I’m a fan of the Vanguard Target Retirement 20XX Funds. These Target Date Funds (TDFs) may not be perfect, but they are a low-cost, broadly-diversified, “set-it-and-forget-it” fund that I feel are consistently under-appreciated and easily maligned due to their inherent “one-size-fits-most” nature.

In a recent Vanguard blog post titled “TDF investors are not rotisserie ovens”, senior product manager John Croke felt the “set it and forget it” description “fuels the misperception that many investors in TDF strategies are disengaged, disinterested, and generally unaware of what they’re invested in.”

The subsequent points he makes are certainly valid, but I happen to think the rotisserie oven analogy should be worn as a badge of honor! As Jason Zweig writes in the WSJ article “Radical Investing Advice: Do Nothing, Nada, Zilch, Zippo”:

Target-date investors, says Jeff Holt, an analyst at Morningstar, “are less prone to take matters into their own hands and move their assets around when markets are gyrating.”

[…] research by Financial Engines found that participants with little or no money in target-date funds underperform them by an average of 2.1 percentage points annually.

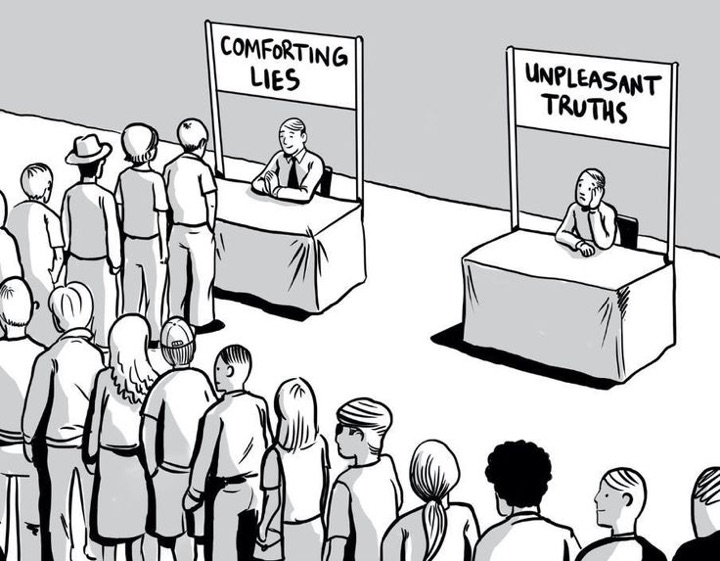

You won’t see Vanguard Target Retirement funds being touted very much in the financial media. Their returns are rarely at the top since they are index-based, so magazines and newsletters won’t write about them. Most advisors are supposedly charging you for their “expert” advice, so they will of course recommend something more complicated. Even index fund enthusiasts like myself often don’t invest in them because we like to fine-tune and tinker (sometimes to our detriment). They never seem to be the “best” move, just something you settle for when you can’t think of anything better. I think this cartoon describes the situation well (found via @michaelbatnick):

It is an unpleasant truth that most people would be better off just focusing their energy on savings rate and leaving the investing to a Vanguard Target Retirement Fund. Another example of the power of inaction: A person who bought the 30 largest US companies back in 1935 and did absolutely nothing after that would have outperformed the S&P 500 over the last 40 years.

Now, I should throw in a few quick points from the Vanguard blog post about what investors shouldn’t forget about:

- TDFs will continue to hold a certain amount of stock risk after you reach your target retirement age.

- Along the same lines, TDFs do not provide guaranteed income in retirement.

To summarize, don’t be insulted when being compared to a Ronco rotisserie oven. Be proud to “Set it and forget it”. Vanguard Target Retirement Funds even perform the chore of rebalancing between stocks and bonds for you automatically. Perhaps Vanguard could even use some tips from Ron Popeil about marketing their low, low pricing 😉

The Best Credit Card Bonus Offers – March 2024

The Best Credit Card Bonus Offers – March 2024 Big List of Free Stocks from Brokerage Apps

Big List of Free Stocks from Brokerage Apps Best Interest Rates on Cash - March 2024

Best Interest Rates on Cash - March 2024 Free Credit Scores x 3 + Free Credit Monitoring

Free Credit Scores x 3 + Free Credit Monitoring Best No Fee 0% APR Balance Transfer Offers

Best No Fee 0% APR Balance Transfer Offers Little-Known Cellular Data Plans That Can Save Big Money

Little-Known Cellular Data Plans That Can Save Big Money How To Haggle Your Cable or Direct TV Bill

How To Haggle Your Cable or Direct TV Bill Big List of Free Consumer Data Reports (Credit, Rent, Work)

Big List of Free Consumer Data Reports (Credit, Rent, Work)

I know somebody who pays 3% advisor fees to put him into funds that cost 1-2% yearly that have a similar allocation as a target date fund. This particular person is very frugal. Fights for every dime. But when it comes to his IRA of around a million bucks, he’s ok losing around 4K a month to fees. Some people just don’t get it.

It’s easy to not get it because the way it’s set up today its an ‘invisible’ loss… there’s no line item on your monthly statement that lists out the fee you’ve paid to any of these advisors or funds, it’s just baked into the bottom line. It’s one of those situations where if you don’t know what you don’t know, then it’s easy to assume the 2% drag they state in the brochure is just a fair fee everyone has to pay and can be chalked up to cost of doing business. It’s not intuitive, and it probably won’t be until there’s a change to make the invisible more visible for everyone.

People just don’t know. Have you introduced him to Personal Capital?

@Ross:

What you say is true, but at the same time, it’s each person’s responsibility to do their due diligence and educate themselves about their own financial situation. These things are not unreasonably hard to understand. For example, you just clearly explained the situation in a few sentences. The main problem seems to be that most people have a dependency mindset when it comes to anything financial. They believe they’re constitutionally incapable of managing their own finances and fear having the responsibility for doing so.

What do you think of the Vanguard resettlement funds, vs a Robo Investor like Betterment?

I’m not exactly sure what to think about robo investors yet. They are still developing their toolbox, adding things like tax-loss harvesting, managing withdrawals in retirement, and the ability to adjust for outside accounts not held by them. Right now, I think of them as a reasonable choice for people who want to go that way. If you have rather modest assets, I’d probably still stick with a Vanguard Target fund. If you are in a really high tax bracket and have significant taxable assets, then the tax-loss harvesting might help enough to offset their additional layer of fees.