Do you know what your household’s savings rate is? Most of us probably have a rough guess, but I wanted to use some more reliable data. Here’s the definition again for my purposes:

Current Spending

There are plenty of ways of tracking your expenditures, as anyone who has tried to follow a monthly budget has found out:

- Handwritten expense lists

- Excel or other spreadsheets

- Online budgeting tools

- PDA/Smartphone input tools

- Automated account aggregation tools

I’ve tried various methods to track my expenses manually, but never had the commitment to follow through for more than a month or two at a time. I track all of my numerous financial accounts using account aggregation site Yodlee, but since August 2009 I have linked my primary checking accounts and the few often-used credit cards at the similar-but-nicer Mint.com.

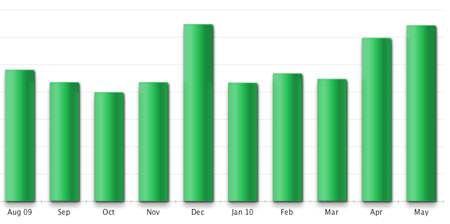

It took a lot of manually categorizing individual transactions, but now it takes less than 10 minutes every couple of weeks at Mint to correct the few new stores I visit (mostly small restaurants). This means I almost have an entire year of spending data from August 2009 to May 2010:

As you can see, there was a general trend, but a few months had major spikes. December had holiday gifts, some travel, and end-of-year charitable giving. In April, we bought a new high-efficiency washer/dryer and had some home electrical-repair bills. In May, we bought our plane tickets and hotel accommodations for a trip to Peru. The lesson here is that there are always going to be these spikes, and it’s best to be prepared and account for them. Our actual average spending ended up being higher than I would have guessed. The monthly fluctuations ranged from 20% below average in October to 30% above average in December.

Current Income

We are a dual-income couple with no kids currently. Our “big-picture budget” is to be able to live off the lesser of our two incomes. We each make relatively good money, so we have been lucky to be able to do this for a few years now. On a practical basis, we do this by having one primary joint checking account in which we only direct deposit that one paycheck. All bills are paid out of this account. This way it psychologically easier to “live within the means” of that single paycheck as the balance goes up and down.

Current Savings Rate

I don’t reveal actual income numbers, so it’s easier to share the savings rate. I am using after-tax income because I feel it is more applicable. According to the above data, on average we spend 84% of the single after-tax paycheck each year, giving us a saving rate of 16%. This is helpful to know we have a buffer if one of us were to lose our jobs. (We also max out the pre-tax 401k plan employee contributions at our jobs, so the single paycheck is already reduce a bit.) When both of our incomes are included, our saving rate is over 60%.

You may consider this low or high, but in terms of early retirement for most people you’ll need to put away a lot more than the 10 to 15% recommended by some experts. I like the idea of both spending a year’s worth of income and saving a year’s worth of income, although this will not be realistic for everyone.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I have to tell you, this blog is harder and harder to read realizing that you all make so much dang money and making this relevant. One should have a minimum of $200K income before you are allowed to view some of these posts to not feel shame.

In a similar boat to you (dual income no kids). We save >60% of net income too, but don’t look at if we can live of one paycheck or not.

Instead I calculated the income we need to sustain a frugal version of our lifestyle (pay mortgage, food etc – but not discretionary spending that sneaks in). We dialed in our mortgage / purchase price so that that required income # is lower than the lower of our two incomes.

I dont think it is so hard Justin for understanding this blog and “a minimum of $200K income” is a far too exaggerated figure. I find it very simply explained on the current savings rate and I totally agree with the formula. We too are dual income no kids group but still find it very important to do savings or else refinancing is the only option for some really urgent jobs to be done.

@Justin,

You have no idea what he makes, nor how much he spends?

Do you intend to have kids? If so, do you intend to have a SAHParent? If so, are you prepared to cut that savings rate from 60% to 16% when the time comes? You are clearly making right decisions with managing money, but dreams of early retirement can make the decision to lose one income that much harder to do. Our savings rate on my single income (my wife is a SAHM for our two kids with plans for two more), is 15%, but our ability to travel is severely curtailed and I don’t save as much for retirement as I’d like to. My business, unfortunately, is my retirement nest egg.

Wow Jon, that’s really impressive. Keep it up, and thanks for sharing!

@Justin,

I would think the ideas and concepts here can (and should) apply to anyone, at any income level. Learning how to manage your money, create savings, and, if you can, invest is useful info for all. This post in particular – you need to know what your situation is now, in order to look forward, plan, and hopefully improve it.

Not everything here will apply to everyone, or should it. Take what info you want or can make use of, and skip over the rest.

Wow, that’s a prodigious savings rate any way you measure it. Good job. We have a slightly different situation, one income and a baby (on the books for one year now) in the household. In the last twelve months we’ve saved an amount equal to 42% of my pre-tax income (57% of post tax). That includes the dollars I put into a savings account, contributed to my DC plan at work, and put away for college. I didn’t realize we were doing so well until I just did that exercise.

I’m also not including forced savings from paying down our mortgage. Does your equation implicitly capture that as saving? Seems like it may.

The “plan” for when we have kids seems to shift all the time. For a while, I was planning to be the stay-at-home parent. After watching some other families, who knows how Mrs. MMB will feel after they arrive. Will she want to work? Some mothers love work still, some put their careers on hold. We will probably do some combination of both part-time or one parent stay-at-home.

