![]() Automated portfolio managers like Betterment will set you up with a diversified mix of index funds and manage it for you for a small fee. I’m an investing geek, so I always lean towards keeping the small fee and manage things myself. But an important variable to this equation is tax-loss harvesting (TLH). Tax-loss harvesting tries to improve your returns by minimizing your tax bill, but it is also tedious work that is ideally suited to handing over to a computer.

Automated portfolio managers like Betterment will set you up with a diversified mix of index funds and manage it for you for a small fee. I’m an investing geek, so I always lean towards keeping the small fee and manage things myself. But an important variable to this equation is tax-loss harvesting (TLH). Tax-loss harvesting tries to improve your returns by minimizing your tax bill, but it is also tedious work that is ideally suited to handing over to a computer.

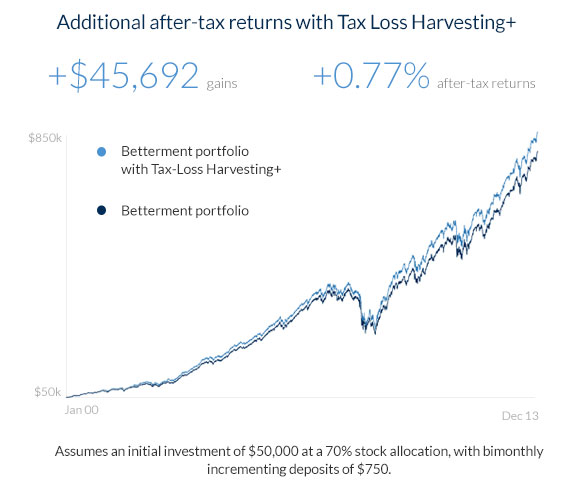

If the management fee they charge is theoretically 0.25%, as long as the benefit from tax-loss harvesting is at least 0.25%, then you’re already ahead of the game. The problem is that predicting the actual benefit of TLH is difficult. Betterment claims that based on past data, their Tax Loss Harvesting+ service could add an estimated +0.77% in after-tax returns, annually:

Up until recently, you also needed $50k in your portfolio. But Betterment just sent me an e-mail today (April 2015) that their tax-loss harvesting service will be available to all taxable accounts with no minimum balance requirement:

Using our smarter technology, we’ve now made Tax Loss Harvesting+ available to you and all of our customers—regardless of balance—at no additional cost.

We are the only automated investing service to provide this tax-reduction strategy, once only available to the wealthiest, for all investors. By democratizing tax loss harvesting, we are continuing our mission of making smarter investing accessible to everyone.

I would not have predicted this a few years ago: automated tax-loss harvesting for any account size and at such a low cost. A customer with $10,000 would be getting TLH and portfolio management for $25 a year. Betterment has no minimum investment requirement.

I would say that I am confident the benefit of TLH over the long-run will be greater than zero. However, I would not count on 0.77%. But even if we split the difference and assume it is 0.4%, then using such a service still has to be considered as it is greater that their management fee of 0.15% to 0.35%. I hate giving up control though, so while I have put a little seed money in various places, I am still 95%+ DIY and keeping a close eye on future developments.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I think 0.4% is optimistic. It’s really only valuable for the initial deposit. As the market tends to increase over time and there would be no losses to harvest after a certain point, barring a 2008-esque epic market collapse, in which case you don’t need a robo to notice that one.

You don’t need a market collapse to gain a benefit from tax-loss harvesting, you just need one of your ETF-held asset classes to have dropped in value (the software checks every day) since you’ll likely be making additional contributions over time. One year it might be emerging markets, another year it might be the US stock market. I’d be a bit scared to see what my Schedule D looks like with 100 extra trades on it, but there will certainly be more opportunities for loss realization in the future.

I disagree. Most of the TLH happens in the beginning. After some time, all positions have large unrealized gains. There’s nothing to harvest. The new money you are adding becomes a smaller and smaller percentage of the total invested. Meanwhile, you are stuck in the secondary ETFs paying higher expenses.

