![]()

Update 3/15/24: M1 just sent me the following e-mail:

We’ve decided to end our M1 Plus membership program. Our premium features will no longer require membership and will instead be available to everyone who builds and manages their wealth on M1.

Starting May 15, a $3 monthly platform fee will apply to clients with less than $10,000 in M1 assets or without an active Personal Loan. Each billing cycle will last 30 days—meeting platform requirements* at least one day during each cycle will ensure this fee is waived for you.

*You will be charged the $3 Monthly Platform Fee if at any point during the 30 days prior to program launch your total aggregate M1 Earn and Invest balances do not equal or exceed $10,000 or you do not have an active M1 Personal Loan.

This is basically free stuff for those with $10,000 invested, and a fee hike for all those with less than $10,000 invested and weren’t already paying for M1 Plus. I happen to be above the $10,000 balance threshold with my IRA contributions, but not an M1 Plus subscriber, and so the new “free” M1 Plus feature that I might take advantage of is the free custodial accounts for kids. I plan to give them the option for regular, dollar-based investments in Berkshire Hathaway shares (diversified, more gradual growth with no taxable dividends).

M1 continues their constant tinkering. They rolled out a rewards credit card linked to company stock ownership, which I don’t think really caught on. They started a checking account, and then shut it down. That’s too bad, because I still really like the core features of M1. They should really just own that they are the “Get Rich Slow” brokerage, as opposed to Robinhood as the “Get Rich Now!… or Lose All Your Money” brokerage. I mean, how many M1 screenshots have you seen that look like this:

If M1 offered excellent customer service (maybe via live chat to save money), they could take funds from Vanguard as the go-to for DIY index fund investors. Vanguard doesn’t offer automatic fractional investments into ETFs. M1 does.

Original review, somewhat edited to be current:

I’ve tried out my share of robo-advisors, which always sounded nice in theory but I eventually became disillusioned as they kept generating lot of unnecessary taxes every time they change their model portfolios to chase the latest and hottest trends. My favorite service for those that want a little extra help is one where I can pick my own custom target portfolio, but the robo still does the hard work: M1 Finance. Here’s a quick rundown of what makes them different:

- Fully customizable. You pick your own target asset allocation “pie”. (You can add ETFs or individual stocks.) You can simply copy one of the many model portfolios out there, or make your own custom pie as you like. You have full control! M1 handles the tedious stuff, like rebalancing or dividing a $100 contribution across 8 different ETFs.

- No commissions. Free stock/ETF trades with a low $100 initial minimum for taxable accounts and a $500 minimum opening amount for retirement accounts. After your initial deposit any amount greater than $10 can be deposited.

- Free with $10,000 balance. Otherwise $3/month. Most robo-advisors charge an annual management fee of 0.25% to 0.50% of assets, or force you to own something bad, like a lot of low-interest cash. (Looking at you, Schwab…)

- Free dynamic rebalancing. All new deposits (and withdrawals) will be invested (or sold) dynamically to bring your portfolio back toward your target asset allocation. M1 will also rebalance your entire portfolio back to the target allocation for you with a few clicks (for free) whenever you choose, on demand. You don’t need to do any math or maintain any spreadsheets.

- Fractional shares (dollar-based). For example, you can just set it to automatically invest $100 a month, and your full amount will be spread across multiple ETFs. Dollar-based transactions were one of the advantages of buying a mutual fund, but fractional shares solve this problem. ETFs are also usually more tax-efficient than mutual funds.

- Real brokerage account with off-the-shelf investments that you can move out. Some robo-advisors hold special, proprietary funds that you have to sell if you ever leave, possibly creating a big tax bill. (Looking at you, Fidelity…) M1 is built on a regular brokerage account, so you can move your Vanguard/iShares/Schwab ETFs and stock shares out to another broker whenever you want.

M1 Finance checks off nearly all the boxes of my brokerage wish list. I suppose the only thing they could add would be to have the high availability of knowledgeable customer service of a huge company like Fidelity or Schwab. Otherwise, I really like their feature set and I have been putting my recent annual IRA contributions into M1.

If you want to invest in newer factor ETFs that focus on Small-Cap, Value, Momentum, or Quality factors like those from DFA and Avantis, or a mix of dividend-oriented ETFs like SCHD/VIG/VYM, their service makes it much easier to set up a portfolio mix of different ETFs.