Our savings rate will most likely not stay this high, if it makes you feel better Justin. 😉

Thinking about if I’m happy with the 16%, I do think we spend a lot of travel (or will, once we get back into things) for which I don’t plan on traveling at all hardly during the first years of having kids. How much do diapers cost again?

@Andy – That’s very impressive. I’m not including the forced savings from our mortgage payment either. Our mortgage is over 50% of our monthly spending each month.

I will take it into account, however, when I estimate future spending. Even though it’s technically separate, I think that I will consider my semi or fully-retired only when the house is paid off.

Property taxes and home maintenance will still be there, but since our home is in an expensive area, I’d much rather be just paying those things.

Having a saving rate of 60% is terrific, however it’s a wise idea to keep up doing it while you have no children. You will never be able to save at the same high rate once you have kids, so you might as well do it at maximum now.

While I agree the amount you save is over 60%, is the actual amount closer to 70%?

BTW, I prefer to add up savings (cash, retirement, equity investment plus debt principal retirement ahead of schedule), rather than just subtract expenses from income.

This way I can’t miss some mystery expenses and I track where my savings are going.

Don’t pick on Justin too much. I’ve quietly thought the same thing for a long time.

I also calculate my savings rate as part of my budget, although I don’t do it month by month. I follow the method of Elizabeth Warren’s “All Your Worth” and count my employer’s pension contribution as part of my savings. Like Jonathan, I translate any pre-tax savings into after-tax equivalents.

Technically, it’s just for entertainment though. I have a spreadsheet that I use to predict my necessary nest egg based on modest assumptions, and I use that calculation to see if I am saving enough to be on track.

This is done with monthly numbers? Annually? Current income is pre tax? post tax? add back in 401K deductions?

Ah! I also enjoy Mint. Though I haven’t quite got it trained to report properly for all the places I visit. It sets your budgets off when they pile into the wrong sections. Still a fabulous tool I think. 🙂

If he was bragging about a high savings rate, I can see where some readers would take offence—or just choose not to read the blog. But I think our host was just being objective, and objectivity is the key, whether you’re saving 1% of your income or 80% of it. Keeping track of expenditures is the lesson here, and making yourself accountable for what you save.

For everyone out there fighting the good fight—keep up the great work!

Cheers,

Andrew

Let me clarify:

I’ve been a long time reader from back in the pre-600K house purchase days. The point of my comment was that it is sometimes depressing to read this blog to see “what the other half has” with respect to spending and saving. I should have said “these types of posts are harder and harder to read.” I was just blowing some steam.

Because I am a long time reader, I know just about how much they make. When I compare this to how much they are saving and do the math, it can be depressing because it is simply not possible for me to ever achieve unless I “work harder and/or smarter, (and get some luck behind me).” I don’t get all excited when I see some of you commenters reflecting the same thing. For all I know, you are addicted to saving. Your hobby might be saving money. You might make your shoes out of old pallets and potato sack string. Because it is possible to live on $12K a year, doesn’t mean that my family is going to do it!

However, I know that Jonathon leads a somewhat normal professional life with a normal food budget and a $600K home.

Good job on your savings rate Jonathan! Now is the time to do it. You could be like a lot of the folks out there who have dual incomes and spending it all like it will never end. By living on one income, it will be much easier to adjust if something were to happen to one spouse’s job, having kids, or any of life’s challenges and changes. I can save 45% of my income, but I’m a 52 year “old” guy who already has purchased most of the “stuff” that I want so its easy for me. Keep up the good work, I enjoy reading your blog from time to time.

Believe me, I know that our income is above average, and our house is above average. Hey, our spending is above average too. And the 600k home is close to 500k now. That’s the reason behind these new metrics “beyond net worth”. The net worth updates are probably going to stop soon if I can get my act together for some good alternatives.

For example…. if your home is 200k that you bought for 150k, and you thus spend less in your area than me… you might be much closer to financial freedom than you think!

I don’t like reading the feeling of “shame”, though I understand where it comes from. I don’t feel shame when I read about hedge fund managers or CEOs other highly paid individuals. Lots of people around me make more money than I do, usually with bigger homes. I only feel envy when I hear about my friend’s parents who are happy ex-pats in Mexico by 55. They figured out a way to their dream. It’s a long journey. 🙂

Do you have separate savings funds for future spending you know you’re going to incur? For example, we have a travel fund that we save for every month, plus a child fund and car fund. To me, these are fixed expenses that I’m pre-paying for and I don’t include them when I calculate my savings rate. Maybe it’ll take me 1-2 years to save up for a major expense I know I will incur so I feel that looking at average spending over 1 year doesn’t really give me the whole picture.

babies actually don’t cost that much. I’ve found the biggest expense to be childcare and saving for college.

Jonathan,

One day I’ll spell your name correctly. I think it’s just that you seem so normal, like one of the “little guys” fighting for survival. If I were reading the blog of a fund manager or professional sports player, I would consider that person in a whole different class of citizenry.

Again, it was just a stupid vent. The reality is that outside of mymoneyblog, we are a very, very lucky family and have much to be thankful for in comparison to so many.

Jonathan,

You figured your savings rate by keeping track of your spending. Personally, I have found it much easier to keep track of the actual savings.

I know all the places that we save money (401k, Vanguard account, brokerage, 529, Bank). It doesn’t take too much time to open each of these and add up the new money for the year. Except, for the bank account, I just take the difference of the balance between Jan 1 this year and Jan 1 last year.

This gives me a good estimate in just 30minutes time — once per year.

I did the same thing with taxes, btw.