Updated. Let’s say you are fortunate enough to be able to make a large contribution to a 529 college savings plan, perhaps for your children or grandchildren. You read from multiple sources that you are able to contribute up to $75,000 at once for a single person or up to $150,000 as a married couple (2018), all without triggering any gift taxes or affecting your lifetime gift tax exemptions. (From 2013-2017, these numbers were $70k/$140k). What you are doing is “superfunding” or “front-loading” with 5 years of contributions, with no further contributions the next four years.

Updated. Let’s say you are fortunate enough to be able to make a large contribution to a 529 college savings plan, perhaps for your children or grandchildren. You read from multiple sources that you are able to contribute up to $75,000 at once for a single person or up to $150,000 as a married couple (2018), all without triggering any gift taxes or affecting your lifetime gift tax exemptions. (From 2013-2017, these numbers were $70k/$140k). What you are doing is “superfunding” or “front-loading” with 5 years of contributions, with no further contributions the next four years.

Those are pretty big numbers, but any contribution above $15,000 will require you to file a gift tax return because that is the annual gift tax exclusion limit for 2018. ($14,000 for 2013-2017.) You’ll need to fill out IRS Form 709 [pdf], “United States Gift (and Generation-Skipping Transfer) Tax Return”. The instructions are quite long and confusing. You ask your accountant and they suggest talking to your estate lawyer. You may wish to avoid paying the $400 an hour or whatever it will cost as the form should be pretty straightforward.

So how do you fill out form 709 for a large but simple 529 contribution? Here are the resources that I found most helpful:

- IRS Form 709 Instructions, section on Qualified Tuition Programs.

- Preparing Gift Tax Returns (2012) – Boston Bar Association (PDF)

- YouTube video and Powerpoint presentation: 10 Biggest Mistakes made on Gift Tax Returns (by an estate attorney, 529 stuff starts at 43:25)

- Barack Obama’s Form 709 (2008)

- SavingForCollege Sample 709 Part 1, Part 2

- Bayalis is the Answer 529 Guide

(Note that I have found what I consider minor errors and/or inconsistencies in some of the sample 709 forms above.)

