![]() The U.S. Department of the Treasury announced the national launch of myRA (my Retirement Account), a new starter option for those who don’t have access to a retirement savings plan at work. There have been some improvements and tweaks since their initial pilot launch in late 2014.

The U.S. Department of the Treasury announced the national launch of myRA (my Retirement Account), a new starter option for those who don’t have access to a retirement savings plan at work. There have been some improvements and tweaks since their initial pilot launch in late 2014.

No monthly or annual fees. No minimum contribution requirement. No minimum balance requirement. Contribute as little as a dollar every paycheck if you like.

Fund via automatic paycheck deduction, automatic bank transfers, or federal tax refund. Automatic paycheck deductions work through your employer’s direct deposit system.

No risk of loss. Your money is backed by the US government, just like US Treasury bonds and FDIC-insured bank accounts. You earn the same interest rate as the Government Securities fund available to Federal employees, known as the G Fund. The good news is that it earns the higher interest of longer-maturity bonds while maintaining zero principal risk like a bank account. Interest is compounded daily.

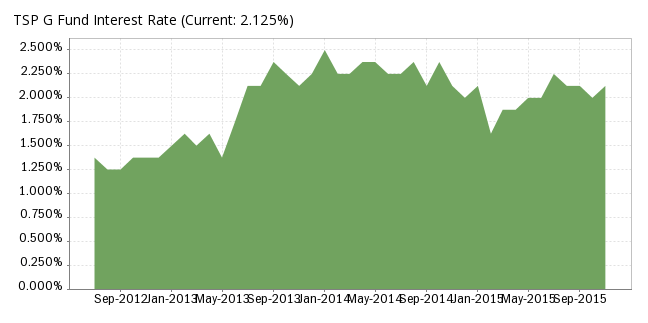

The G Fund 1-year historical return for 2014 was 2.31%. Taken from TSPFolio, here is the interest rate history. The current annualized rate for November 2015 is 2.125%.

What does “starter account” mean? There are no stocks or other riskier options here. You can roll over your myRA into a private-sector Roth IRA once you’ve either reached the max balance of $15,000 or the max time period of 30 years.

What do you mean it’s a Roth IRA? I mean just that; it is a Roth IRA. The same rules apply:

- Tax-fee and penalty-free withdrawal of contributions at any time, if needed.

- If you make a qualified withdrawal, you’ll pay no taxes on both contributions and earnings.

- For 2015, the contribution limit per person is $5,500 a year, or $6,500 if you are at least 50 years old by the end of the year.

- The income limit is based on modified adjusted gross income (MAGI). The 2015 phase-out range for singles is $116,000 to $131,000. For married filing jointly is $183,000 to $193,000.

Although you may not be the target audience, you can still use myRA if you have a 401k or previous IRAs. Again, myRA is a Roth IRA so you’d have to direct part or all of your annual contribution to this Roth IRA instead. The G Fund is something that I would invest in if it was an option for me, but it is somewhat inconvenient to open another account just for one investment option. For example, if you are 90% stocks and 10% bonds, a $5,000 total contribution would only direct $500 towards a myRA.

Commentary. As I noted when it first came out, myRA is kind of a Frankenstein cobbled together from the parts bin. Existing Roth IRA vehicle. Existing Thrift Savings Plan G Fund. Comerica Bank quietly manages the backend (they’ve done previous work for the Treasury). It’s a bit clunky as you have to tell your employer to direct deposit some of your paycheck into your myRA, which a is basically a Comerica bank savings account and routing number (111925074). If you employer can’t handle split direct deposits, you must contribute via bank transfer or tax refund.

Will this combo convince someone who’s not saving today, to start? My guess is that the popularity will be relatively low. While I personally wouldn’t mind having the G Fund as an investment option, but I don’t know that someone who’s not saving now will be enticed by a 2% interest rate. (Maybe if rates rise.) But hopefully I’m wrong and the opportunity to have a “retirement plan of your own” is enough.

To me, what’s missing is super-easy auto-enrollment (auto opt-in, voluntary opt-out). So the best case scenario is if small businesses without 401(k) plans actively encourage their employees to sign up for myRA, as we’ve seen that automatic deductions are a good trick to save more for retirement. For more information, visit the myRA.gov employer FAQ.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

For those that make too much to contribute to a Roth IRA, is there a way to do a “backdoor” myRA?

I believe that the normal process should be available, although you’d only get to keep $15k in your myRA at any given time. Contribute to non-deductible Traditional IRA somewhere, request rollover check, cash rollover check, send funds to myRA via bank transfer within 60 days. I don’t know if your initial broker would be too happy about opening an IRA and then immediately cashing it out, so watch out for fees.

https://www.irs.gov/Retirement-Plans/Retirement-Plans-FAQs-regarding-IRAs-Rollovers-and-Roth-Conversions

Also, is this for those who does not have access to a retirement savings plan at work? I contribute to 401K via my company but would like to contribute to myRA..is that possible?

As it is a Roth IRA, yes you can still contribute to a myRA if you have a retirement savings plan at work. From their FAQ Question #5:

I believe that you can contribute to this, as well as your 401k. The myRA uses your IRA space though (5,500 max), so for a competent investor, I don’t see any advantage of the myRA vs. a IRA.

@ Adam so if you are already doing max roth ira you can’t do this one too? I was thinking this myRA contribution was beyond roth ira?

Between I and my wife I was thinking of this as using my emergency funds.

From what I’ve read, you cannot max the roth ira and contribute to the myRA. The $5,500 max is for your combined contributions to an IRA or myRA.

So to sum it up, a myRA is basically a Roth IRA with a guaranteed low return. Probably no reason for anyone reading this site to use one.

Well, the major draw for starter savers is the fact that you can deposit as little as $20 a paycheck and have a “retirement plan” to call your own.

It could still be attractive if you already own short-term Treasury Bonds in a Roth IRA. Because that’s what this is, but with added principal protection, which like Jim said is useful *if* interest rates rise. Right now the yield on Vanguard Intermediate-Term Government Bond ETF (VGIT) is only 1.44% and if rates rise the share value will drop. You are limited to that $15k and you’d use up part of your Roth IRA contribution. If you would say most readers of this site already have a Roth IRA funded, or that it is mostly stocks in that Roth IRA, then yes it probably isn’t worth the bother.

Yes, the myRA *is* a Roth IRA. Just limited to what you can put inside, and always held in an account by Comerica Bank.

That 2% rate on a guaranteed principal is appealing. Especially with the looming risk of interest rate increases which will cause bond investments to lose value.

Have a question of the max balance of 15k. Does it mean 15k of the principal I put in or does it also include the earnings? I hope it’s only the principal as that’s be easier for me to control the balance, but if inclusive of earnings, it would be harder to control. Once 15k is reached/exceeded, the rule says “you will have to transfer or roll over your savings into a private-sector Roth IRA”. Is this mandatory? What if I don’t have an existing private-sector Roth IRA to transfer to? Can I simply withdraw enough principal so the balance stays below 15k?