M1 Plus features are now available to everyone. M1 Plus was their premium subscription tier with several additional perks. Now everyone gets these features, but they are only free with a $10,000 balance and $3/month otherwise.

- High-yield savings (currently 5.00% APY as of 1/10/24). FDIC-insured up to $5 million.

- M1 Owner’s Rewards credit card (2.5%, 5%, or 10% cash back at 70+ brands, no annual fee).

- Lower interest rates on margin borrowing (1.5% rate discount).

- Custodial accounts for kids.

- Extra 3pm PM ET trade window.

- Automated “smart” transfers.

$100 referral bonus. M1 has a $100 referral bonus if you open a new account with $10,000 and maintain it for 30 days. You’ll also get 6 months free of their M1 Plus premium service. Here are the referral bonus details. Here is my M1 referral link (thanks if you use it!) from which you must start opening your new account.

A bonus that amounts to 1% of your initial deposit with only a 30 day hold is technically a 12% annualized yield. This is also better than their standard offer for a $10,000 new deposit (see below), and you can also consider the ACAT transfer and retirement rollover promos below.

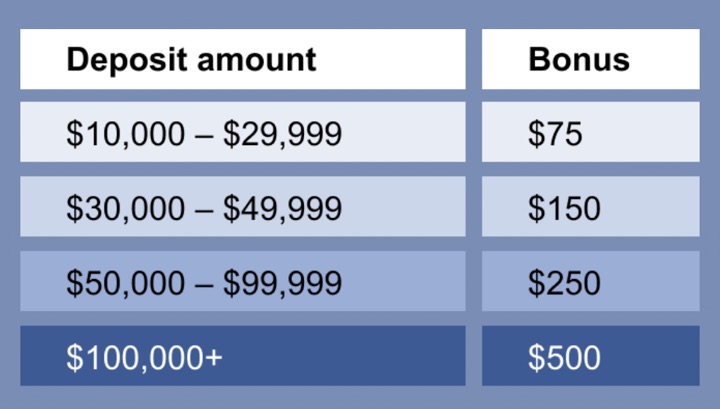

Up to $500 New User deposit bonus. Deposit $10,000 or more within two weeks of opening your new M1 Brokerage Account and get a cash bonus of $75 – $500 deposited to that account. See deposit bonus promotion link for full details. Currently set to expire 12/31/2024.

Up to $20,000 ACAT Transfer bonus (EXPIRED as of 3/31/2024). Up to $20,000 if you transfer brokerage assets via ACAT to M1 by 3/31/2024 (now expired). See ACAT transer promotion link for full details.

Up to $5,000 Retirement Rollover bonus (EXPIRED as of 3/31/2024). Up to $5,000 if you roll over your 401(k), 403(b) or another employer-sponsored retirement plan in an M1 Traditional/Roth IRA account by 3/31/2024 (now expired). See this Retirement rollover promotion link for full details.

Bottom line. M1 Finance is a brokerage account that acts like a customizable robo-advisor with automatic rebalancing into a target portfolio. You control the model portfolio, and they do the tedious work. Great for implementation of a low-cost, index or passive ETF portfolio. New pricing structure as of May 15th, 2024: Free for those with $10,000 in assets, otherwise $3 a month.

Disclosure: If you use my referral link, I may be compensated if you click through my link and open a new account.

Also see: Big List of Free Stocks For New Commission-Free Brokerage Apps

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

Any idea how they may money?

All that is laid out in Jonathan’s well written article.

Errr….any idea how they make money?

Here is what i found in their website

https://www.m1finance.com/blog/how-m1-makes-money/

1) Interest on idle cash (can be minimized as you can auto-invest all idle cash in the investment account)

2) M1 Borrow (margin loan interest)

3) M1 Spending (a banking product with a debit card that generates fees for them)

4) Payment for order flow (same as Robinhood and TD Ameritrade)

5) M1 Plus (premium subscription that gets you higher interest rates and debit card cash back).

You forgot the securities lending!

I’ve been seeing this from certain brokers, but do you actually earn any money from the securities lending? Especially if you just own ETFs? I can see maybe if you own a lot of a hard-to-find stock people are looking to short.