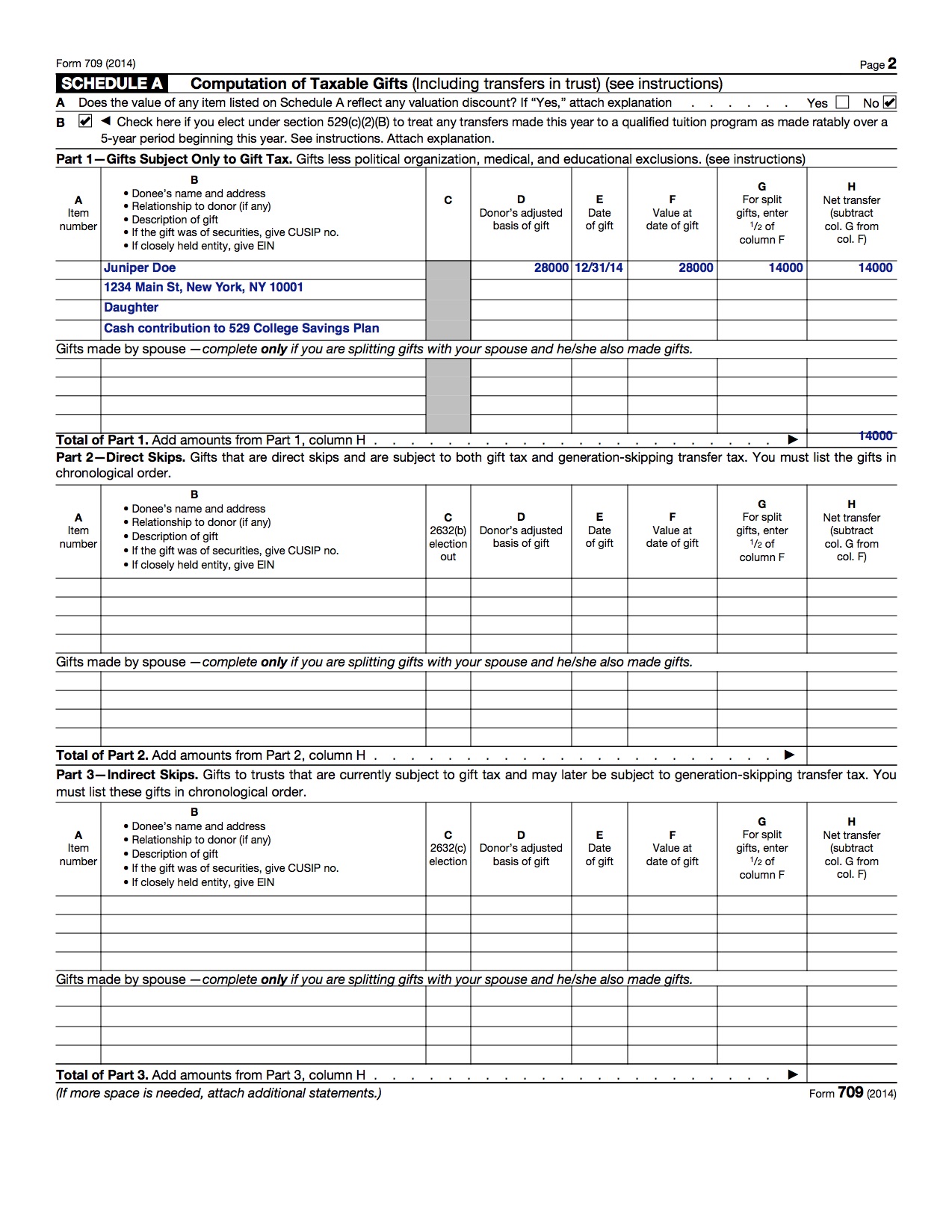

Here’s a redacted version of my completed Form 709. Let me be clear that I am not a tax professional or tax expert. I am some random dude on the internet that did his own research to the best of his abilities and filled out the form accordingly. This is what my form looks like. It could be wrong. You’ll need to make changes to conform to your specific situation. Feel free to offer a correction, but please support your statement.

For my version, I am assuming that you and your spouse contributed the maximum $140,000 together. (I didn’t actually contribute that much.) The 2014 form is shown below, but I just did this for another kid using the 2017 form and I couldn’t find any differences. Note that you’ll need to file two separate gift tax returns, one for you and one for your spouse. Mail them to the IRS in the same envelope, and I like to send them certified mail.

Here is my Form 709, Schedule A, Line B Attachment

Form 709, Schedule A, Line B Attachment

– Donor made a gift to a Qualified State Tuition Program (a 529 plan).

– Total amount contributed $140,000 in 2014.

– Donor elects pursuant to Section 529(c)(2)(b) of the IRS Code of 1982, as amended to treat the gift as having been made equally over a 5-year period.

– The gift was made jointly by the taxpayer and the taxpayer’s spouse on January 1st, 2014 and will be split equally in half.

– Election made for $140,000 over 5 years is equal to $28,000 total per year, or $14,000 per person per year.

– The contribution is for

Juniper Doe

Daughter

1234 Main St

New York, NY 10001

When to file Form 709. When taking the 5-year election, you must fill out the gift tax return (Form 709) by April 15th of the year following the year in which in the contribution was made. So if you make the contribution in 2018, you must file Form 709 by April 15th, 2019. If you make the upfront contribution in the first year and then make no future contribution in the next four years, you do not have to file a gift tax return after the one you did for the first year.

What if you’re late? Well, you should file the Form 709 as soon as possible. If you did not exceed the limits then technically there is no gift tax due, and there is no penalty that I could find for late filing when there is no taxes due. Still, I would file ASAP.

The tax information set forth in this article is general in nature and does not constitute tax advice. The information cannot be used for the purposes of avoiding penalties and taxes. Consult with your tax advisor regarding how aspects of a 529 plan relate to your own specific circumstances.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I have a question regarding 529 plans…

I have 2 kids, ages 7 and 4. I want to contribute to a 529 plan, but not sure if I should put it in my name or theirs. If it is in my name, I could perhaps give it to a niece or nephew should one or both my kids not attend college. If it is in the kids names, I presume I could pull it from one and give it to the other, but I’m just not sure how that all works. There is also the issue of financial aid. (If the 529 plan is in my name, does that make it easier for them to get financial aid and then I could transfer it to their name?)

I’ve yet to see an article discussing the best plan of attack for 529 plans.

Thanks for this post. I’m confused here, though. We have 529s for both our children. My understanding was that ownership of these accounts lies with the account holder and the children are beneficiaries. In other words, they count as our (the parents’) assets for the purposes of calculating financial aid and other net worth tests, and remain in our estate. As a result, I don’t understand why contributing to them could possibly be considered a gift and trigger this kind of IRS filing. What am I missing?

Thanks.

I am confused as to why you needed to file this. You get $14k per spouse. Why did you have the $28k come from one spouse rather than $14k from each spouse thus negating the necessity for the form?

