(This post is part of a new series taking a closer look at some popular portfolio holdings.)

The Vanguard Total Stock Market Index Fund is one of the largest funds in the world, and definitely the largest index fund. For individual retail investors, it is available in mutual fund flavors (VTSMX, VTSAX) as well as ETF flavor (VTI). Across all shares classes, there is currently over $230 billion dollars of total assets invested in this fund – that’s nearly a quarter of a trillion dollars! If you own a Vanguard Target Retirement or LifeStrategy fund, you own this fund as well. So let’s try to understand what’s inside.

Despite the name, the Vanguard Total Stock Market Index fund only tries to represent all the stocks in the U.S. equity market, from big to small, from financial companies to shoe store chains. The fund is currently transitioning from tracking the MSCI US Broad Market Index to the CRSP US Total Market Index. These are both market-cap weighted indexes, which means that the amount of each stock held is directly proportional to the total market value of the company. In other words, if all Nike shares together are worth $50 billion while Skechers is worth $1 billion, then the index would hold 50 times more Nike than Skechers.

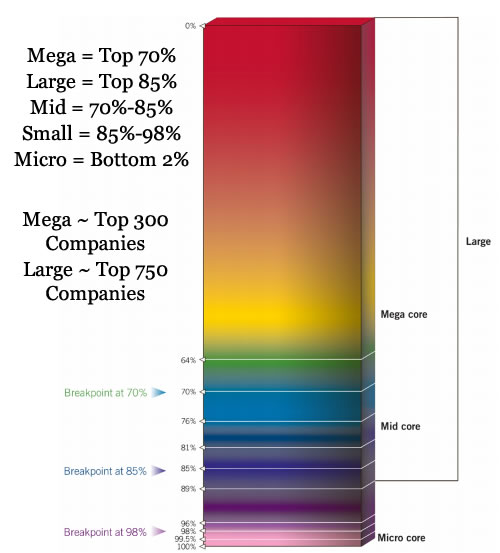

Market Capitalization Weighting

Above is a chart showing how the CRSP US Total Market Index is broken down. CRSP categorizes companies into Mega-cap, Large-cap, Mid-cap, Small-cap, and Micro-cap by cumulative market capitalization, as opposed to a fixed number or a set number of stocks. For example, “Mega cap” companies are those in the top 70% of cumulative market cap. This works out to roughly the 300 largest companies, or the companies worth more than about $2.6 billion. Note that CRSP defines “Large cap” stocks as the combination of “Mega” and “Mid” cap stocks, which can be a bit confusing.

Currently the total amount of stocks in the CRSP index is around 3,600. The smallest company in the index is worth only $2 million. The largest company is worth over $400 billion, or 200,000 times larger than the smallest company. A very wide range. Right now, VTSMX owns all 3,225 companies inside the MSCI index, so I am assuming it will own nearly all of the companies in the CRSP index. (The CRSP index includes some micro-cap stocks that MSCI does not.)

This also means that the top 700 or so stocks make up 85% of the fund, while the bottom 3,000 or so make up only 15% of the fund. The big corporations are really big. The top 10 holdings alone make up 15% of the fund. Some people may view this as a negative, but it also tends to reflect their relative impact on the economy.

Owning the Haystack

Owning a piece of every single stock that is publicly-traded is a powerful thing. Back in 1997, Apple Inc. had a market cap of around $2 billion. Today, the market cap is over $400 billion. That’s 200 times larger, or a 20,000% return over just 16 years. Instead of trying identify ahead of time that little company that will be the next Apple in 2030, you may already own it. To paraphrase a well-known quote from Vanguard founder Jack Bogle:

Don’t look for the needle in the haystack. Buy the entire haystack.

You may not make a 20,000% return, but you will own the result of whatever innovation comes in the future. It make come from one of the big names like Exxon and General Electric, or it make come from a company you’ve never heard of before. Just sit back and relax. 🙂

Another benefit that results from all this is minimal trading and thus very little turnover. If a company rises (or drops) in value, then with market-cap weighting it should be a larger (or smaller) part of the portfolio and there is no need to buy or sell any shares. Since you own the whole haystack, you don’t even have to worry about a company going from “large-cap” to “mid-cap” or vice-versa. This means the fund is very tax-efficient and distributes very little taxable capital gains. In a taxable account, this improves your after-tax returns and lets compounding do its thing.

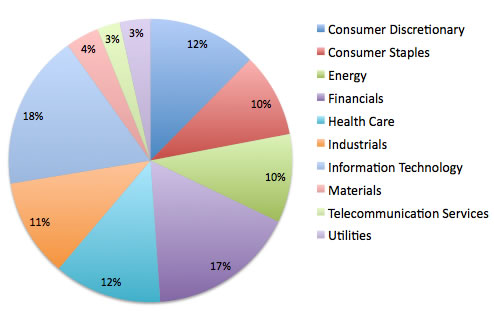

Sector Breakdown

Here is the overall breakdown of VTSMX holdings by sector, as 3/31/2013.