Good question, I have added my comments to the original post.

I’m not understanding the value add is. Vanguard already allows you to enjoy fractional ownership. I can chose to purchase $3.23 of VTSAX and they will let me. On the flip side, I can choose to sell $10.07 of VTSAX and they will let me.

I can evaluate my portfolio for free with Excel + Mint or with Personal Capital. KISS (keep it simple stupid).

Am I missing something?

The main value add is that you can now manage a more complex portfolio of up to 500 ETFs (not that I recommend that) without having to do all the trades yourself. You could have a portfolio with Value ETFs, Small Value, International, Emerging Markets, High-Yield Bonds, Municipal bonds, etc and it will rebalance for you regularly and with all new cashflows. You don’t need Excel or to place any trades yourself. Also, I can use any ETF from any provider, for example I happen to like the Schwab TIPS ETF more than the Vanguard alternative.

Between Vanguard mutual funds vs ETFs, a smaller factor is that some Vanguard ETFs are now cheaper than their Admiral shares, and I suspect that number will only grow bigger with time. ETFs have lower internal costs for Vanguard and in order to compete with iShares and Schwab, they are no longer sharing those cost savings with Admiral shares.

I tried them out a few weeks ago by coincidence. The value add for me comes a couple of ways… in the filters. I like being able to go in and screen for stocks with at least 3% dividend. You can’t buy fractional shares at vanguard. You can buy fractional etf shares, but not stocks. So say I want to build an “pie” / personal etf of 15 stocks paying 4%…I go in and choose them, make a pie, and each time I put money in its invested across the individual stocks I personally chose for my pie. You can choose what percentage each stock will have in your pie. If you want amazon to be 10% of your pie and Phillip Morris 5, it invests accordingly and rebalances.

For me another value add is not being dragged down by some of the stocks that are put in an s&p 500 fund automatically. Maybe their are overpriced and have dragged down the dividend a vanguard fund like VOO is now paying because AAPL has gone so high. Maybe they are just about to be delisted.

You have mentioned about My Money Blog Portfolio pie. If you make any changes to the pie % allocation or change ETF in it, will it get reflected in the portfolio of whoever using it?

I don’t think so, it’s not an “Expert Pie”, I think it just serves as a starting point for your own custom pie.

Any ideas about “secret” fees? I asked this question in your “Public review” post.

Jonathan,

Do you ever get nervous about the thought of sending your life savings to one of these new start-up brokers?

As long as I verify that they are an SIPC-insured broker, then it’s the same as sending money to a FDIC-insured bank. I might not move all my assets over because I am not sure of their customer service, but less about my money disappearing or something like that.

Is this an option for retirement accounts too?

Yes you can open IRAs with them. I used them for part of my 2019 IRA contribution.

They are giving $100 to transfer $20k+

M1 Finance Promotion Details

M1 Finance Bonus Account Transfer Amount

$2,500 $1,000,001+

$1,000 $500,001 – $1,000,000

$500 $250,001 – $500,000

$250 $100,000 – $250,000

$100 $20,000 – $100,000

IMO,

It is a good tool for playing around, maybe get a promotional offer or make some bucks from an affiliate link.

But, major brokerages are providing fractional shares now- fidelity, Robinhood etc and even the option of DRIP.

M1 finance has a great interface but the problem is you cannot invest less than $10.

Also, the pie investing is not for everyone, example- I have $5000 to invest at a certain given time, I only want to buy few stocks or ETF as some they may be trading low and avoid other in my pie as they are at all time high. so why would I invest everything in a PIE, I can invest manually in stock through M1 also but then what advantage pie gives.

I am planning to consolidate all my account for ease of maintenance, even with personal capital I dont get a clear picture of the portfolio when you have so many accounts.

Planning to consolidate in Fidelity for a great interface and same/free pricing.

The biggest thing with M1 Finance is that *I* get to pick the target asset allocation. M1 just does the boring stuff, like rebalancing or dividing a $100 contribution across 8 ETFs. If one of the full-featured brokers offered such a service, I would be happy to see it.