Based on my experience, this whole article seems misleading to me. 529 accounts are taxed by owner, not beneficiary. So this gift tax only applies if someone like a grandparent gives an account owner like a parent a large sum of money to invest. Otherwise, you just put the money in a 529 account under your name as the owner and you’re done; no forms required. Or did I miss something?

@Maury: The account should be in your name. Then you control the money and can decide where you want it to go. You must designate a beneficiary, but you can change that along the way if needed (say your first child gets a big scholarship and doesn’t need all of the funds you set aside for them, so you redirect them to you second child).

RE: Andy, TJ

The reason for the IRS Form 709 filing is because the gift was actually for $140,000.00… This is called “superfunding” for 529s. A special rule for 529s permits you to make up to 5 years worth of annual gift exclusion transfers in a single year. So $14k per parent = $28k x 5 = $140k. After making this gift, you cannot transfer any more money for 5 years without incurring a tax. Why would someone superfund? Because that gives you 5 years of tax-free gains on a larger principal. Consider $140k @ 6% for 18 years compounded annually is ~$400k.

RE: Scott

529s are generally setup as “account holder” and “beneficiary”, with the parent being the account holder and the child being the beneficiary. This allows the account holder to make the decisions about how the money is used and invested. However, TRANSFERS TO A 529 ARE TREATED AS GIFTS TO THE BENEFICIARY, thus the need to be careful of the gift tax limit (currently $14,000).

Does anyone have sample of 709 using lifetime amount as portion of 5.3M?

Basically I like to use 709 to report a gift value off $200K and not pat tax , as it will be part of $5.3M lifetime.

I need a sample form of a 709 where a husband and wife give $70k to children for towards the purchase of a home.

I provided detailed guidance on both of these scenarios below.

Hi,

Thanks for uploading this form. Seeing as this is the only place on internet where such a completed form is available, I can’t thank you enough for the time and effort it saved me. That said, a few minor questions/remarks:

– It would have been great if you filled in the SSN and signature fields (with fake values of course). Leaving some required fields blank means that the rest of the blank fields become suspect – should we fill them or not?

– Why is total number of donees (line 10 of page 1) 2 and not 1?

– The form says that if 11(a) is answered with a “No”, 11(b) must be skipped. You did not skip 11(b)

– What about the “Gifts made by spouse —complete only if you are splitting gifts with your spouse and he/she also made gifts. ” section in part 1? Why did you not fill it? And if we fill that part, do we still need to complete two separate forms (one for each spouse) or is just one form enough?

EDIT: Actually the instructions form for 709 is clear that we can’t file gift tax returns jointly. “A married couple may not file a

joint gift tax return. However, if after reading the instructions below, you and your spouse agree to split your gifts, you should file both of your individual gift tax returns together (that is, in the same envelope) to help the IRS process the returns and to avoid

correspondence from the IRS.”

Thanks,

P

Total number of donees should be 1 and not 2. I was editing my personal sheet which had 2 donees and made an error. If you only have one donee, then the form should note that. I will have to get back to the other questions.

I have updated the first page of my sample form 709.

– Filled in SSN with fake numbers

– Corrected total donees for sample case (one listed on sample form)

– Skipped 11(b), left it blank instead

– Added reminder for consenting spouse to sign and date

When filing a Form 709 to report “superfunding” a QTP for a grandchild, do you also need to complete Part 2 of Schedule A to report this as a “direct skip”? Technically it IS a “direct skip” as an outright gift to a grandchild, BUT since it is sheltered by the $14,000 annual exclusion, is it also technically reportable in Part 2 as a “direct skip”? Can’t find an answer or example that addresses this in the IRS instructions. Obviously no tax due, but I have an aversion to “over-reporting” anything.

I answered your question in my detailed post below. Best wishes!

Thank man. I appreciate it! I’m not sure why they make such a simple act so complicated to fill out. You saved me hours.

Glad you found it useful. That was my goal in writing this post.

Like the other said: Thank you so much!

I swear it feels like my reading comprehension gets downgraded to “idiot level” when I have to read the IRS instructional booklets. I just can’t seem to make sense of their explanations.

On the other hand, I appreciate your ability to explain the 709 form in a straight-forward manner. So helpful.

Thank you sir!! I am glad someone took the effort for the rest of us to post a sample form. I have filed a 709 for a similar gift split for childs education fund with spouse and am filing one this year too.

