While updating my portfolio spreadsheet, I noticed that it had been 10 years since I bought my first electronic savings bond. I recently listed Reasons To Own TIPS, Treasury Inflation-Protected Securities and Reasons To Own Series I Savings Bonds. This got me wondering – How did my 10-year savings bond performance compare to buying a TIPS ETF or a TIPS mutual fund?

While updating my portfolio spreadsheet, I noticed that it had been 10 years since I bought my first electronic savings bond. I recently listed Reasons To Own TIPS, Treasury Inflation-Protected Securities and Reasons To Own Series I Savings Bonds. This got me wondering – How did my 10-year savings bond performance compare to buying a TIPS ETF or a TIPS mutual fund?

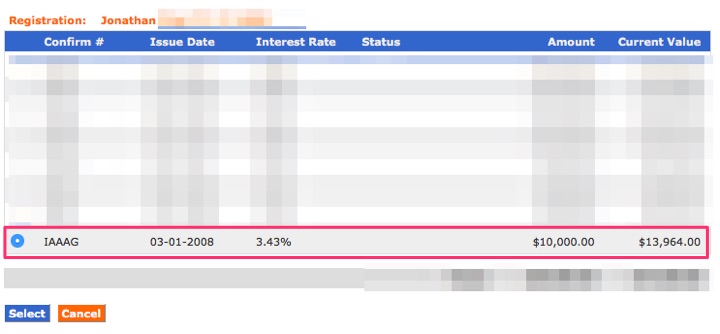

A $10,000 Series I Savings Bond issued 3/1/2008 is now worth $13,964 as of 9/1/2018, a 3.4% annualized return. The interest automatically accrues and compounds, assuming no withdrawals were made. This is taken straight from my TreasuryDirect.gov account.

The largest TIPS ETF is the iShares TIPS Bond ETF (TIP). According to ETFReplay, below is the total return (green) of $100 invested from March 2008 to September 2018. Total return includes the effect of the immediate reinvestment of any dividends and distributions. TIP is a basket of individual TIPS, with an average effective maturity of about 8 years. $10,000 invested in TIP on 3/3/2008 would have turned into $13,230 on 9/4/18, a 2.8% annualized return.) (Actual dates used are the closest trading days.)

The largest TIPS mutual fund is the Vanguard Inflation-Protected Securities Fund (VIPSX). According to Morninstar, here is the total growth of $10,000 invested from March 2008 to September 2018. VIPSX is a basket of individual TIPS, with an average effective maturity of about 8 years. $10,000 invested in VIPSX on 3/1/2008 would have turned into $13,100 on 9/1/18, a 2.7% annualized return.

I could have also bought an individual TIPS bond back in March 2008 that matured in 2018, but I’m not sure about how to compute the total return with reinvested dividends (which kept varying with CPI) all the way up to today. If someone wants to run the numbers, I’d be happy to add them to this post.

Bottom line. Over roughly the last 10 years, the total returns from owning savings I Bonds vs. popular TIPS ETF vs. popular TIPS mutual fund varied between 2.7% vs. 3.4% annualized. The savings bond probably beat the ETFs and mutual funds slightly this time because it held a fixed rate of 1.2% while the other bond funds have an ongoing ladder of TIPS with lower average real rates. Over the next 10 years, with the current low fixed rates on savings bonds, the ETF and mutual fund might win slightly instead. This is why you would compare the current fixed rate on savings bonds vs. the current real yields on TIPS when considering a purchase between them. I would also factor in the tax deferral feature of savings bonds.

The bigger question is whether you want to own inflation-linked bonds at all. (See links at the top of post for help on that.)

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Hey, Jonathan you inadvertently have the dates wrong in a couple of places in this article. The charts show the period you refer to, but the text has 2018 in a couple of spots where I think you meant 2008. Thank….enjoy your articles…

Dan

Thanks, I think I caught them all.

Yea, I added VIPSX to my Roth back in 2010 and bought some with the annual contributions each year. It has yielded a disappointing 1.8% over those 8 years…. But that is the magic of diversification 🙂 .

Now that inflation is raging, it would be nice to revisit this analysis.

Good idea 👍