What is the minimum amount you have to put into your pie once you have the initial $100 dollars? Thinking of doing it for my kids and sometimes they only have $20 or $30 dollars to put in. This sounds like an awesome platform if they could put that whenever they want and it would automatically distribute it across their chosen ETF’s. Thanks.

Edit: $10 is the minimum additional deposit. $1 is the minimum purchase amount for each security inside a slice. $25 is the minimum auto-invest size (they will wait until your cash balance accumulates to at least $25 before making an automatic investment.

That’s a good idea, although for my kids I might pick some names of companies they know instead of ETFs. Disney, McDonalds, Amazon, or perhaps Berkshire since I’d like them to know about that too.

2% loans! I know it will fluctuate but assuming rates stay low for the near to medium term, I might “refinance” into this for a mortgage I was planning to be able to pay off in 5 years anyway. It’s risky but since I can cover the loan by selling other assets in a pinch I’m seriously thinking about leveraging with this loan. Also, margin interest is fully tax deductible unlike the caps on mortgages. What do you all think?

The 2% loans really jumped out at me too. I’d consider it for a car loan, but if the numbers work for your mortgage, that could be a good option, too. It’d be great if it provides quick access to funds without the overhead / transaction costs of other financing, and at a lower rate.

According to M1 “Exchanges make money in part through matching buyers and sellers at the ask and bid respectively and pocketing the spread” and this is sort of the way they make money using “order flow”. Maybe I’m uneducated but I thought that market makers, not exchanges, match buyers and sellers and pocket the spread because it’s actually them that buy at the slightly lower price and sell at the slightly higher price, not the exchange itself. Are they just conflating the terms exchange and market maker to try to simplify their answer or what?

I love M1. I’ve been very happy with the way my pie was done. My picks are doing well.

Looks like they don’t offer any money market funds for storing cash temporarily…

They do have an M1 Spend account that is FDIC-insured and currently pays 1% APY. That is actually much higher any money market fund that I know about right now.

However, I personally use M1 to minimize the idle cash via fractional shares and automatic dividend reinvestment to keep things fully invested automatically. I manage my cash needs elsewhere.

Interesting. Unfortunately, it looks like you have to pay $125/yr to get that 1% rate (thru M1 Plus). Might still be worth it if you have enough cash though (it’s like earning 1% on everything beyond the first $12.5k deposited).

The fee for the first year is a reduced $25

Gotta say, this is EXACTLY what I’ve been looking for. No brokerage (other than the now defunct Motif) would let me set up MY OWN asset allocation and automatically rebalance.

If I can set up an 401K, Roth RO1K, etc., these guys may get all my business.

Look the transfer deadline is 5/31/2020

Thanks, M1 sent me an email that they are extending the promotion to at least June 15th.

Jonathan,

I don’t think there is “automatic” rebalancing done by M1Finance in the general way we think about it(at least, I think about it)

– Rebalancing happens when new money is invested – by investing more in into under performing stocks/ETF’s to bring the allocation back to target

– Rebalancing done when we clink on the “Rebalance” and initiate rebalance

So, if I leave the account without any new investments for couple of years, there is no quarterly/annual rebalancing initiated by M1Finance to reallocate to bring my assets back to my target allocation. This to me is fully automatic rebalancing.

One nice feature I liked with manual rebalancing is, we can rebalance either a specific Pie or entire portfolio.

In any case, I have been using M1 for about an year now and like it.

I really like m1 filters.

Two downsides for me…

Yes, as you mentioned…customer service.

Second is not being able to choose buy price. It’s good for dollar cost averages, but buys go in first thing in the morning. If I’m building positions, I’d rather go in and buy at intraday lows. Especially if I am going to throw 100k plus in to get a bonus.

If you’re not actively managing your money and just want to put like a thousand bucks in the market every month, dollar cost average in to an etf you build yourself, I think m1 is fantastic. To counter their once a day buy, I think I would sit on cash, wait for a couple of down days and then have m1 move your cash into your etf on those days.

Looks like they’re back to their typical bonus amount already ($3,500 at the high end, $40 at the low end).

If you go through the promo link, the fine print on the bottom says good for transfers requested through 2/14/21.

They only place orders at market open unless you pay for Plus, i think that’s the big negative. Who wants ot place orders right at the open?

Can’t wait to see the performance of the my money blog portfolio. It looks like a good selection of stuff. That should do well.