May be as an extension, could you add how your NEXT years form 709 would be if you were in a similar situation of having split 28k between your spouse and yourself again. I was struggling filling out schedule B (which you left empty as you indicated never having filed a gift tax before) especially columns c and e. If I understood correctly, column E refers to taxable gifts. In situations like yours (and mine), it would be zero and not 14k even though you gave 14 k out to your child. My reading of column C, “Enter the applicable credit against tax allowable for all prior periods” was similarly the amount of tax calculated for those taxable gifts. So also zero. Am I right?

thanks

I provided an answer to this question in detail in my post below. Good luck!

Thank you for the detailed explanation !! I didn’t understand how it works until I saw it here. Here is a link to site that also explains how to fill out the 529 plan – it mirrors what this blog said as well – so it is confirmed.

http://www.bayalisistheanswer.com/hitchhikers-guide-529-superfunding/

Thanks for sharing, it’s always good to have agreement.

Does anyone have sample of 709 using lifetime amount as portion of 5.3M?

Basically I like to use 709 to report a gift value off $50K and not pay tax , as it will be part of $5.3M lifetime.

I answered your question in my detailed post below. Best wishes!

Nina: I’ve been looking around as well and no one does. Everyone just mumbles out an answer. Some mention unified credit, but that word isn’t mentioned anywhere on the form.

This is also why they go with easy numbers like 14000 that cancels out by annual exclusion.

I answered your question in my detailed post below. Best wishes!

I’ve been debating whether to superfund our 529s and the remaining question has to do with state tax benefits. In my state I can deduct up to $20k annually for funding 529s. But if I superfund, do I lose the ability to deduct that for the 4 years following the initial superfund?

I answered your question in my detailed post below. Best wishes!

I’m a CPA and Enrolled Agent. I had a friend reach out to me regarding many of these same issues and forwarded this page along as a reference. In discussing these issues with my friend, I thought I would add some guidance free of charge. Here goes.

Johnathan-

You are pretty close and I commend you for your effort. To fellow readers, please don’t file your return this way. It can be very, very confusing; I understand.

You and your wife should each file Form 709 for $14,000 apiece, assuming you are contributing cash owned jointly. You will only do a gift split if you gift a piece of property YOU own SEPARATELY from your spouse and you want to consider it as 1/2 from you and 1/2 from her. In that event, you would still need to each file your own Form 709. Columns D, F & H would be $14k on each spouse’s return with column G left blank. (NOTE: This amount has since increased to $15,000 and will continue to increase periodically.)

A by-product of this is that on page 1, Part 1; lines 12, 13 & 14 should be left blank.

Other Notes:

*The information Mark’s 8/31/15 post is correct.

*Regarding Richard’s 2/5/17 post, the short answer is no. If YOU set up the 529 plan for the grandchild, YOU own it for the benefit of the the grandchild. No GST. If the 529 is established by the grand child’s parents and you merely contribute to it, there would still be no GST (generation-skipping tax). The owner would be your child (or son/daughter-in-law) for the benefit of the grandchild. Therefore, the gift technically only goes down 1 generation. The GST is triggered at the 2nd generation and beyond (or various other rules for non-family donees.)

*Regarding Kris’ 4/15/17 post, the answer is that you more than likely don’t need to file the Form 709 for the following 4 years. If you made other gifts that would trigger the need to file a Form 709 in any of the following 4 years, only then would you file a Form 709 Gift Tax Return. In this scenario, any 709 filed over the next 4 years would show the $14,000 for that year in addition to the other gift that caused the need to file the return. They would both be shown. Most importantly, if you didn’t make any other gifts above the $14k threshold (note: this amount is now $15,000) in any of the following 4 years, no gift tax return is required. For most who superfund, they only have to file the initial return because they don’t give gifts above the threshold in the following years.

Regarding Nina and Rep’s posts, I simply don’t have the time to fill out a sample and I don’t share client work; even if it is redacted. I will provide some general guidance though. Regarding the $5.3M “exclusion vs. the unified credit, I should first point out that the $5.3M has since increased to $11.18M. The unified credit is simply the tax liability that would result if the the amount of the exclusion weren’t excluded. Basically, if there was no such thing as an exclusion, a gift of $5.34M (example of 2015 exclusion amount) would create a tax liability of $2,117,800. Therefore, for 2017, the “unified tax credit” is $2,117,800. Instead of calculating your total gifts against that year’s exclusion, they instead calculate it as the tax credit that full exclusion allows. The form then calculates your tax liability as if there were no exclusion and the offsets that liability with the unified tax credit. It is confusing but it makes since to do it that way for reasons I won’t go into here. It has to do with carrying forward deceased spouses’ unused amounts, handling gifts in multiple years with differing exclusion amounts in each year, etc.

