion on the short-term? I don’t see any benefit in waiting until May. If you have money to put aside now, buy Series I savings bonds now. If you don’t, just wait until you do. The rate is already higher than savings accounts or 1-year CDs, and by waiting around in a 0.75% savings account or 1-year CD you’ll be missing out in interest.

If you’re looking to buy in January, I’d put in your order today at TreasuryDirect. It’s better to buy near the end of the month, as you get credit for the entire month no matter if you buy at the beginning or the end.

The Best Credit Card Bonus Offers – 2025

The Best Credit Card Bonus Offers – 2025 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - 2025

Best Interest Rates on Cash - 2025 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Another option that has been thrown around the bogleheads forum is that the new rate for bonds purchased after May 1st will be release April 13th at 8:30am Eastern. This gives you time to decide when or not you want to purchase before month end.

I think it’s safe to assume that new rate after May will not be too far off from 3%. I’d think give/take few basis points 3% is pretty much guranteed based on the history. Am I wrong?

What’s your experience wiht the other non I-bonds? If you max out on iBonds, should the “series” bonds be considered?

Just 10k, doesn’t matter much…

Was trying to figure out TreasuryDirect… The site is too confusing. I’ll park my money elsewhere.

If you wait until the end of April, you’ll know what your full year (minimum holding period) rate of return will be. Of course you can generally estimate it since it’s based on publicized numbers.

@bluecat, EE series bonds aren’t too bad, but you really have to hold until maturity to get the benefit of them, so they’re not really good for short term savings. Plus with investments over that long a term most people can tolerate more risk so there are investments with better yields available.

csdx, thanks.

Yes, between April 15th and the end of April you will know what you’ll be getting for a full year. But your decision then is basically buying in April vs. May. However, while you’re waiting your money may be earning 0.80% at ING Direct or wherever.

EE bonds are another option as they are guaranteed to double if you hold them for 20 years (3.5% annual return). That’s a long time, and if you hold anything less than 20 years, you may end up with a lot less. For me, I considered them as a mortgage offset balance, but I don’t plan to have my mortgage for 20 years.

Interesting chart. Inflation during the first half of the year, deflation during the second.

Even if the I bond rate decreases to zero the savings rates/cd rates from banks are not going to be much better….We are saving to buy a house in 3-5 years from now and earning .07% from a savings account is very attractive. Our savings are going into I bonds….lets hope the gov’ment does’nt default =)

you will get a fixed rate of 0%, and a variable rate of 3.06% for six months

Could someone please clarify this for me? I don’t comprehend what this means…

Has anyone heard of Mike Dillard and his program called “the elevation group”

is it true that the dollar will drop so much that it will be worth close to nothing within the next year?

please someone give me your honest opition. is it worth it to buy this program, is it a scam?

thanks,

gio

OT: @gio: IMHO, it would depend on the results of the November election.

I suppose I’ll be getting my federal tax overpayment refund in the form of I Bonds. At least then they will be in paper form and earn ~3% (depending on the inflation for the succeeding 6 months)

I agree that the Treasury Direct website is a major PITA. I think it is all part of the Treasury Dept’s policy of discouraging Savings Bond purchasing.

TreasuryDirect is unavailable.

We apologize for the inconvenience and ask that you try again later.

Nice tip about buying at the end of the month.

I don’t know whether anyone looks at this old page, but the March CPI-U has been released as 229.392. That’s 1.10% over September’s figure, so I expect the annual rate will be 0% fixed + 2.20% inflation = 2.20%. The previous few months looked like it would be close to 0%, but March had a big bump up. I guess I’ll be keeping my August 2011 bonds which I was considering cashing in November 2012 (1 year + 3 months to be able to keep all of the current 3.06% rate). 2.2% will still be better than a short term CD.