M1 has become trash. They randomly start supporting various ETF based on some algo they have without nary an in app notice.

It also takes days to transfer money even after settlement so you can’t even schedule back to back transfers until a trade completes and transfers.

And the worst part is the lack of transparency in trades. They seem to always get horrible price execution.

Jonathan,

A good review – thank you.

M1 seems like a good platform. They were doing a “put in $10, get $100” deal a few months ago. The current terms just don’t seem that compelling.

Just spoke to rep and they said you need to deposit 5k for the $100. Do you have a referral code I can give them to reference your special promotion?

There’s a referral link in this post above, does it not work? I haven’t had time to try yet.

Referral link works but rep says the deposit has to be 5k not $100

Thanks for bringing this to my attention, I contacted M1 and it does look like they quietly increased this minimum funding amount from $100 to $5,000. The text “There’s $100 waiting for you! Just sign up and fund your free M1 account.” with no additional qualifications is very misleading. The landing page used to look the same, but the funding requirement was simply the minimum required to open an account in general ($100), as is a reasonable assumption in my opinion. I think it’s a bit tacky that they didn’t clearly mark this on the referral landing page. Anyhow, I will edit the post.

How does this work with assets you hold with non-M1 accounts such as your current employers 401K? Does it take those balances into account when determining your current portfolio mix?

No, it only goes toward a target pie that you set and does not automatically adjust for holdings in external accounts. I don’t know of any robo-advisor that does.

Hey Jonathan,

After much back and forth with M1 they not only changed the terms as I mentioned previously, but after depositing the 5K they are only providing a $10 credit not the $100 credit stating a signed up with an affiliate rather than a referral promotion (their response in quotes), even though the landing page clearly stated $100 for 5k. Maybe I can get this escalated to get them to do whats right, but thought you’d like to know since you are an affiliate and are recommending the M1 Finance site. This type of bait and switch is pretty egregious (first they changed the $100 deposit to 5k deposit then the award from $100 to $10).

“Hi David,

Thanks for getting back to me.

Since you signed up via an affiliate link, not a referral link, you received $10.

When you referred a friend and they met the terms and conditions, both parties received $100 on 6/1/23.

You have received all eligible promotional credits.”

I’m sorry to hear that. I’m also at mercy to their tracking system, and I don’t think I’ve gotten a single $100 referral from their previous offer either. I hope you can reach a good resolution.

No resolution. I had to talk to them multiple times just to get the $210 out of $300 owed (Referred my wife). It appears nothing with the referral system at M1 seems to be working. I was planning on keeping one of the M1 accounts long term, but with such poor customer service to right an obvious wrong I have closed both of the accounts.

Yea I signed up with Jonathans referral link & transferred $100 on 04/12/23. 75 days later and it’s still at $100 balance. Definately bait & switch.

M1 is a scam. They pull a bait and switch with their bonuses. Their lack of limit/market trades, and the once/twice a day trade window is a cracket, to literally suck money off their clients. I’ve done dozens of referral bonuses for Jonathan over more than a decade through this site. This one is a bridge too far.

M1 is a nice robo-advisor and has a very nice margin loan feature, but I don’t like how they just up and change the pricing and terms of these products all the time. They closed my checking account with little warning, as an example. Now they’ve added this new fee. Not particularly thrilling. I’d stick with a real boomer brokerage (Schwab, Fidelity, Vanguard) for the core features they offer over centralizing at M1. It’s just not quite there yet but it’s a nice place to have a self-defined roboadvisor.

Their credit card is also very … bad. I mean, there’s no sign up bonus. It’s also the only credit card that has a MAXIMUM you can earn for rewards per month…

“1.5% – 10% Owner’s Rewards cash back earned on eligible purchases subject to a maximum of $200 cash back per calendar month. Cash back rates of 2.5% – 10% require an active M1 Plus subscription (billed at $36 annually or at $3 monthly).”

That’s right! This card earns 1.5% as a base rate, but that is ALSO subject to the rewards maximum. What a dumb card program. I’d rather they just offer something like the Fidelity Visa that earns 2% rewards but auto-invests the rewards every month into my pie. That would be a great feature. Instead they have this dumb rewards structure that makes the card effectively worthless to me.