Now to the practical part. You’ll start with Schedule A, Part 1. You’ll enter $50k. You won’t have a split if it’s cash. If you want to split it, you and your spouse would each file a gift tax return at $25k or whatever you decide. All in all, column H will come out to $50,000. That carries to Part 4, line 1; which is shown on Johnathan’s 3rd page in the above example. Line 2 will show $15,000, assuming the gift was in 2018 and was all given to the same person. Line 3 will be the net amount, which is $35,000. If it was given to multiple people, they will all be listed on Schedule A Part 1 and Schedule A Part 4 line 2 will be $15,000 x the number of donees. On line 7 of Sch. A Part 4, you have to enter the TOTAL amount of charitable contributions for that year, net of the annual exclusion to each recipient. On Schedule A, you need to list every charitable contribution you made in that tax year. On line 7 of Sch. A Part 4, you will only include any amounts that exceed the annual exclusion ($15k for 2018; $14k for 2015-2017). If you didn’t give any single organization more than $15k (for 2018), line 7 will be $0. If you did, you will enter the total gifts to organization’s that exceed the annual exclusion. You’ll subtract line 7 from line 3 and enter that amount on line 9. This more than likely carries to line 11 and is then taken to Page 1, Part 2, line 1. Assuming no gift tax returns in prior years, this amount will then carry to line 3. If you made gifts in prior year, you’ll just put that on line 2 and get a net number on line 3.

FINALLY, this is where you calculate the gift tax (as if there were no unified credit; see my comments above). You’ll use the table on the next to last page of the Form 709 Instructions to calculate this tax. In your case, gifts of $35,000 would generate a gift tax of $5,100 using 2018 figures. Your unified tax credit, as described above will offset this amount. For 2018, the unified credit is $4,417,800 (which represents the “would be” gift tax on the 2018 exclusion amount of $11.18M). Your tax liability for 2018 would be $0. Your remaining unified tax credit would (theoretically) be $4,412,700 (which is $4,417,800 – $5,100). The reason I say “theoretically” is because this amount actually re-calculates each year going forward. If the tax law changes the credit amounts or gift tax rates, it will essentially calculate your gift tax liability on the $35,000 using the rate in place AT THAT TIME. They will then subtract that amount from the unified credit in place AT THAT TIME. There’s more to it than that but it’s the basic logic.

In response to Joe’s question on 5/10/18, the answer to that varies from state-to-state. It depends on what your state tax code allows. Another state will treat it differently. Even if I knew what state you are in, I probably wouldn’t know off hand and would have to look it up myself. Good luck.

NOTE: This does not constitute tax advice or a client relationship. It is for educational, illustrative and/or discussion purposes only. Please seek qualified counsel as needed regarding your own personal situation.

Thanks so much for the guidance.

You wrote “…A by-product of this is that on page 1, Part 1; lines 12, 13 & 14 should be left blank.”. Do you mean that Line 12 should be answered “No” and lines 13 to 18 should be left blank?

Thanks for the advice Jay.

I your computation you indicated gifts of $35,000 would generate a gift tax of $5,100 using 2018 figures. Should this be $7,100 from the table? e.g. 3800 + 0.22*(35000-20000)

Hi, I was reading the IRS rules on gift splitting and as I understand for 2022 the gift limit per year is $16,000 per person, $32,000 per couple. So if you’re superfunding $160,000 in 2022 for a couple, that’s spread ratably over 5 years (check the box on form 709), i.e. $32,000 per year, then as per the instructions below you an elect to split the gifts between the spouses in a single gift form 709 and the other spouse doesn’t need to file a separate form. Am I reading this correctly? Quoting from the IRS website:

In general, if you and your spouse elect gift splitting, then both spouses must file their own individual gift tax return.

However, only one spouse must file a return if the requirements of either of the exceptions below are met. In these exceptions, gifts means transfers (or parts of transfers) that do not qualify for the political organization, educational, or medical exclusions.

Exception 1. During the calendar year:

Only one spouse made any gifts,

The total value of these gifts to each third-party donee does not exceed $32,000, and

All of the gifts were of present interests.

Exception 2. During the calendar year:

Only one spouse (the donor spouse) made gifts of more than $16,000 but not more than $32,000 to any third-party donee,

The only gifts made by the other spouse (the consenting spouse) were gifts of not more than $16,000 to third-party donees other than those to whom the donor spouse made gifts, and

All of the gifts by both spouses were of present interests.