Fund Management Expenses

As of 4/12/2013, the annual expense ratio of both the ETF (no minimum) and Admiral share classes ($10,000 minimum) of the Vanguard Total Stock Market Index Fund is just 0.05%. So for every $10,000 invested, Vanguard charges a total of just $5 a year to manage this basket of stocks. There is no way an individual could replicate the underlying holding themselves for such a price. The Investor class shares have an expense ratio of 0.17%. Specifically, these fund expenses are taken out of the fund’s net asset value (NAV) a tiny bit each day (fractions of a penny per share).

Final Thoughts

By representing the entire US stock market in a complete, efficient, and low-cost manner, the Vanguard Total Stock Market Index Fund is the epitome of a “core” portfolio holding. Owning a competing index fund that also tracks a broad US index using market-cap weighting with a similarly low expense ratio will likely give you similar results. However, I give a slight preference to Vanguard due to (1) their “at-cost” client-ownership structure helps to ensure that costs will stay low, and (2) their experience and skill at indexing.

Disclosures: VSTMX/VTSAX/VTI is a cornerstone of my portfolio, and I expect it to stay that way for the foreseeable future.

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

You’ve an extra zero in your Apple return percentage.

Thanks! Fixed.

Great review Jonathan.

Owning an index fund like the Total Stock Market Index means:

(1) you own the entire haystack and the advantages that come with it as you pointed out

(2) this is by far the cheapest way to get a diversified portfolio built

(3) your transactional costs are greatly reduced because you are not having to trade individual stocks if you were to pick stocks on your own

(4) investing in an index fund takes your emotions out of the way so that you are not emotionally tied to one or a handful of companies

It appears that Vanguard’s index switch (a witty boglehead forum poster accused Vanguard of actively managing their indexes, LOL) is mainly driven by index licensing costs.

http://www.morningstar.com/cover/videocenter.aspx?id=569429

I can understand paying to license a more complicated index like foreign markets, emerging, specialized sectors, etc. But why would you need to pay for an index for something so trivial such as a market cap breakdown? Why don’t brokerages just call it a generic “Top 70% U.S. Market Cap fund” and pay no licensing fees, period?

Just bought my first Vanguard index fund (VFINX) in a traditional IRA to get a bit of a break on this years taxes, as well as, start saving for retirement. What I’m left wondering is if I made the best choice in fund based strictly on the basis that it is around an all time high.

I’ve heard some say this a non-issue for a long term investor, but still wonder if I should move it into something else before I start taking a hit.

@Tony: No, if you’re a long term investor, you should leave it in VFINX. If you start trying to guess which sector is going to going to be the next hot one, then you’re playing stock market games. You could win, you could lose. For all anyone knows, VFINX/S&P500 could keep going up from here and never ever come back down to this level.

Case in point, in 1995, the S&P500 hit its all time high. After that, it kept going up and up. Even during the crashes of 2001 and 2008, S&P500 never dropped below 1995 levels.

@Bucky – Well, creating indexes themselves is not a very efficient market. 🙂 Agreed that it’s all about lower costs, previous post:

https://www.mymoneyblog.com/vanguard-index-fund-benchmarks.html

@Tony – What @Bucky said… if you really knew what was coming up, you could do something. But you don’t. I don’t. Buffett don’t. As long as your horizon is long, just relax and you’ll be fine. If the S&P 500 is at 1600 today, do you really care if you bought in at 450 or 500 long long ago?

“What I’m left wondering is if I made the best choice in fund based strictly on the basis that it is around an all time high.”

It’s at an all time high up to the present day — do you know if it’s at an all time high when looking 50 years into the future? No, and no one does. All the “all time high” tells you is how it’s done in the past — but the past is over, and it tells you nothing about how it’s going to perform in the future.

I’m nearing retirement and just now asking the question “am I investing my money in a way that benefits me or the financial adviser who has my money?” I’ve wondered about Vanguard but, from what the fees look like, I could just give my money to a ‘fee only’ adviser and do just as well don’t you think?

I am a 80 year person I don”t need money for my livings expences that all ok, I sold some property a few months ago,and would like some funds monthly to spend on the kids and grandkids. we have a few hundred thousand to invest, looking at your posts, and looking at Kiplingers posts, I get a little confused on the leters on the Index funds of vandguards funds, the artical talked about 5 index funds. I would like to invest in funds, and take most of the gain out monthly.

Tell me what you think thanks