Ah, budgeting. New year, same old goals? While I’m not one of those people that think everyone needs a detailed budget, I do think everyone should track their spending at least once a year or so. This way, you have a real snapshot of where your money is going (which may just surprise you). Writing down every little transaction on a piece of paper or even tapping it into your smartphone can get really tedious. So here’s what I do to manage it in 15-minutes a year.

Put All Your Spending On A Credit/Debit Card

The main idea is to put all your spending in an electronic format so that a bank keeps track of all your purchases for you instead of little slips of paper. If you don’t like credit cards, use a debit card. But credit cards offer superior consumer protection features, so I prefer them. You don’t need to put it all on one card, but it does make things simpler.

Now, do this for a month, and avoid paying cash whenever possible. Don’t change your spending behavior, and there is no need to record anything.

Sign Up For Mint.com

Next, you should sign up for the online aggregator tool Mint.com. I also like versions of Yodlee, but it looks like their development has slowed significantly. To start, all you need is your e-mail address and the login details for your credit card website.

Next, you should sign up for the online aggregator tool Mint.com. I also like versions of Yodlee, but it looks like their development has slowed significantly. To start, all you need is your e-mail address and the login details for your credit card website.

I know that many people are wary about giving out their login credentials, but in my opinion your credit card login is not as sensitive as say, a bank login. Credit card companies make so much money that they are happy to refund any fraudulent charges immediately. It is in their interest to make you feel very safe about using credit cards.

Anyhow, Mint has improved their back-end system so that most credit card information syncs up fairly quickly. Click on the “Transactions” tab on the top of the page, and you should see all your recent purchases. You can wait until after a month of spending on the card, because Mint should upload all your historical transactions within the last few months.

Categorize Transactions

Without any input from you, Mint will have tried their best guess for the Category of each of your purchases. They’ve gotten better, but there will likely still be a few that are incorrectly categorized or simply left labeled as “Uncategorized”. In addition, some of your purchases from a megastore like Walmart/Target/Costco might be “groceries” or it might be “electronics”.

Use the the pull-down menus and spend a little time “teaching” Mint the proper categories that you prefer. If you want all future CVS purchases to be under “Groceries” instead of “Pharmacy”, you can click on Details and make a rule that will do that for you automatically. This saves lots of time in the future.

Finally, if you have certain transactions that you wish to have Mint ignore in your budget calculations, use the “Exclude from Mint” category.

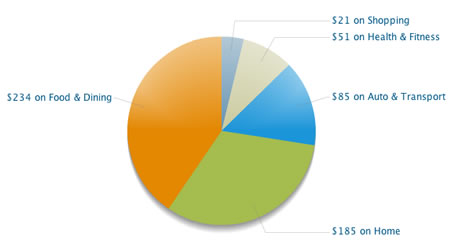

Pretty Pie Charts!

After all your transactions look nice, click on the “Trends” tab on top, and check out some pretty pie charts created from your spending history. The charts are very interactive, click around and drill down into your data. You might need to go back and re-label some expenses to get everything to sort nicely.

Now you should have a clearer idea of where your money goes. If you have bills that you had to pay by bank account, you’ll want to account for those separately if you don’t want to sync it up with Mint. If you make some small cash purchases, just track your ATM withdrawals. I just made a rule that labeled all ATM withdrawals “Dining Out”, since that’s usually where it goes.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

my CC statements already do the slicing and dicing for me. a great 5 minute snapshot of where money is going

I still prefer Yodlee over Mint. I really would like to like Mint. Yodlee just does it better, albeit with less flash. Check out my comparison of the 2 and maybe you’ll agree.

http://sunkcostsareirrelevant.com/2011/01/review-of-yodlee-vs-mint/

I use Quicken at home, but I’m not opposed to using a service like Mint.com. I tried it once, but one of my favorite Quicken features wasn’t available, so I stopped.

I use savings goals in my checking account. My wife and I both have a little “Fun Money,” but rather than use separate accounts for this, we each have a Quicken Savings Goal that draws from our Checking account in Quicken. The balance in the bank might be $2k, but if my wife has $300 in her ‘Fun $’ and I have $500 in mine, Quicken will show a $1,200 checking balance.

Any ‘Fun $’ purchase comes out of Checking, then I move the same amount from the savings goal into checking and the net effect is that ‘Fun $’ was reduced, and checking appeared to stay the same.

Also… I don’t want to deal with categorizing transactions from long ago. If I sign up today, can I just pull in information from 1/1/11 forward?

Thanks!

Matt,

It will pull in historical data I believe, but you can just ignore it. If you’re satisfied with Quicken, I don’t know if I’d bother.

slug

I tried Mint but it couldn’t categorize the purchases I made with my debit card. It seemed easier just to do everything myself. Plus, I don’t trust them with my info.

I’ve been using Mint for about a year or so now and I think it’s great! It has it quirks and since it’s free, the customer service sometimes can take a long time to get back to you if you have an issue (sometimes I think my requests get lost). But if you can put up with that then Mint IS a great tool for quickly keeping track of your personal finances and analyzing how you spend your money. If you have a smart phone, then you can download and categorize transactions wherever you are in just a few seconds which is very convenient!

Jonathan,

I’ve been using yodlee.com ever since your recommendation several years ago.

I read reviews about mint.com and checked it out when it first came out, but I remember getting the impression mint was a prettier site but not as robust as yodlee and didn’t give it a second thought. Things like yodlee could connect to certain accounts that mint couldn’t, etc.

Have you now switched over completely to mint.com? Would you now recommend mint over yodlee?

btw – you said yodlee’s development slowed. They completed a major upgrade not too long ago, I assume in response to mint, as the site is now somewhat “prettier.”

You don’t need to worry about giving mint your data if you use one of the big banks, it uses Yodlee for logins which most major banks already use for there login systems

@Dan – I still use Yodlee through Bank of America as my primary data aggregator, as they include a larger amount of sites including rewards points, etc. I definitely think Mint has better budgeting features, the upgrades I’ve seen on BofA Yodlee are not nearly as good.

@Bryce – Since being bought by Intuit, I don’t think Mint uses Yodlee for logins anymore. I’d say Intuit is also well-respected around financial institutions.

Mint.com has some issues, mostly dealing with tracking investments (they’ve got serious issues with that tool, just check the online discussion forums and you will see many, many issues, some of which go back for a year).

As for tracking spending, Mint.com has been pretty solid for us. We’ve used it for about 18 months or 24 months. If you use it, check “Uncategorized” transactions regularly so you can place them in the right categories (and set up rules).

Also, they do not have a simple “Delete” transaction option – I have had need for that when a transaction that Mint attributed to my AmEX card never, ever occurred (on the AmEx card or any other card, check, etc.). No way to delete that from Mint’s data entirely, you can only “Exclude” it. So when Mint creates bad data, you are stuck with it.

This is the worst advice you could give to someone who needs to be on a budget. Using cash is an immediate way to limit spending. Using virtual cash allows those lacking will-power to overspend.

I managed to get my American Express cards up, but when I tried for my USAA credit card (Visa or Master Card), nothing clicked. Mint.com seemed to think I was referring to the USAA Bank. I don’t want to put up my bank accounts.

Is it always so difficult to enter credit cards?

Thanks.