If either of the above exceptions is met, only the donor spouse must file a return and the consenting spouse signifies consent on that return.

I created a sample 709 following Jay’s instructions:

https://fastupload.io/hn9TAEt16ey97Dq/preview

To clarify:

– If donation was made from a joint account, do NOT gift split. Copy https://fastupload.io/hn9TAEt16ey97Dq/preview

– If donation was made from an account owned by one spouse, do gift split. Copy the 709 in the blog post.

Jonathan, feel free to add this to your blog post.

Thanks for sharing! I’ve been meaning to update this post with more recent gift limits.

Regarding “superfunding” a QTP for grandchildren:

If a grandparent makes contributions to the parent-owned 529 plans of two grandchildren and parent (rather than each child) is considered the beneficiary, is the maximum 5-year exclusion amount allowed 150,000 total – i.e., 75,000 per child – instead of 150,000 per child? And is the parent who owns the 529 plan listed as the donee on the form – rather than each child? thank you in advance for any help you can provide

Sorry – I should have said if the parent of the two grandchildren is the Owner of the 2 accounts and each grandchild is the beneficiary of one of the two accounts – Who is listed as the donee – the parent or the grandchildren and if the parent is listed as the donee, does this limit the donors from depositing only 75,000 per child for the 5 year period to avoid incurring gift tax liability?

In Schedule A, Part 1, the Obama 709 also filled out the section “gifts made by spouse” but you did not in your example. Not sure I understand the difference between what you did in your 709 vs. what the Obama’s did. Just trying to figure out what I should do because my wife and I gave each kid $150,000 in 208.

I believe I’ve done something wrong on a 709 form as the IRS sent a recalculation letter saying my client owes $23,800!!! Synopsis is this: client gave her 2 children & 2 grands $40,000 each which came from a land sale. What could I have done wrong???

I made five different gifts to my son in 2018. How in the world should I be able to enter the donee’s name AND description of the gift [2 properties, a life Insurance, and 2 securities??? 🙁 Am at a loss a how to accomplish this. Or is it allowed to attach a page so that i have more space? I an a little old 82-year old lady and need all the help I can get too cope with this Form 709. Thanks, Chris

Hi Jonathan –

Thank you so much for your posts. I really enjoyed exploring your site and appreciated your guidance on the 709 Form in particular. Honestly, saved me hours and made me realize this really was the right decision for our family. Glad I am getting through all the paperwork. This was the only form that I have encountered that turbo tax does not cover. That alone, was interesting.

I spent a decade working for a credit card company and my net take-away was that it is no good to have an incentive to “spend”. Very slippery slope all those rewards programs….much better to have an incentive to “save” that is key to your personal goals. My 2 cents anyway…

Glad you found it useful!

I appreciate your perspective. I see nothing wrong with avoiding credit cards entirely, if that works best for you.

Hi Jonathan,

I have a question on this 709 form, based on 529 contributions. I have my 529 at Utah’s my529. I am the owner and my kids (two kids, I have two accounts with them – one for each kid). The plan doesn’t allow listing two owners, like me and my wife together. However, we file tax together jointly. In 2020 – we contributed 30K per kid to that 529 plan, so overall 60K (30K for each kid). As we file jointly – I split that 30K contribution (is that ok?) and in doing so – It’s within the allowed 15K/from one person to one donee/ year. SO with that understanding – we don’t need to file form 709. If you or anyone can confirm this that will be very helpful. I am not finding a confirming answer on IRS site or anywhere else. My concern is

1. is it’s ok to split the contribution across me and my wife, as we file jointly, even though the 529 account owner field only has my name in them (there is no means to have multiple names, to have my wife listed as well)

2. Is my understanding right that by splinting that way and we are within 15K per kid per parent – so we don’t need to file form 709.

Thanks

Richard

That’s a good question, and I’m afraid I don’t have a solid answer. The best I can say is that you may not be required to do so, but to be 100% safe you and your wife probably should each file a Form 709.

From Intuit Turbotax:

Thanks Jonathan,

I somehow missed that intuit article. I found now.

The whole point of limiting within 30K was to avoid the complexity with form 709. Looks like it’s best to have it filled, as that’s the only means to say it’s a split between me and my wife. To add to this looks like turbo tax doesn’t support form 709 and asks to download from IRS and file directly. Not sure if that means I cannot efile my tax return or if it can be e-file’d thru turbo tax and send just the 709 separately physically. More digging and not sure what other questions going to open up when filing form 709. Jonathan, want to thank you for responding, even though this thread/article is old – the content is still relevant. Appreciate sharing the experience.