As was recently posted on Bogleheads:

“Something interesting I’ve learned is to not expect a switchback after 30 days. In all of these TLH events the market has recovered by then, and Betterment won’t switch back at a gain. So the TLH’ed funds tend to get “stuck” in the secondary ETFs until a bigger downturn occurs. At some point the unrealized gain of TLH’ed shares will be so big that there will be almost no chance of a downturn being big enough to TLH them again, and there’s more or less a 50/50 chance of whether they’ll be in the primary or secondary ETF at that time. Currently more than 50% of every asset class category is in the secondary ETF. So I may end up paying the higher expense ratio of the secondary ETFs “forever” due to the TLH. But I’m essentially reinvesting the tax savings, and expense ratios will change over time, so it’s hard to say whether it’s a net gain or loss in the long run in the case of, e.g., a mere 2% harvested loss in VOE (which occurred on 10/10) into IWS with 0.16% in extra expenses. My guess is that if TLH is considered “in aggregate” then it’s a net benefit long-term but that some individual TLH events may not be.”

Well, VOE and IWS is a bit of special case. Most roboadvisors won’t hold a mid-cap value ETF, and it won’t be a huge part of your portfolio even if it is included. I wouldn’t mind switching between similar Vanguard and Schwab ETFs for tax-loss purposes, there is enough competition now that the expense ratios will be extremely close.

The average investor for these roboadvisors are young and just starting their portfolios. Stock market performance has been great since 2009. I can’t see how there won’t be more TLH opportunities in the future. I agree that there is an opportunity for better research papers that would set reasonable expectations for tax-loss harvesting alpha.

With the introduction of these automated tax loss harvesting services, I’m a little surprised I cannot find a personal finance blogger who shows what the Schedule D looks like in a given year where a Wealthfront/Betterment TLH strategy was employed. Maybe they are too new. Maybe with the recent changes, we’ll see it for next year.

I would like an idea of the added complexity for my taxes before I would consider this a good option.

A lot of bloggers have put in a few thousand to try it out, but not many put in the 100k to get TLH. But after this change, I would bet in February 2016 you should be able to see more Schedule D forms that include TLH trades.

@redbeardedmike Here’s your idea, also posted on bogleheads:

“I had an account with Betterment from 2013-May 2014. They kept changing their ETF mix, so my funds were churning more than I liked. I left before they introduced their TLH features.

If I remember correctly, the 1099-B/DIV for tax year 2013 wasn’t available until Jan 31st 2014. And the 1099 for tax year 2014 wasn’t available until the second week of Feb, 2015. I don’t get my W-2 until the end of January, so waiting an extra week or two isn’t terrible. The 1099 summary looks correct, but the detail is 22 pages long. It is downloadable by both TurboTax and H&R Block tax software which is nice.

I don’t have any info on what a TLH 1099 looks like, but I imagine that it’d only be a couple more pages long.”

https://www.bogleheads.org/forum/viewtopic.php?p=2402917#p2402917

Very informative post. I have to admit I have never heard of TLH in my life but I made a note to do some research and learn more about it!!! I also consider myself a DIY investor (love the excitement of it) so I am not sure I’ll be their target clientele as I’d be hesitant to hand over my portfolio to Betterment. Nonetheless, I believe this can be a very valuable service for a lot of people. Will check out your post on wealthfront as well. thanks for sharing!

Betterment is a fairly significant and growing part of our portfolio (about half of our taxable accounts). To me, the features (automatic rebalancing etc) are worth the fee simply because I don’t have to think about it. I’ve yet to see a TLH event in my account, most likely because the markets in general haven’t dropped significantly in the last year or so when I started adding significant money.

I make deposits at least weekly as cash comes in which makes me somewhat happy I don’t have to look at the number of lots I have.. 😉

For me it makes sense to defer the taxes on gains and take the $3k write off each year (assuming the Betterment portfolio can ever generate such amounts). Our marginal tax rate is 33% plus California’s 9.3% cut so a $3k write off is an extra $1269 that can be invested. We save around 33% of our gross income so when we retire we will almost certainly be in a lower tax bracket, possibly even able to enjoy a 0% rate on gains if they still exist (since we’ll be withdrawing a mix of capital and gains/dividends) to meet our spending needs. I plan to use the early years of retirement to roll as much of our pre-tax accounts over into Roth IRAs as possible during that time.