Thanks

Richard

I wish there was a simpler option to indicate this as well, but filing the Form 709 isn’t really all that hard. It doesn’t have to be with your tax return. Form 709 is only for individuals, so you fill out one, it may be 1 or 2 pages. Your wife fills out one, again 1 or 2 pages. You stuff them both in a paper envelope and send it Registered Mail to have proof since the IRS won’t send you any acknowledgement. You keep a copy of the forms and the Registered Mail in case anything comes up in the future, although it probably won’t. In exchange, you get peace of mind.

Thanks Jonathan.

I share the same minset, for peace of mind, I decided to file 709. As you said and with content you have here – it’s not that bad to have the information filled on that form.

I have one final question though. For my case (where I contributed to kids 529, though from joint account – but the 529 is on my name with Kids being the beneficiary (one for each kid). So essentially my wife didn’t contribute. My contribution to each kid is 30K, so I file 709 to show that I share that 30K/kid with my wife, so its within 15K/kid/donor limit) and she consent with her signature (in my form). So in this case, as my wife didn;t contribute, I don;t need to file form 709 for my wfe. Its just my form. Atleast that’s how I interpret. Also the youtube video link you have (at time 13.48), went thru this specific case – where wife doesn’t need to file her 709, as she didn’t contribute. If you have time – can you pls share if you also see this the same way.

Again, appreciate you taking the time. I think this can help many. Thanks as always.

Thanks Jonathan.

I share the same minset, for peace of mind, I decided to file 709. As you said and with content you have here – it’s not that bad to have the information filled on that form.

I have one final question though. For my case (where I contributed to kids 529, though from joint account – but the 529 is on my name with Kids being the beneficiary (one for each kid). So essentially my wife didn’t contribute. My contribution to each kid is 30K, so I file 709 to show that I share that 30K/kid with my wife, so its within 15K/kid/donor limit) and she consent with her signature (in my form). So in this case, as my wife didn;t contribute, I don;t need to file form 709 for my wfe. Its just my form. Atleast that’s how I interpret. Also the Alan Gassman’s youtube video linked in your article (at time mark 13.48), went thru this specific case – where wife doesn’t need to file her 709, as she didn’t contribute. If you have time – can you pls share if you also see this the same way or still believe my wife should also file 709 along with mine, as you suggested initially.

Again, appreciate you taking the time. I think this can help many. Thanks as always.

First, thank you ever so much! Can’t tell you how helpful this has been!

If I contributed a total of $50,000 in one year to my son’s 529, and I can fill out the 709 to claim that divided up between 5 years ($10k a year), is there any reason to further divide it with my spouse by filling out a separate 709 for him?

I probably wouldn’t bother to keep it simple, it just uses up your annual gift exclusion and keeps your spouse’s intact.

If you give a gift of over $50k, with $15k exclusion, do you have to pay tax on the amount over $15k? The tax rate on the 709 table is very high!! But it said somewhere that you don’t, if your lifetime total is under $11.6M (or some such amount)

Thx, TLH

I believe that you need to file a gift tax return, and then the overage amount will be deducted from your lifetime gift allowance. However, you need to file the gift tax return sot that the IRS can track it.

There’s a lot here, so I may have missed the answer. My wife and I contributed $52k into our daughter’s 529 account prior to divorcing the past year. How should we complete the 709 Forms. If “Yes” to Part 1/line 12, do we attach 5 year summary noting $26k each? and we both sign each others’ forms, OR “No” to line 12 and we each do our own 709 and outline the $26k still using the 5 year plan summary?

Also, other than Schedule A (B) and Part 1/A is there anywhere else (lines)on the form that the amount needs to be listed? Thank you.

A large gift of $300,000 to my sister per my Moms wishes. Stocks and Cash.

I will list assets on Schedule A

How do I fill out Part 4 deductions?

Do I need Schedule D Part 2

My mom made 6 different gifts to different people. There isn’t enough lines to list all of that in the part A box. Does she just attach a separate piece of paper with the information about each gift?

What is there are not enough lines for the cash gifts made to one donee on form #709. What if there were twelve times when a cash gift was made in a year? How do you report each separate cash gift

According to the IRS instructions:

https://www.irs.gov/instructions/i709

I don’t know how to fill in Part 2, lines 4 with the gift tax table. i have to report 54K gifted to my brother with annual exclusion of $15K. Tax table says $3800/22%??

We didn’t file a 709 after superfunding a 529 plan in 2012. Do you know if the election to treat the contribution ratably over 5 years would be valid if made now on a late filed 709? Also, would we have to amend a subsequent 709 that was filed in 2019 to account for the unreported gift from 2012 (to make Schedule B prior gifts accurate)?

Hi, IRS form 709 can be mailed to IRS addr, separate from my 1040 packet.. ? thanks

Yes, 709s can’t be e-filed and must be paper- filed to the IRS address per the instructions.

Hi Jonathan, This has been helpful in many ways. I have one older child for whom I superfunded the 529 and know that I have to file form 709 (and exceed the annual gift limit) but for the younger child I chose to make contribution below the annual gift limit. I wonder if I only fill the information for the older child whom I gift above the annual gift limit. Or do I have to provide all the information two separate schedule A one where I chose to divide the contribution over 5 years (older child) and another I chose to not do that. Any insight will be helpful. Thanks

Jonathan, thank you for the straight forward sample we can use. I did notice that Jay the CPA & EA had suggestions to correct some errors on your form. Would it be possible to update your sample form after incorporating his comments? I’m trying hard to follow but it’s challenging

With lots of Series I Savings Bonds ripe for redemption now, can you superfund a 529 with Savings Bond proceeds and apply the full super funded amount to the interest income exclusion calculation in the year of redemption (assuming age/income requirements are met)?

Jonathan, when you mention in your blog that each spouse must file their own gift tax return when gift splitting – you’ve only included one sample return. Would spouse B’s gift tax return be identical to spouse A’s (with just the names / signatures of the spouses being swapped) – i.e. would the attached Statement as well as the numbers in Schedule A Part 1 be identical for both spouses including the option for selecting Gift splitting?

Did you get answer to this? I have the same question. Are the form for both spouses filled with the same details?

Jonathan, could you share the second spouses sample form also please.

Yes, they would pretty much be identical except for switching the names.

Does anyone have an example of a single one time gift of $100,000.00 cash to niece, where the donor is single. No spouse involved, no trusts involved, with are both US citizens, just $100,000.00 in cash one time gift. I suspect I would subtract the annual gift tax deduction of $17,000.00 with a balance gift of $83,000.00 I suspect I would have to deduct the $83,000.00 from the life time exclusion of $12.92 million or $12,920,000.00 – $83,000.00 = $12,837,000.00 life time exclusion remaining. I suspect neither I (donor) or my niece (donee) will pay any gift tax. If anyone out there can create an example of these circumstances I would truly appreciate it.

My wife and I sold a second home to our son and his wife. The price was under fair market value. The amount under the fair market value is the gift. Of that amount can we each use the 17K exclusion for each son and daughter in law? For a total of $68,000 excluded? My wife and I were joint owners (both names on the deed) and the property is now in my son’s and wife’s name (both names on the deed).

Scenario: A grandfather gives a 2023 contribution of 75,000 to a 529 Plan with the grandchild as the beneficiary. The father of the grandchild controls the 529 account. It is elected to be a split gift on Form 709. 5 year superfunding is elected, resulting in net transfers for 2023 of 7,500 from each grandparent.

Can the same thing be done again in 2024, using 5 year superfunding with another 75,000 dollar gift?

I’m not sure if concurrent superfundings work, but why not just have Grandparent 1 do the 75k in 2023 and Grandparent 2 do their own 75k in 2024. Would be more clear and less filings.

Thanks so much for the guidance.

You wrote “…A by-product of this is that on page 1, Part 1; lines 12, 13 & 14 should be left blank.”. Do you mean that Line 12 should be answered “No” and lines 13 to 18 should be left blank?

I am US citizen, working and living in India and paying taxes in India, and I gifted some US stocks last year to dependent daughter living and studying in US college in US who is also a US citizen. As per Form 709 instructions, I owe gift tax, will I pay gift tax to IRS in US or tax in India? As per Indian tax rule, there is no limit on how much we gift to child.

Statement from the above comment by Jay the CPA:

“No GST. If the 529 is established by the grand child’s parents and you merely contribute to it, there would still be no GST (generation-skipping tax). The owner would be your child (or son/daughter-in-law) for the benefit of the grandchild. Therefore, the gift technically only goes down 1 generation”

My Question: : On Form 709, would the 529 contribution by me (grandparent) to a 529 plan in which my son is the account holder and my grandson the beneficiary, be reported On Schedule 5 Part 1 (Gifts Subject Only to Gift Tax) or on Schedule A Part 2 (Direct skips subject to both gift tax and generation skipping transfer tax). The contribution was superfunded and below the exclusion amount).

Thank you for help with this confusing form.